Tamilnadu State Board New Syllabus Samacheer Kalvi 11th Accountancy Guide Pdf Chapter 1 Introduction to Accounting Text Book Back Questions and Answers, Notes.

Tamilnadu Samacheer Kalvi 11th Accountancy Solutions Chapter 1 Introduction to Accounting

11th Accountancy Guide Introduction to Accounting Text Book Back Questions and Answers

I. Multiple Choice Questions

Choose the correct answer.

Question 1.

The root of financial accounting system is

(a) Social accounting

(b) Stewardship accounting

(c) Management accounting

(d) Responsibility accounting

Answer:

(b) Stewardship accounting

![]()

Question 2.

Which one of the following is not a main objective of accounting?

(a) Systematic recording of transactions

(b) Ascertainment of the profitability of the business

(c) Ascertainment of the financial position of the business

(d) Solving tax disputes with tax authorities

Answer:

(d) Solving tax disputes with tax authorities

Question 3.

Which one of the following is not a branch of accounting?

(a) Financial accounting

(b) Management accounting

(c) Human resources accounting

(d) None of the above

Answer:

(d) None of the above

Question 4.

Financial position of a business is ascertained on the basis of

(a) Journal

(b) Trial balance

(c) Balance Sheet

(d) Ledger

Answer:

(c) Balance Sheet

Question 5.

Who is considered to be the internal user of the financial information?

(a) Creditor

(b) Employee

(c) Customer

(d) Government

Answer:

(b) Employee

II. Very Short Answer Type Questions

Question 1.

Define accounting.

Answer:

According to the American Institute of Certified Public Accountants “Accounting is the art of recording, classifying and summarising in a significant manner and in terms of money, transactions and events which are in part, at least of a financial character and interpreting the results thereof’.

Question 2.

List any two functions of accounting.

Answer:

Measurement:

The main function of accounting is to keep systematic record of transactions, post them to the ledger and ultimately prepare the final accounts.

Comparison:

Accounting helps to compare the actual performance with the planned performance. It is also possible to compare with the accounting policies. Effective measures can be taken to enhance the efficiency of various operations.

![]()

Question 3.

What are the steps involved in the process of accounting?

Answer:

Question 4.

Who are the parties interested in accounting information?

Answer:

The following are the parties interested in accounting information

Question 5.

Name any two bases of recording accounting information.

Answer:

Cash Basis:

The actual amount of cash received and cash paid is recorded in this. Any kind of income received and expenditure paid will be entered in this.

Accrual or Mercantile Basis:

The income which is not received but has been earned or accrued and the expenses incurred, which is paid and not recorded, is known as Accrual or Mercantile Basis.

III. Short Answer Questions

Question 1.

Explain the meaning of accounting.

Answer:

Accounting is the systematic process of identifying, measuring, recording, classifying, summarizing, interpreting and communicating financial information. Accounting gives information on:

1. The resources available.

2. How the available resources have been employed and

3. The results achieved by their use.

Question 2.

Discuss briefly the branches of accounting.

Answer:

The following are the branches of accounting:

Financial Accounting:

It involves recording of financial transactions and events. It provides financial informations to the users for taking decisions.

Cost Accounting:

It involves the collection, recording, classification and appropriate allocation of expenditure for the determination of the costs of products or services and for the presentation of data for the purposes of cost control and managerial decision making.

Management Accounting:

It is concerned with the presentation of accounting information in such a way as to assist management in decision making and in the day-to-day operations of an enterprise.

Social Responsibility Accounting:

It is concerned with presentation of accounting information by business entities and other organisations from the view point of the society by showing the social costs incurred such as environmental pollution by the enterprise and social benefits such as infrastructure development and employment opportunities created by them.

Human Resources Accounting:

It is concerned with identification, quantification and reporting of investments made in human resources of an enterprise.

![]()

Question 3.

Discuss in detail the importance of accounting.

Answer:

Systematic records:

1. All the transactions of an enterprise which are financial in nature are recorded in a systematic way in the books of accounts.

2. The records are classified under common heads and summaries are prepared.

Preparation of financial statement:

1. Results of business operations and the financial position of the concern can be ascertained from accounting periodically through the preparation of financial statements namely, income statement or trading and profit and loss account and balance sheet.

2. This helps in distribution of profits to the owners and to provide funds for future growth of the business.

Assessment of progress:

Analysis and interpretation of financial data can be done to assess the progress made in different areas and to identify the areas of weaknesses.

Aid to decision making:

1. Management of a firm has to make routine and strategic decisions while discharging its functions.

2. Accounting provides the relevant data to make appropriate decisions. Future policies and programmes can be planned by the management based on the accounting data provided.

Satisfies legal requirements:

Various legal requirements like maintenance of Provident Fund (PF) for employees, Employees State Insurance (ESI) contributions, Tax Deducted at Source (TDS), filing of tax returns are properly fulfilled with the help of accounting.

Information to interested groups:

Accounting supplies appropriate information to different interested groups like owners, management, creditors, employees, financial institutions, tax authorities and the government.

Legal evidence:

Accounting records are generally accepted as evidence in courts of law and other legal authorities in the settlement of disputes.

Computation of tax Accounting:

Records are the basic source for computation and settlement of income tax and other taxes.

Settlement during merger:

When two or more business units decide to merger, accounting records provide information for deciding the terms of merger and any compensation payable as a consequence of merger.

Question 4.

Why are the following parties interested in accounting information?

Answer:

Investors:

Investor is a person who is interested in investing their funds in an organization. They are the persons in need of the financial situation of the concern. They are more concerned about future earnings and risk bearing capacity of the organization which will affect the return to the investors.

Government:

The scarce resources of the country are used by business enterprises. Government also administers prices of certain commodities. In such cases, government agencies have to ensure that the guidelines for pricing are followed.

Question 5.

Discuss the role of an accountant in the modern business world:

Answer:

Record keeper:

The accountant maintains a systematic record of financial transactions. He also prepares the financial statements and other financial reports.

Provider of information to the management:

The accountant assists the management by providing financial information required for decision making and for exercising control.

Protector of business assets:

The accountant maintains records of assets owned by the business which enables the management to protect and exercise control over these assets. He advises the management about insurance of various assets and the maintenance of the same.

Financial advisor:

The accountant analyses financial information and advises the business managers regarding opportunities, strategies for cost savings, capital budgeting, provision for future growth and development, expansion of enterprise, etc.

Tax manager:

The accountant ensures that tax returns are prepared and filed correctly on time and payment of tax is made on time. The accountant can advise the managers regarding tax management, reducing tax burden, availing tax exemptions, etc.

Public relation officer:

The accountant provides accounting information to various interested users for analysis as per their requirements.

11th Accountancy Guide Introduction to Accounting Additional Important Questions and Answers

I. Multiple Choice Questions

Question 1.

The incomplete system of accounting is …………….

(a) Double Entry system

(b) Single Entry system

(c) Double account system

(d) none

Answer:

(b) Single Entry system

Question 2.

Accounts of persons with whom the business deals is known as …………….

(a) Personal Account

(b) Real Account

(c) Nominal Account

(d) Profit & Loss Account

Answer:

(a) Personal Account

![]()

Question 3.

Business transactions may be classified into …………….

(a) One

(b) Two

(c) Three

(d) Four

Answer:

(b) Two

Question 4.

The main aim of the proprietor is to earn …………….

(a) Profit

(b) Loss

(c) Cash

(d) Capital

Answer:

(a) Profit

Question 5.

Unsold stock lying in a business on a particular date are known as …………….

(a) Sales

(b) Loss

(c) Cash

(d) Stock

Answer:

(d) Stock

Question 6.

Any written or printed document in support of a business transaction is called …………….

(a) Receipt

(b) Credit Note

(c) Debit Note

(d) Voucher

Answer:

(a) Receipt

Question 7.

Withdrawn from the business by the owner for the personal use is called …………..

(a) Capital

(b) Drawings

(c) Purchases

(d) Sales

Answer:

(b) Drawings

Question 8.

……………… involves recording of transaction and events which are financial in nature.

(a) Financial accounting

(b) Management accounting

(c) Human resources accounting

(d) None of the above

Answer:

(a) Financial accounting

Question 9.

An activity which involves transfer of money or money’s worth from one person to another person is called as ……………

(a) Transactions

(b) Assets

(c) Liabilities

(d) Capital

Answer:

(a) Transactions

Question 10.

Good will is an example of …………….

(a) Liabilities

(b) Tangible assets

(c) Intangible assets

(d) Capital

Answer:

(c) Intangible assets

Question 11.

……………… developed double entry book keeping system.

(a) Luca Pacioli

(b) Kautilya

(c) Philip Kotler

(d) None of the above

Answer:

(a) Luca Pacioli

Question 12.

………….. refers to choosing a desirable course of action from alternative courses of actions.

(a) Control

(b) Forecasting

(c) Decision Making

(d) None of the above

Answer:

(c) Decision Making

![]()

Question 13.

The amount invested by the owner in the business is called …………….

(a) Capital

(b) Drawings

(c) Purchases

(d) Sales

Answer:

(a) Capital

Question 14.

A person who owns a business is called as …………………

(a) Borrower

(b) Landlord

(c) Owner

(d) Sales man

Answer:

(c) Owner

Question 15.

Records of debit and credit were found in ……………

(a) 15th Century

(b) 13th Century

(c) 12th Century

(d) 20th Century

Answer:

(b) 13th Century

Question 16.

……………. is said to be the root of accounting.

(a) Cost Accounting

(b) Stewardship Accounting

(c) Management Accounting

(d) None of the above

Answer:

(b) Stewardship Accounting

II. Very Short Answer Questions

Question 1.

What do you mean by Transaction?

Answer:

A business activity which involves transfer of money or money’s worth (goods, services, ideas) from one person to another person.

Question 2.

What is an Voucher?

Answer:

Any written or printed document in support of a business transaction is called a voucher. Examples: Cash receipt, invoice, cash memo, bank pay-in-slip etc.

Question 3.

What are goods?

Answer:

It includes articles, things or commodities in which a business is dealing with. Examples: Furniture will be goods for those who deal in furniture.

Question 4.

What is mean by solvency?

Answer:

Solvency is the capability of a person or an enterprise to pay the debts.

Question 5.

What do you mean by depreciation?

Answer:

Depreciation refers to the decrease in the value of fixed assets due to usage and passage of time.

Question 6.

What are bad debts?

Answer:

It is a loss to the business arising out of failure of a debtor to pay the dues. It is irrecoverable debt.

![]()

Question 7.

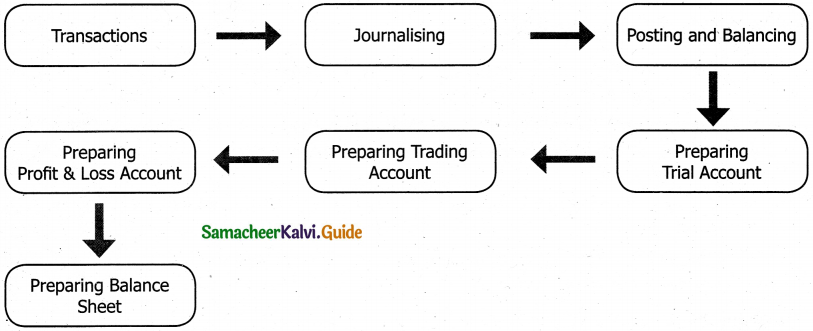

What do you mean by accounting cycle?

Answer:

An accounting cycle is a complete sequence of accounting process, that begins with the recording of business transactions and ends with the preparation of final accounts.

III. Short Answer Questions

Question 1.

Briefly explain the attributes of account emerge.

Answer:

The following are the main attributes of accounting.

1. Accounting is an art. It requires the expertise and skill of accountants design accounting system and policies, to decide the accounting process in order to suit the requirements of an organization.

2. The transactions or events of a business must be recorded in monetary terms.

3. Accounting process involves recording, classifying and summarizing of transactions and analysis and interpretation of the results.

4. The results of such analysis must be communicated to the persons who are interested in such information.

IV. Long Answer Questions

Question 1.

Explain the steps involved in the process of accounting cycle.

Answer:

Identifying the transactions and journalizing:

1. The first step in the accounting process is identifying the financial transactions of a business.

2. All the monetary transactions are recorded in the books of original entry called journals.

3. Recording the transactions in the journal is called journalizing.

4. Entries are made in the journals on the basis of source documents in the chronological order, i.e., the order of occurrence of the transactions.

Posting and Balancing:

1. Transferring the entries from the journal to the ledger is called posting.

2. In the ledger, entries are made in each account after classifying them under common heads.

3. Finding the difference between the total of the debit column and credit column of all the ledger accounts is called balancing.

Preparation of trial balance:

1. The list of ledger balances namely trial balance is prepared as the next step.

2. On the basis of ledger balances the financial statements are prepared.

Preparation of trading account:

1. Next step is preparation of trading account for a particular accounting period.

2. All the direct revenues and direct expenses are transferred to trading account.

3. The balance in the trading account is the gross profit or gross loss.

Preparation of profit and loss account:

1. It is prepared next for a particular accounting period. Alt the indirect revenues and indirect expenses along with gross profit or gross loss are transferred to profit and loss account.

2. The balance in the profit and loss account is the net profit or net loss.

Preparation of balance sheet:

1. A statement showing the balances of assets and liabilities namely balance sheet is prepared as the final step in the accounting process.

2. It is prepared on a particular date, normally, on the last day of the accounting period.

3. The closing balances of an accounting year are taken as the opening balances for the next accounting year.

4. The transactions identified and recorded for the next year are followed by posting and other steps.

5. The results are communicated to the users of accounting information for the purpose of analysis and decision making.

Question 2.

Explain the Objectives of Accounting.

Answer:

Following are the objectives of accounting:

- To keep a systematic record of financial transactions and events

- To ascertain the profit or loss of the business enterprise

- To ascertain the financial position or status of the enterprise

- To provide information to various stakeholders for their requirement

- To protect the properties of an enterprise and

- To ascertain the solvency and liquidity position of an enterprise.

![]()

Question 3.

Explain the Functions of Accounting.

Answer:

The main functions of accounting are as follows:

Measurement:

1. The main function of accounting is to keep systematic record of transactions, post them to the ledger and ultimately prepare the final accounts.

2. Accounting works as a tool for measuring the performance of the business enterprises. It also shows the financial position of the business enterprises.

Forecasting:

With the help of the various tools of accounting, future performance and financial position of the business enterprises can be forecasted.

Comparison:

Accounting helps to compare the actual performance with the planned performance. Through comparison of the actual financial results of the business enterprises with projected figures and standards, effective measures can be taken to enhance the efficiency of various operations.

Decision making:

Accounting provides relevant information to the management for planning, evaluation of performance and control. This will help them to take various decisions concerning cost, price, sales, level of activity, etc.

Control:

As accounting works as a tool of control, the strengths and weaknesses are identified to provide feedback on various measures adopted. It serves as a tool for evaluating compliance of business policies and programmes.

Assistance to government:

Government needs full information on the financial aspects of the business for various purposes such as taxation, grant of subsidy, etc. Accounting provides relevant information about the business to exercise government control on business enterprises.

Question 4.

Write a note on the Evolution of Accounting.

Answer:

1. In the earliest days of civilisation, accounting was done by stewards who managed the properties of wealthy people.

2. The stewardship accounting is said to be the root of accounting.

3. In 1494, Luca Pacioli an Italian developed double-entry book-keeping system.

4. To safeguard the interest of owners and investors, the business establishments required detailed information about business which paved the way for development of comprehensive financial accounting information system.

5. In the 20th century, the need for analysis of financial information for managerial decision making caused emergence of Management Accounting as a separate branch of accounting.

6. Though accounting was individual centric in the initial stage of evolution of accounting, it has gradually developed into Social Responsibility Accounting in the 21st century.

Question 5.

Write a note on Transaction.

Answer:

An activity which involves transfer of money or money’s worth (goods,services, ideas) from one person to another, is known as Transaction. It is of two types, namely.

Cash transaction:

It is a transaction which involves immediate cash receipt or immediate cash payment.

Credit transaction:

It is a transaction in which cash is not received or paid immediately, but will be received or paid later.

![]()

Question 6.

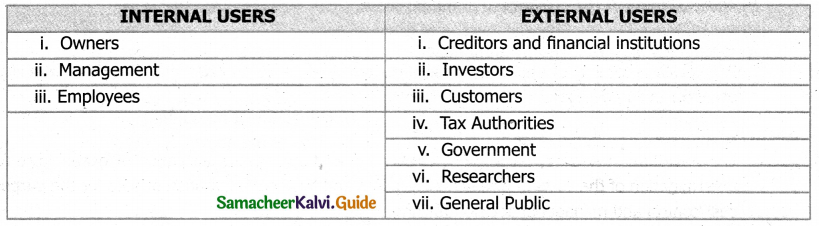

Who are ail the internal users of Accounting Information?

Answer:

The internal users are owners, management and employees who are within the organization.

Owners:

1. The owners of a business provide capital to be used in the business.

2. They are interested to know whether the business has earned profit or not during a particular period and also its financial position on a particular date.

3. They want accounting reports in order to have an appraisal of performance and also for an assessment of future prospects to ensure that they will get their expected returns from the business and get back their capital.

Management:

1. Accounting data are the basis for most of the decisions made by the management.

2. The trends in sales and purchases, relationship of expenses to the sales, efficiency of employees, comparative profitability of different departments, capital structure and solvency position are some of the vital data required by management for planning and controlling the business operations.

3. Financial statements and other reports prepared under financial accounting provide this information to the management.

Employees:

The employees are interested in the profit earning capacity of the business which will affect their remuneration, working conditions and retirement benefits and stability and growth of the enterprise.

Question 7.

Explain the External Users of Accounting Information.

Answer:

External users are the persons who are in the outside of the organisation but make use of the information for their own purpose. The following are the external users:

Creditors and Financial Institutions:

1. Suppliers of goods and services, commercial banks, public deposit holders and debenture holders are included in this category,

2. They are interested in knowing the liquidity position and repaying capacity of the business to ensure the safety of getting the amount due to them or interest and the principal amount.

Investors:

1. Persons who are interested in investing their funds in an organisation should know about the financial condition of a business unit while making their investment decisions.

2. They are more concerned about future earnings and risk bearing capacity of the organisation.

Customers:

1. Customers who buy and use the products and services of business enterprises are interested in knowing the details of the products and the prices charged to them.

2. They are interested in knowing the stability and profitability of an enterprise to ensure continued supply of the products or services by the enterprise.

Tax authorities and other regulatory bodies:

1. Accounting information helps the tax authorities in computing income tax and taxes on goods and services and other taxes to be collected from business units.

2. Other regulatory bodies also require information about revenues, expenses and other financial aspects of business to ensure that the enterprises comply with statutory requirements.

Government:

The scarce resources of the country are used by business enterprises. Information about performance of business units in different industries helps the government in policy formulation, for development of trade and industry, allocation of scarce resources, grant of subsidy, etc. Government also administers prices of certain commodities.

Researchers:

Researchers to carry out their research can use accounting information and make use of the published financial statements for analysis and evaluation.

General public:

From accounting information, the general public at large can get a view of the earning capacity and stability of the enterprise as well as the social responsibility measures undertaken by the enterprise particularly in its area of operation and also the employment opportunities provided to the local people.

![]()