Subject Matter Experts at SamacheerKalvi.Guide have created Tamil Nadu State Board Samacheer Kalvi 11th Books Answers Solutions Guide Pdf Free Download in English Medium and Tamil Medium are part of Samacheer Kalvi Books Solutions.

Let us look at these TN State Board New Syllabus Samacheer Kalvi 11th Std Guide Pdf of Text Book Back Questions and Answers of Volume 1 and Volume 2, Chapter Wise Important Questions, Study Material, Question Bank, Notes, Formulas and revise our understanding of the subject.

Students can also read Tamil Nadu Samacheer Kalvi 11th Model Question Papers 2020-2021.

Tamilnadu Samacheer Kalvi 11th Guide Text Book Back Answers Solutions Pdf Free Download

TN Samacheer Kalvi 11th Book Back Answers Solutions Guide

- Samacheer Kalvi 11th Maths Guide

- Samacheer Kalvi 11th Physics Guide

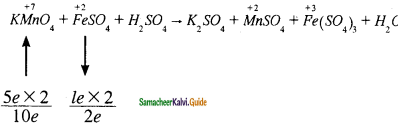

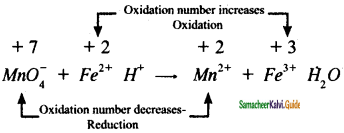

- Samacheer Kalvi 11th Chemistry Guide

- Samacheer Kalvi 11th Biology Guide

- Samacheer Kalvi 11th Bio Botany Guide

- Samacheer Kalvi 11th Bio Zoology Guide

- Samacheer Kalvi 11th Tamil Guide

- Samacheer Kalvi 11th English Guide

- Samacheer Kalvi 11th History Guide

- Samacheer Kalvi 11th Commerce Guide

- Samacheer Kalvi 11th Accountancy Guide

- Samacheer Kalvi 11th Economics Guide

- Samacheer Kalvi 11th Business Maths Guide

- Samacheer Kalvi 11th Computer Science Guide

- Samacheer Kalvi 11th Computer Applications Guide

We hope these Tamilnadu State Board Samacheer Kalvi Class 11th Std Books Solutions Answers Guide Pdf Free Download in English Medium and Tamil Medium will help you get through your subjective questions in the exam.

Let us know if you have any concerns regarding TN State Board New Syllabus Samacheer Kalvi 11th Standard Guides Pdf of Text Book Back Questions and Answers of Volume 1 and Volume 2, Chapter Wise Important Questions, Study Material, Question Bank, Notes, Formulas, drop a comment below and we will get back to you as soon as possible.

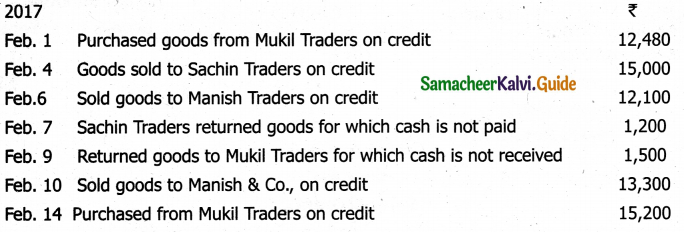

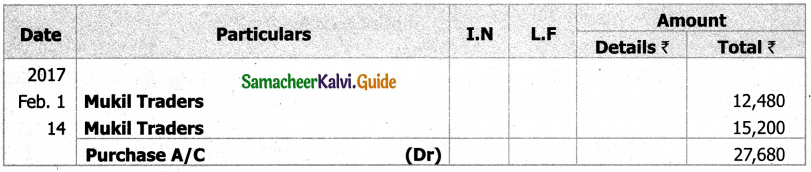

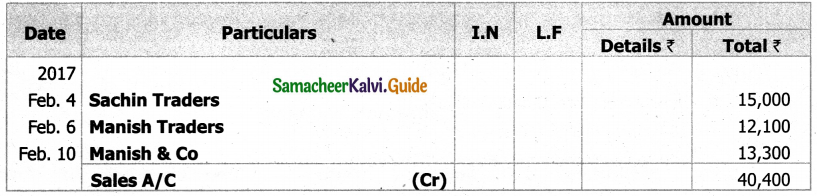

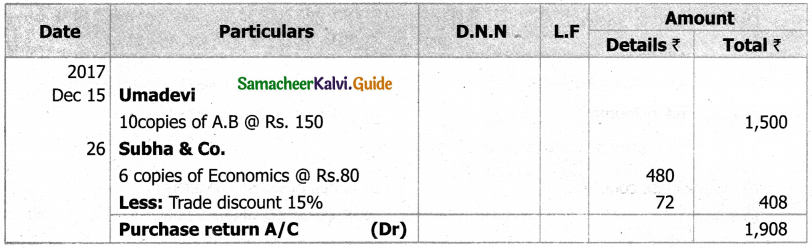

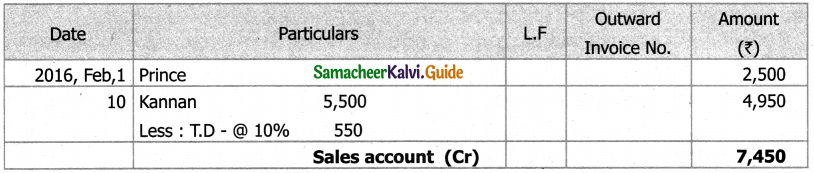

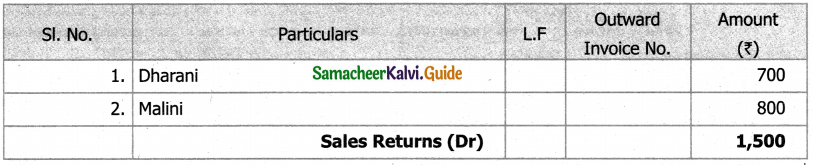

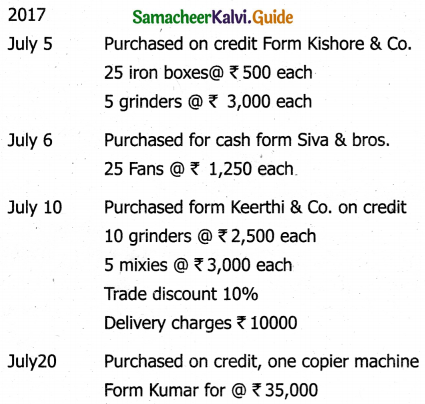

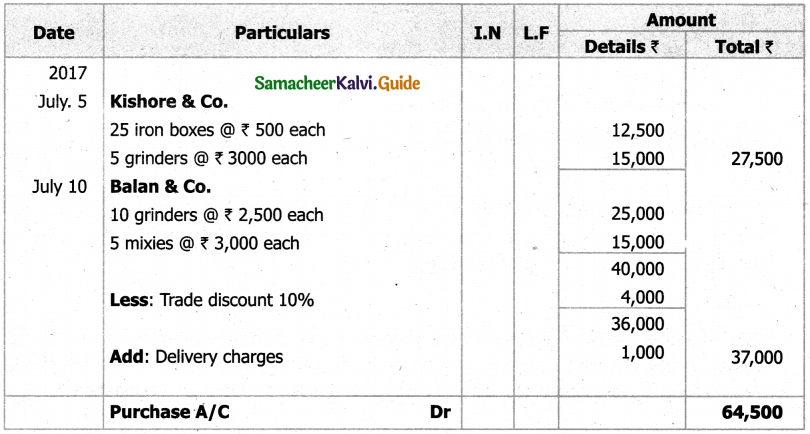

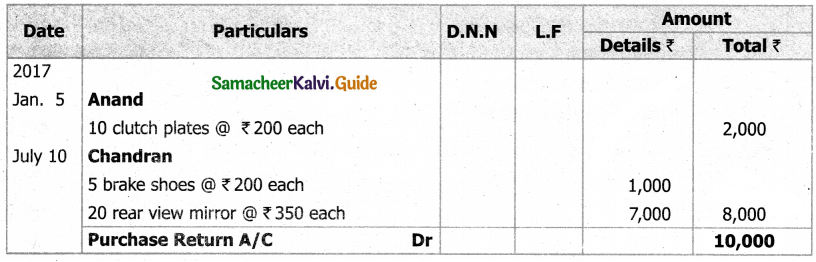

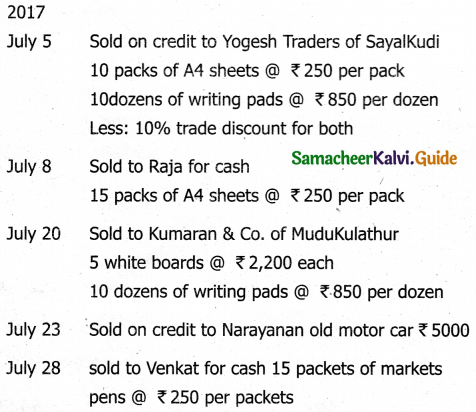

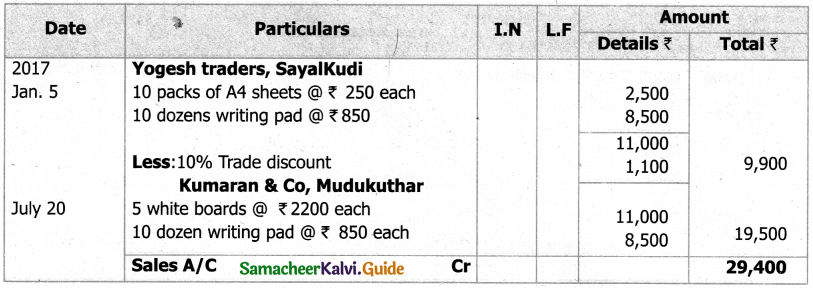

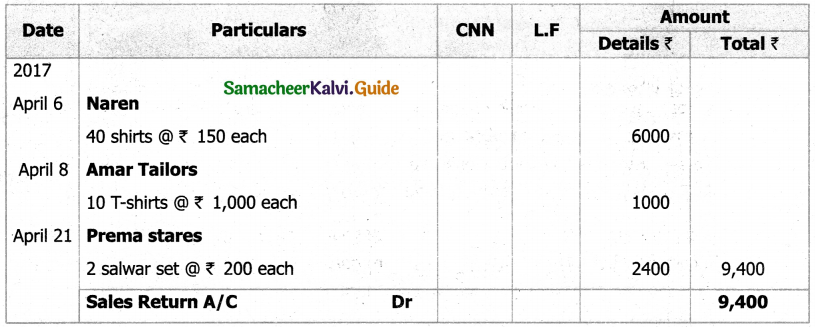

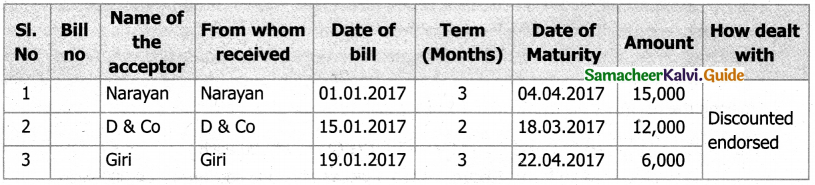

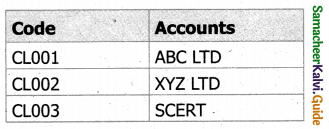

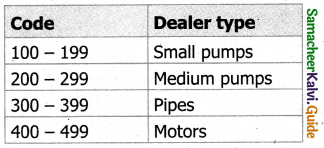

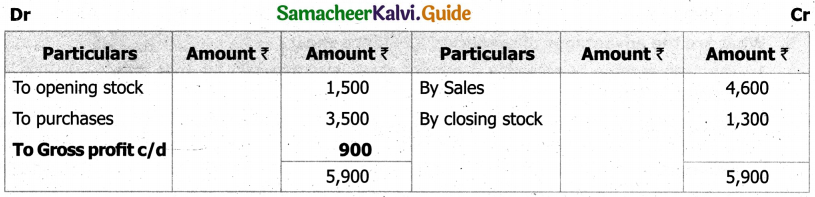

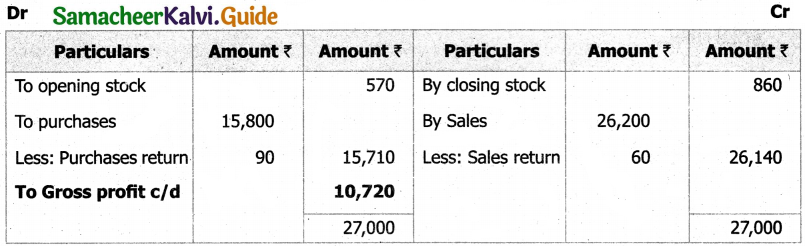

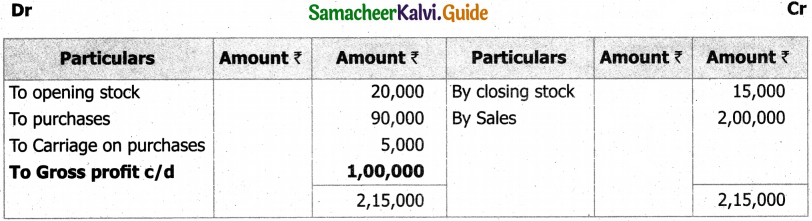

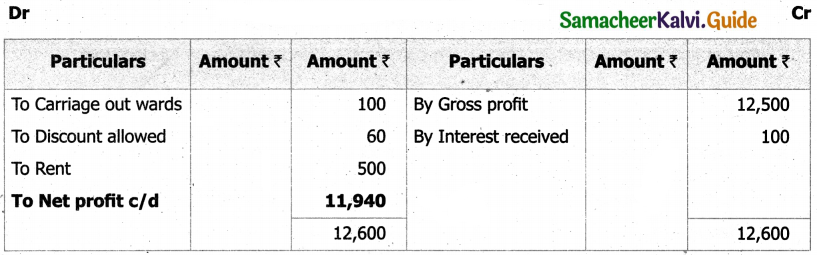

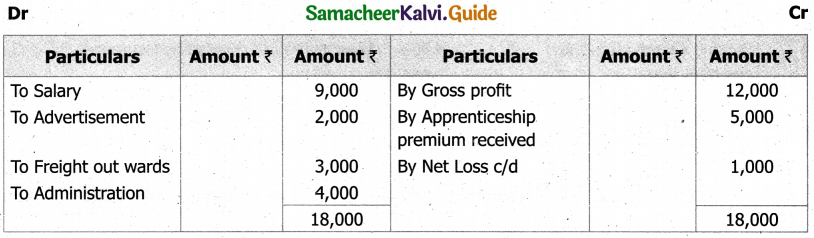

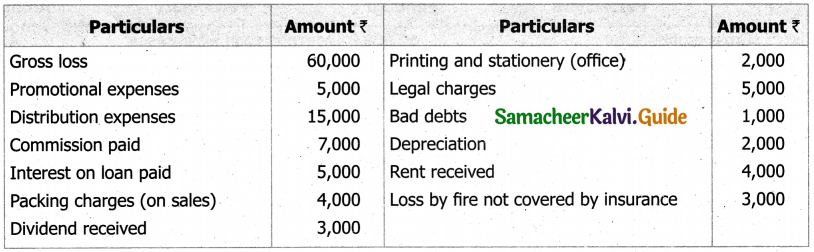

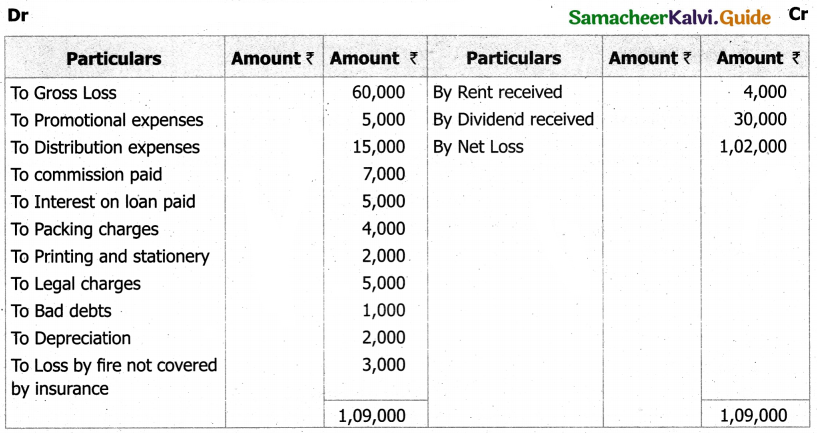

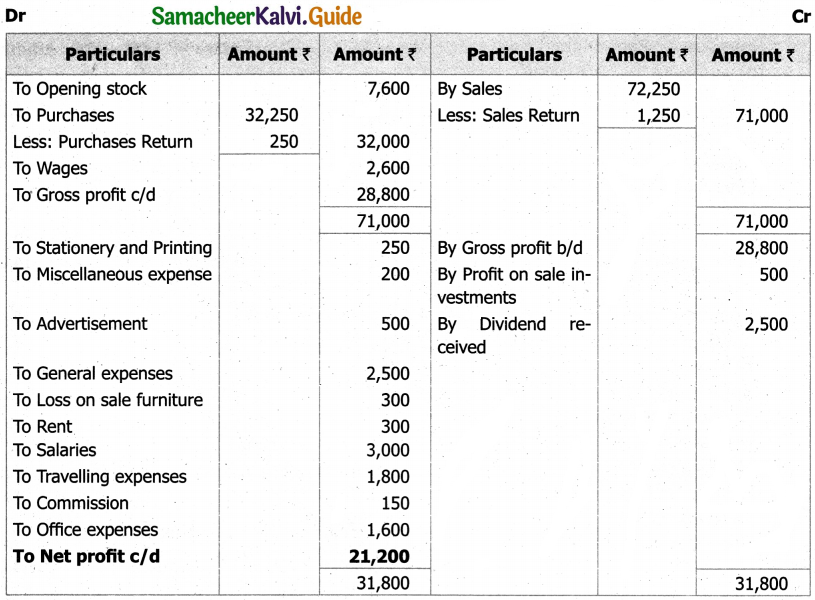

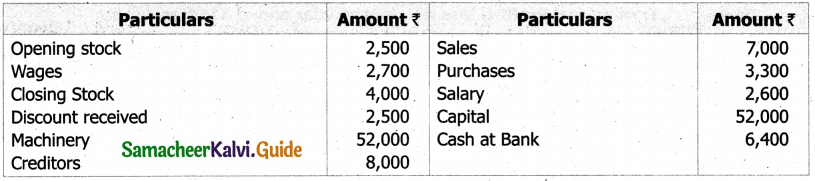

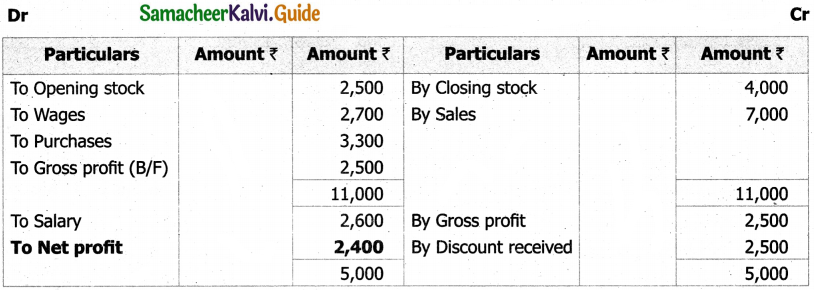

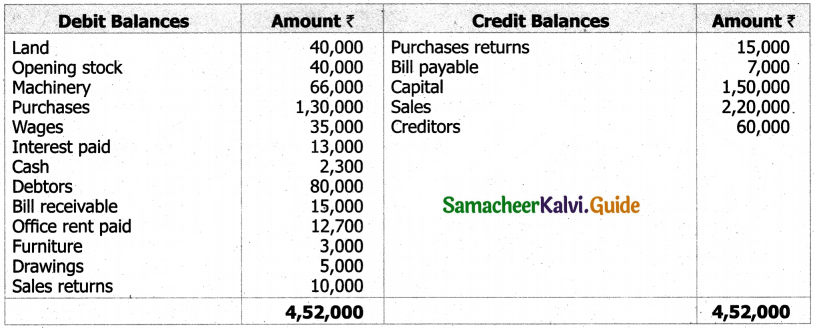

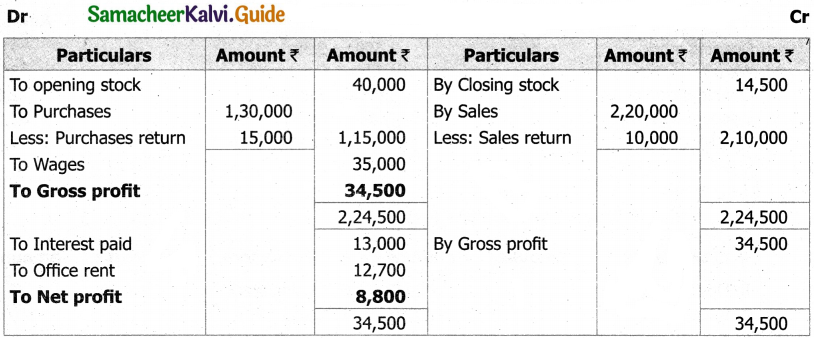

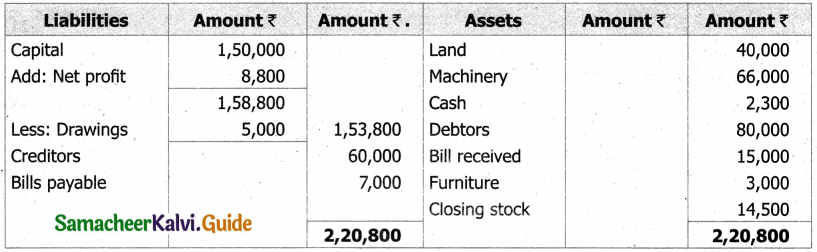

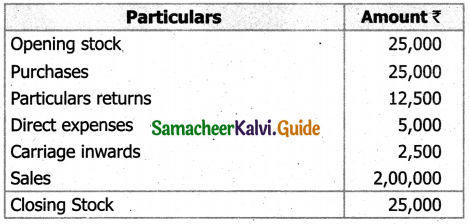

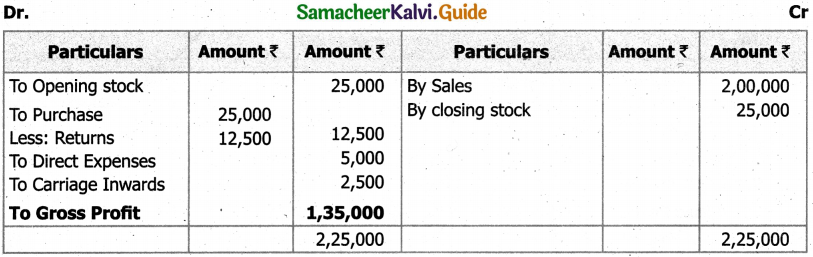

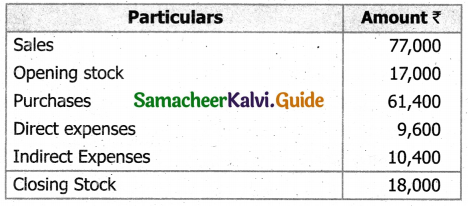

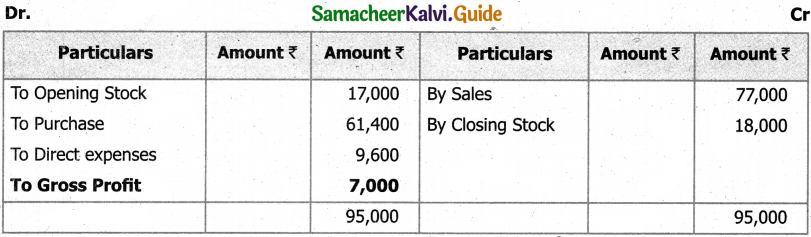

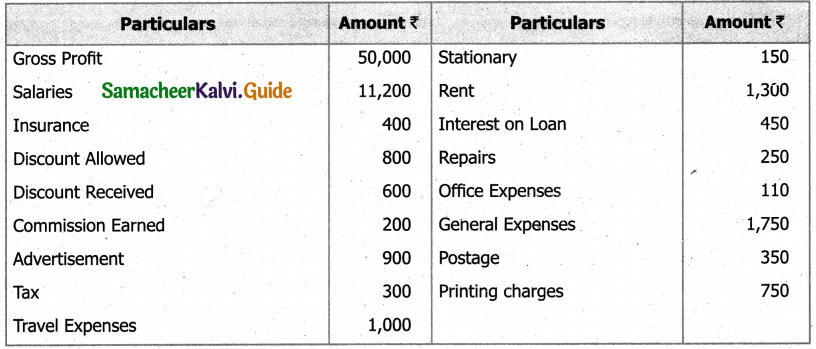

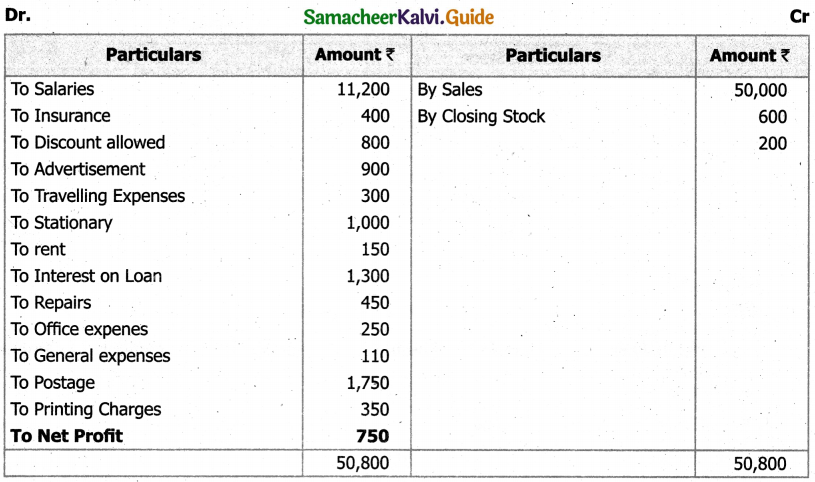

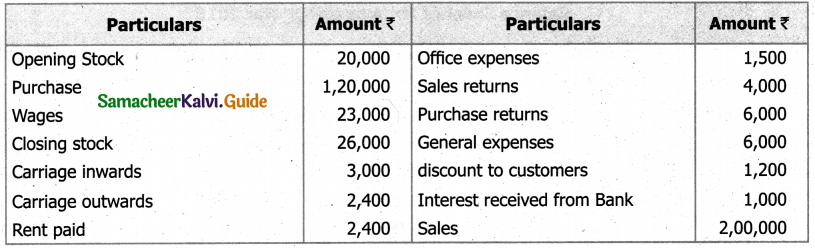

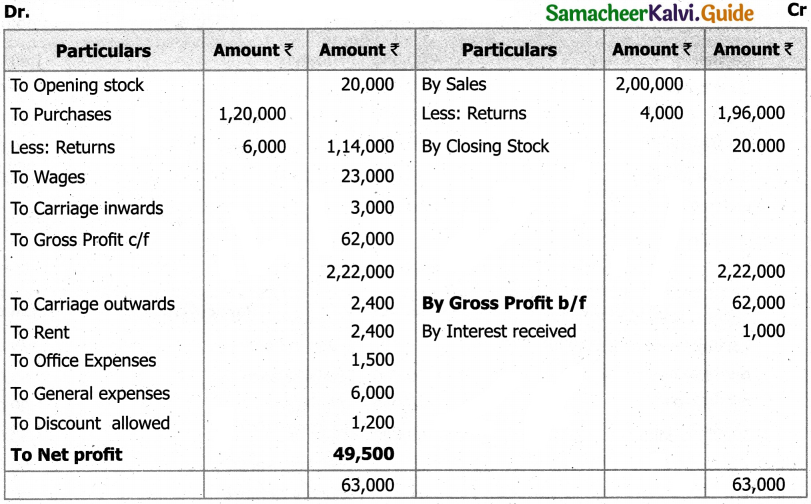

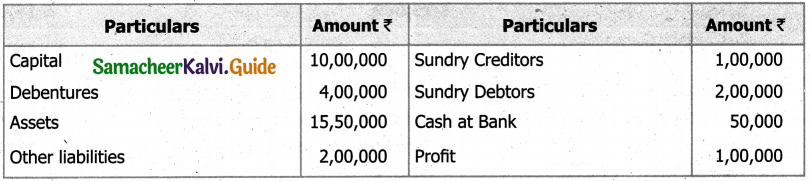

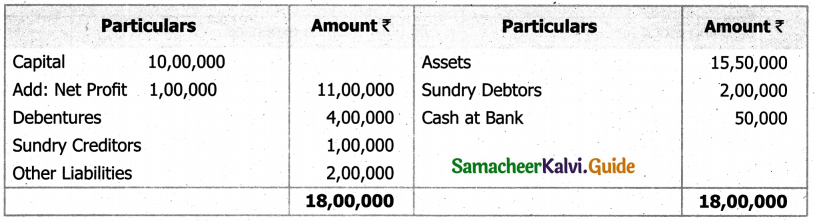

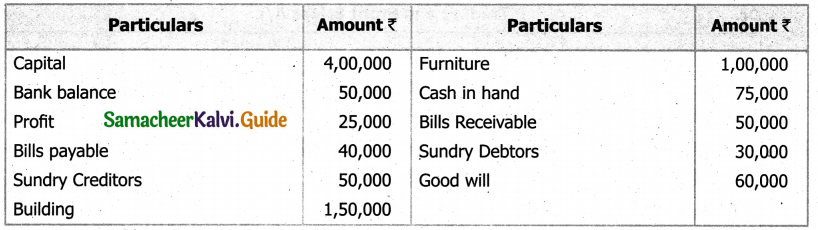

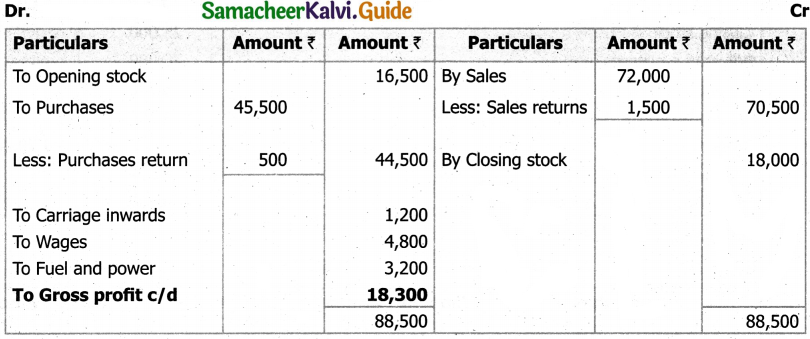

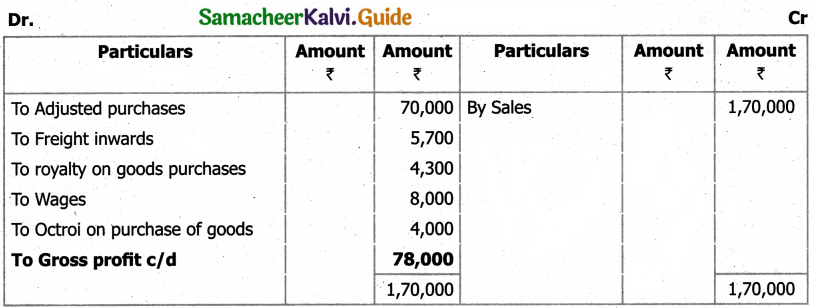

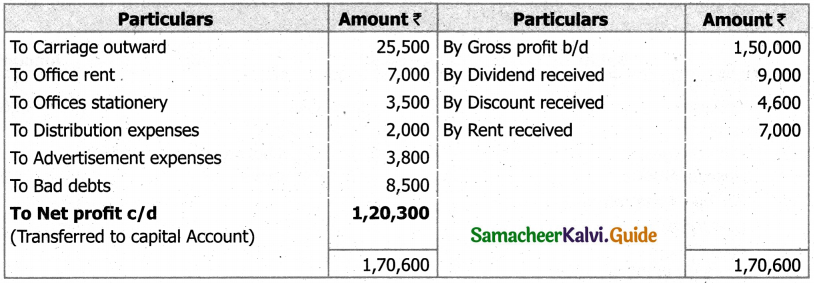

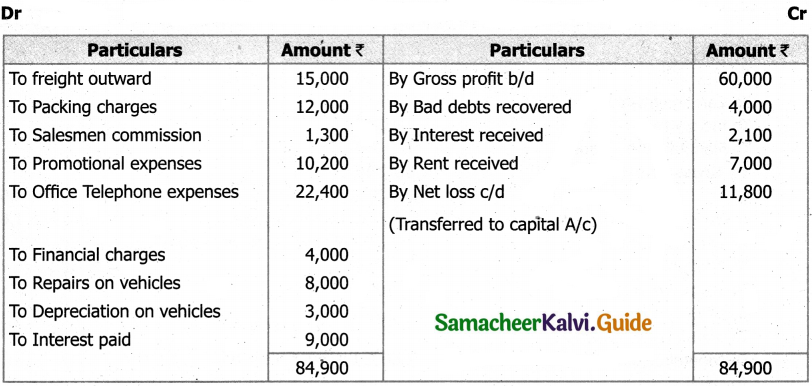

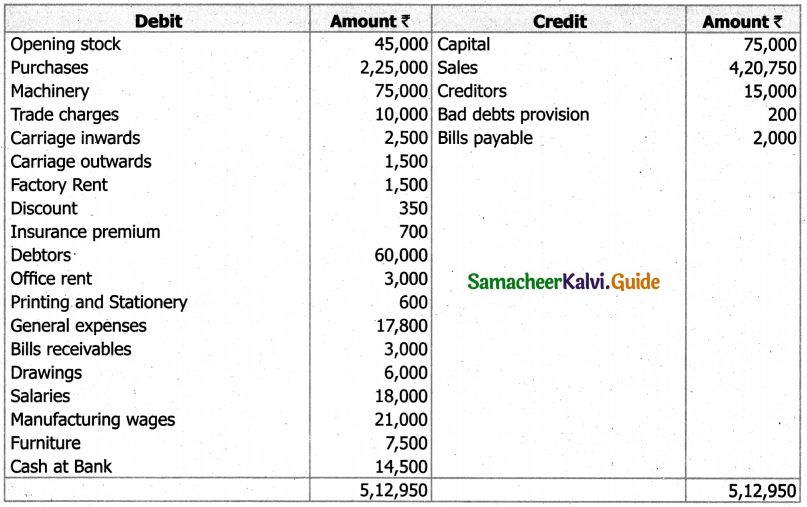

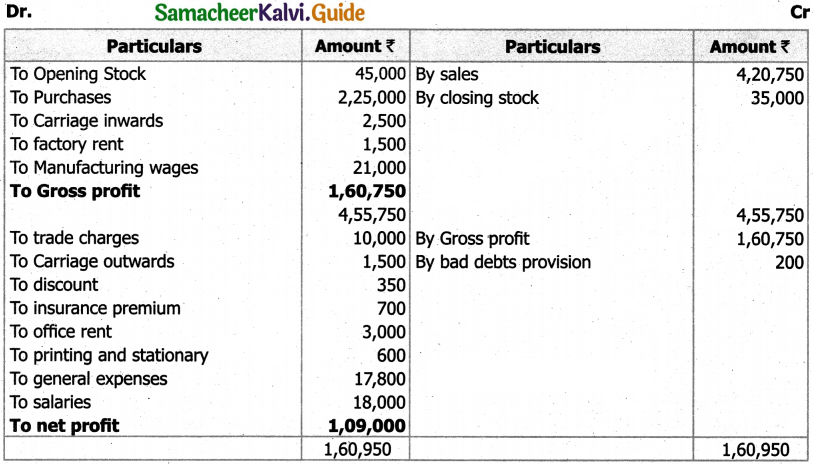

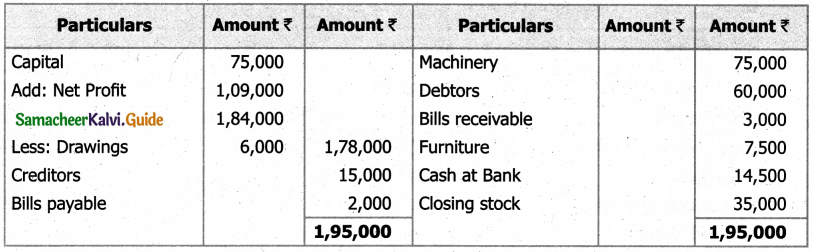

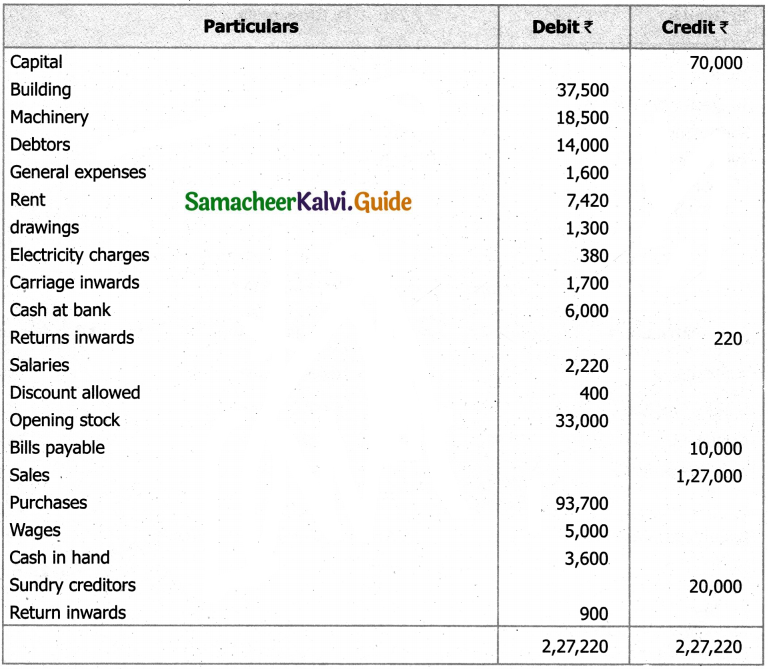

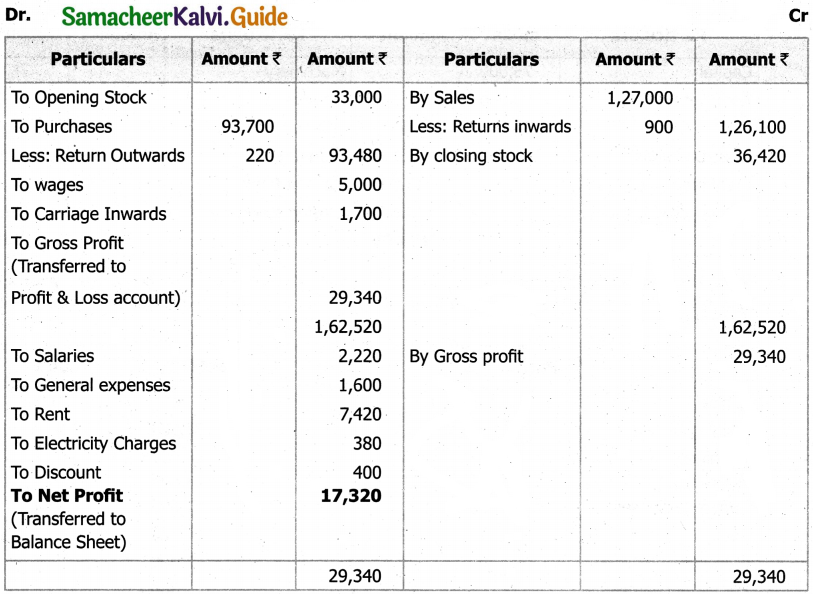

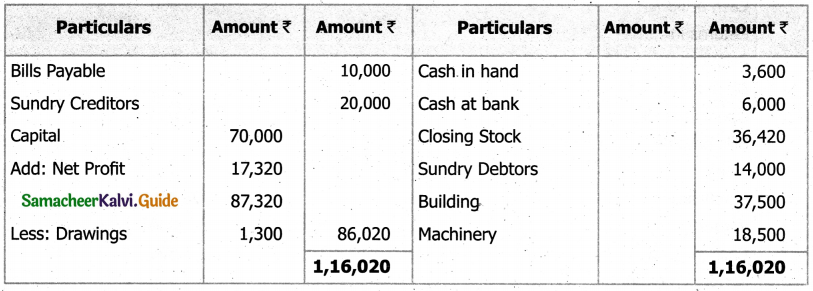

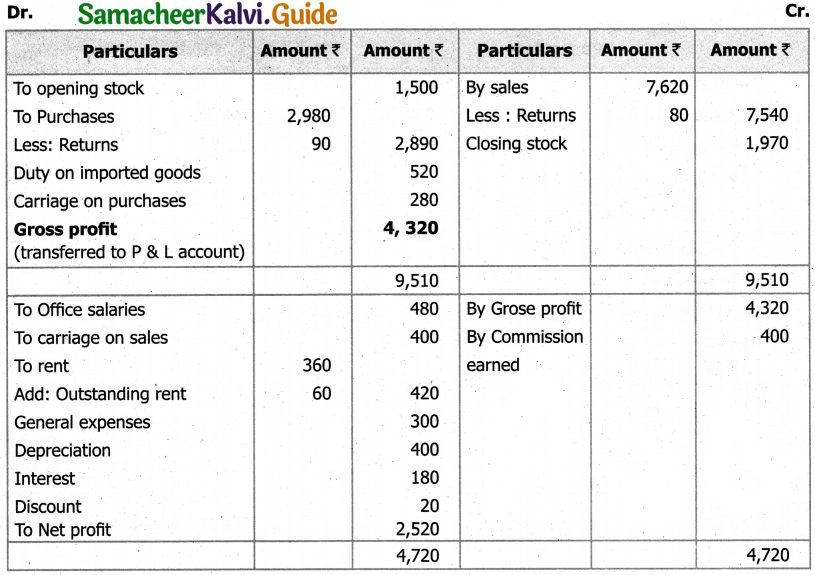

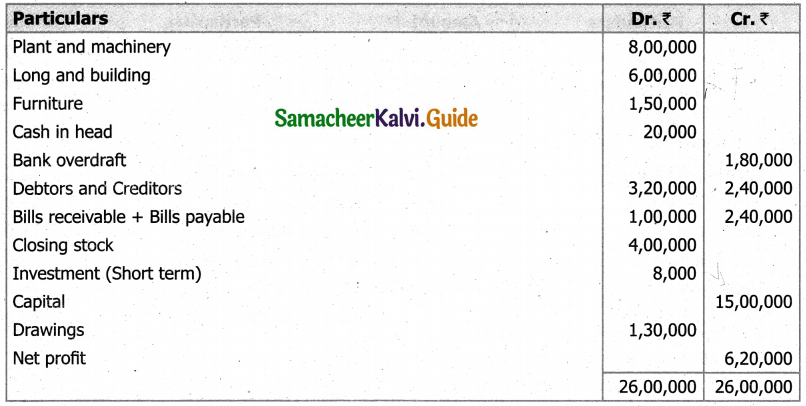

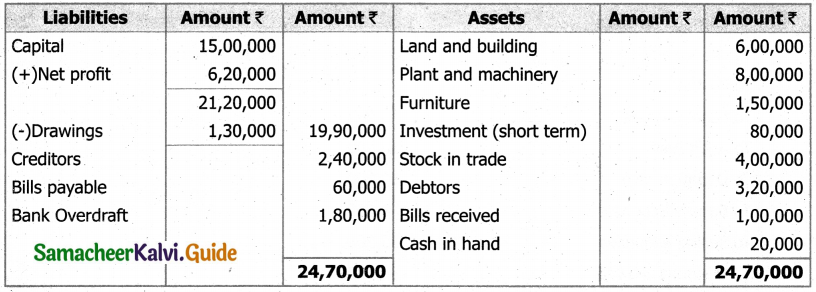

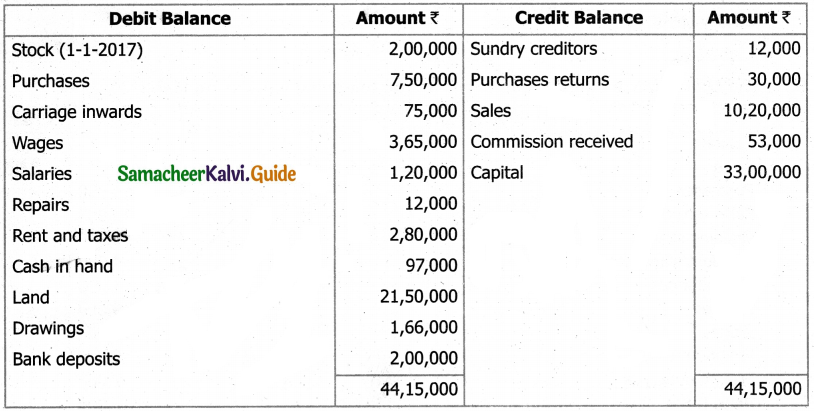

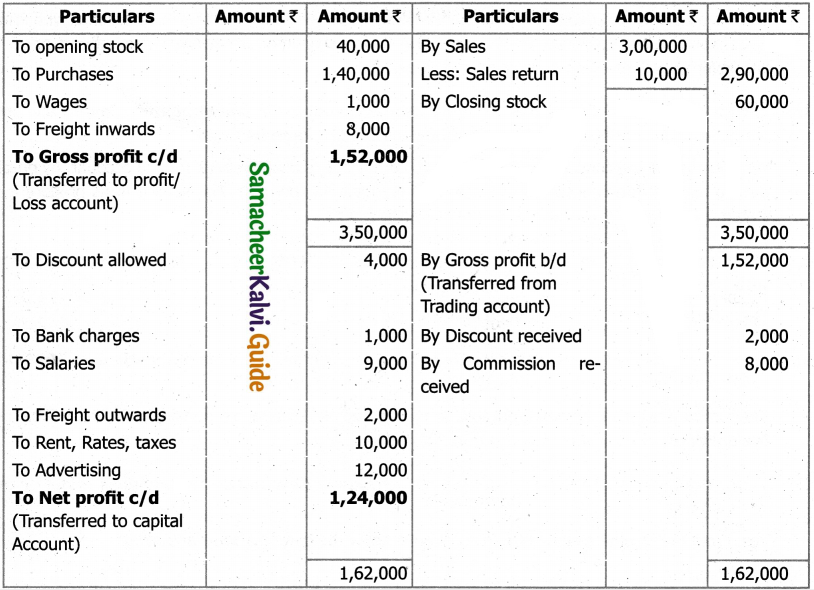

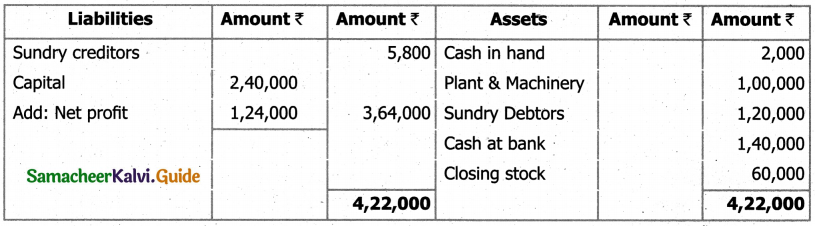

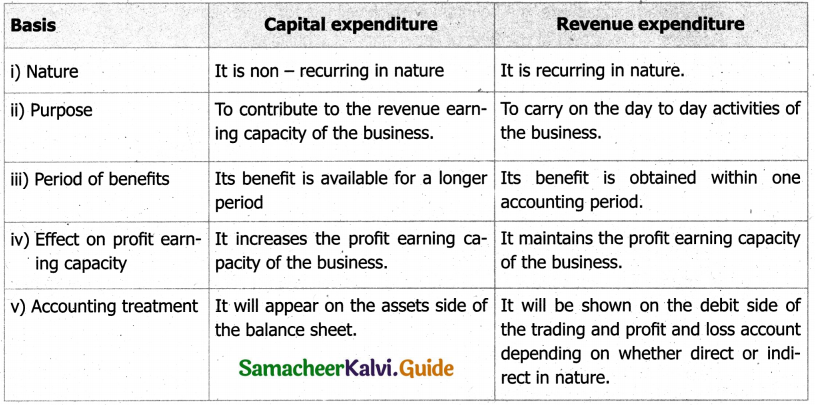

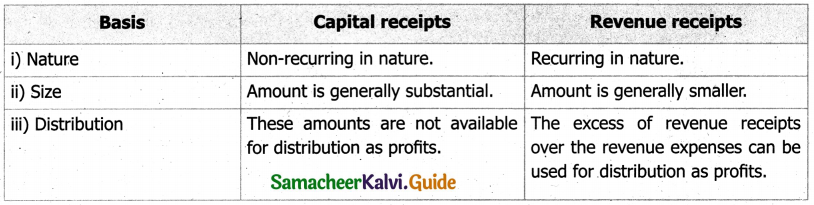

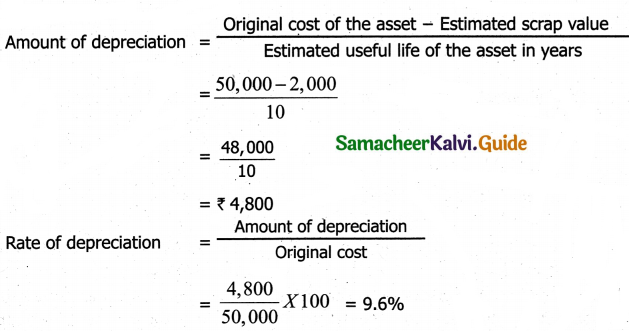

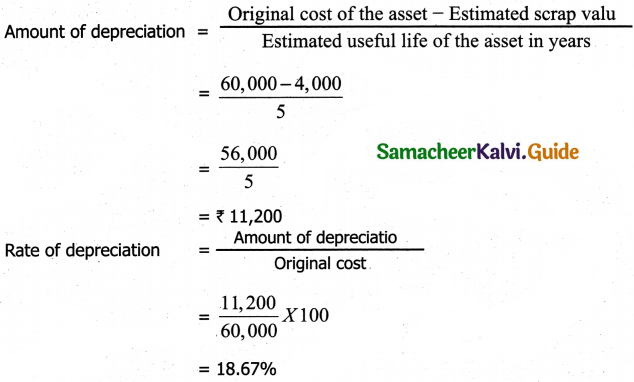

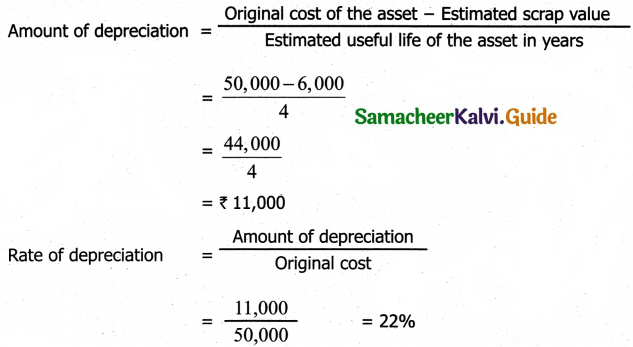

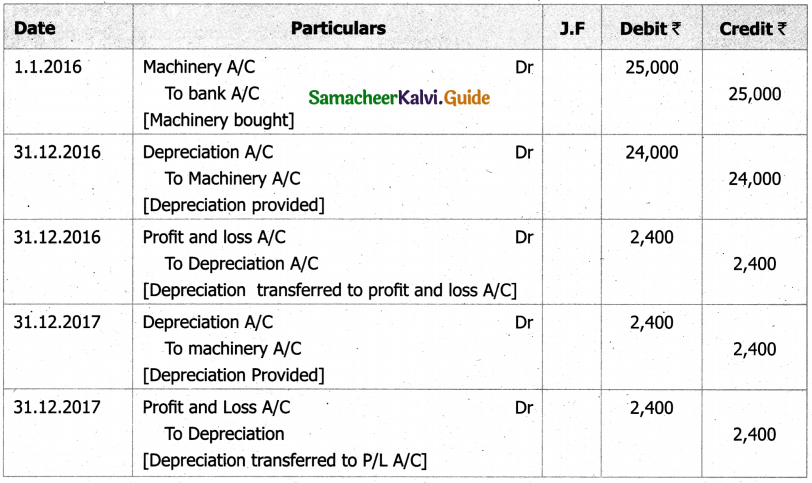

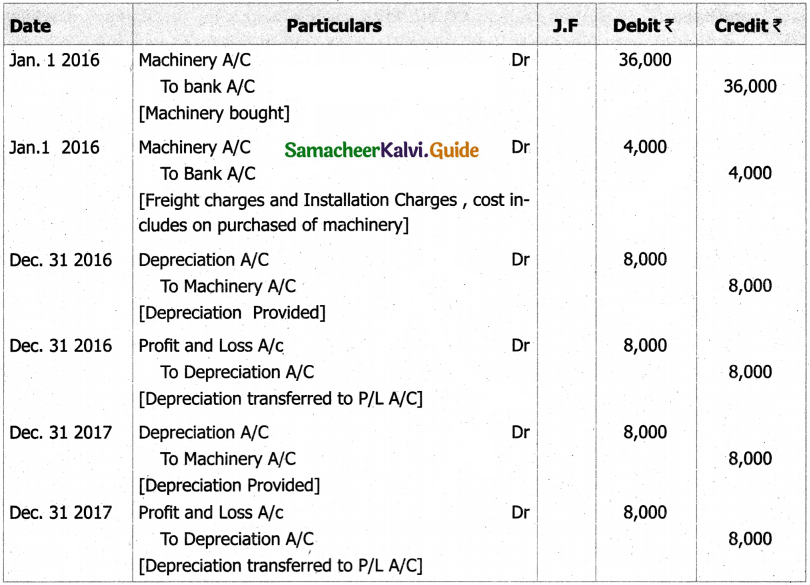

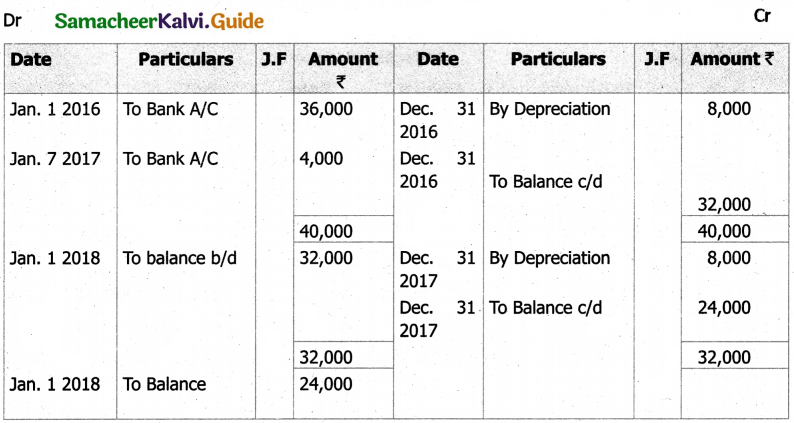

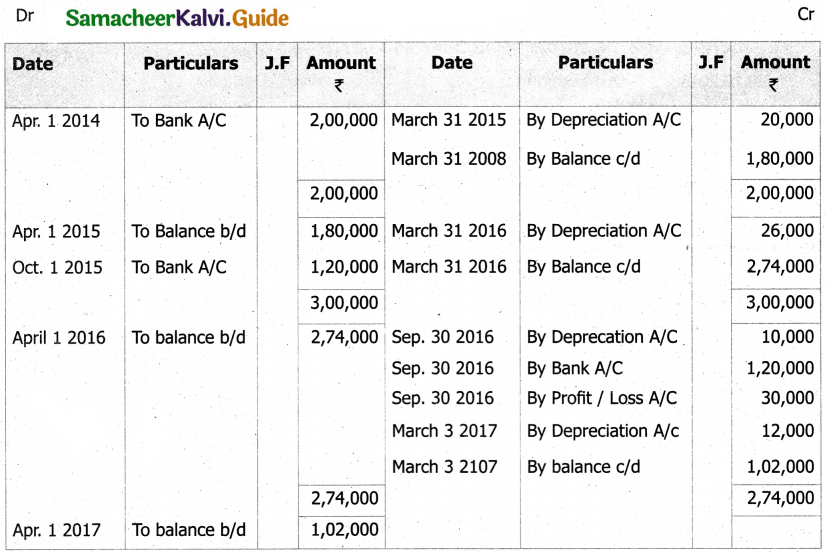

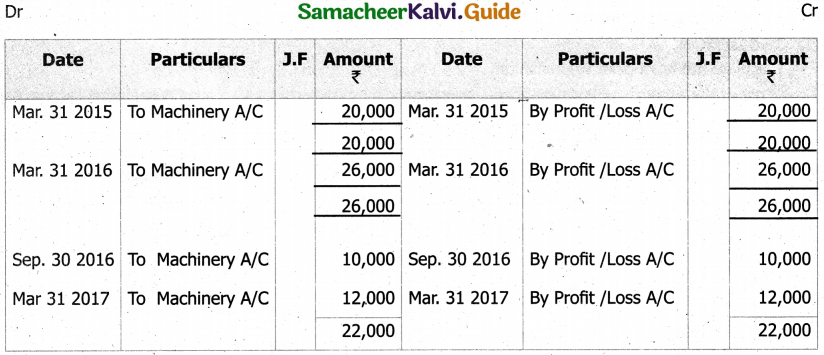

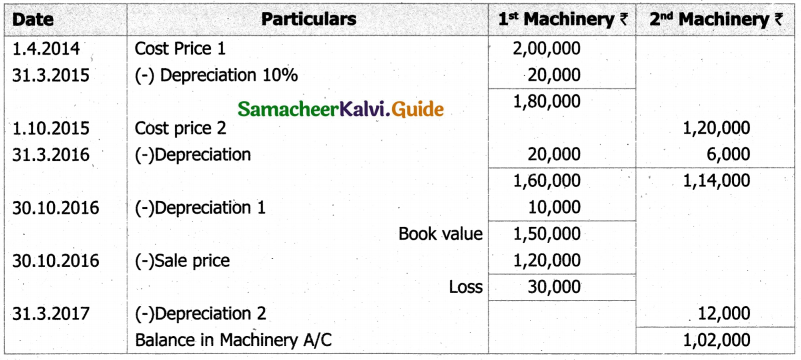

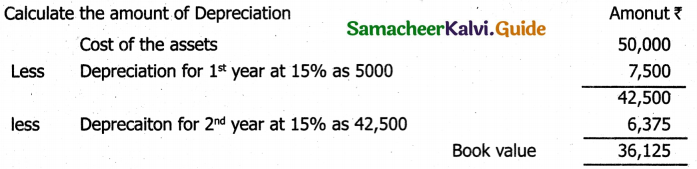

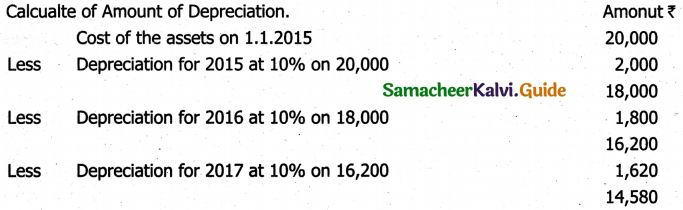

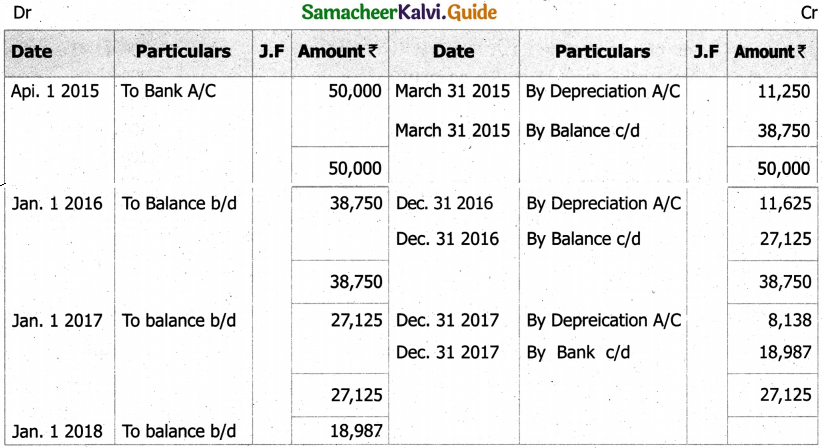

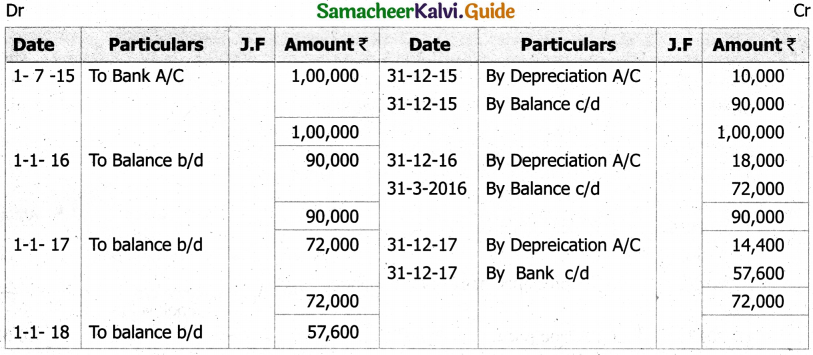

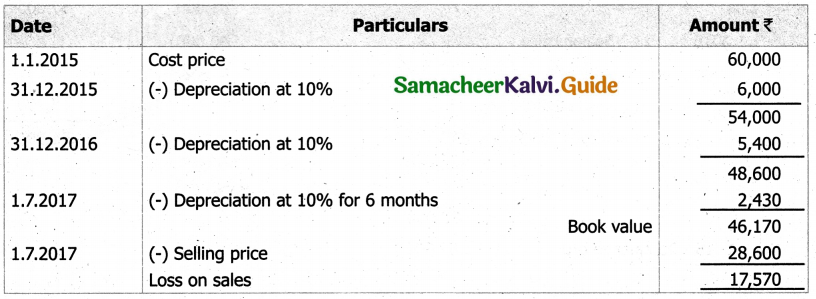

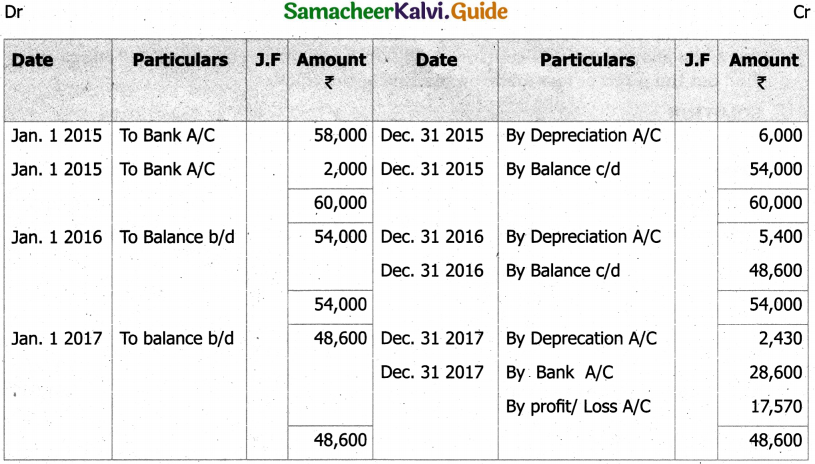

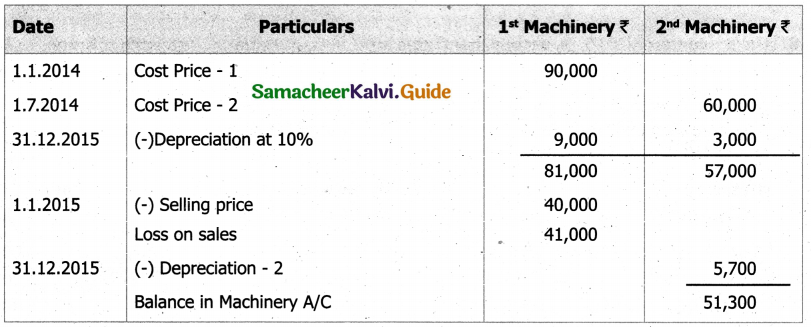

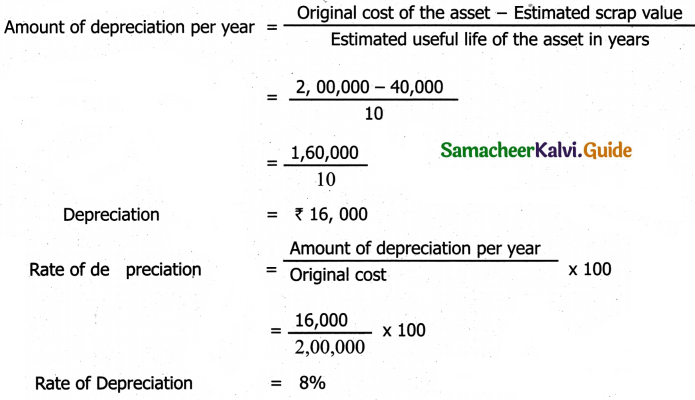

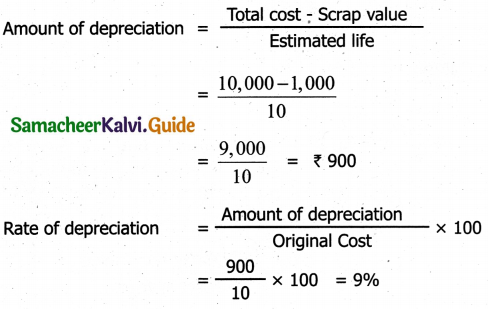

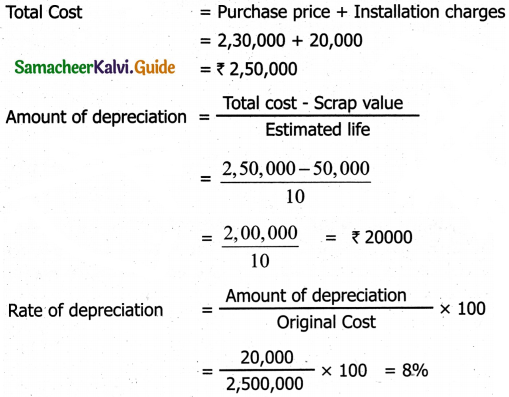

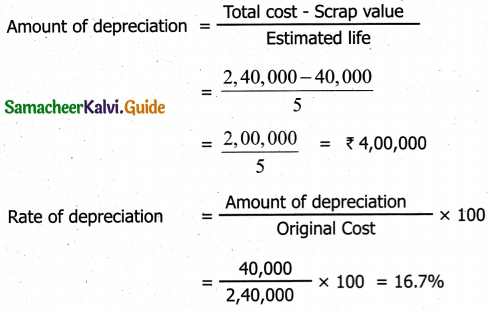

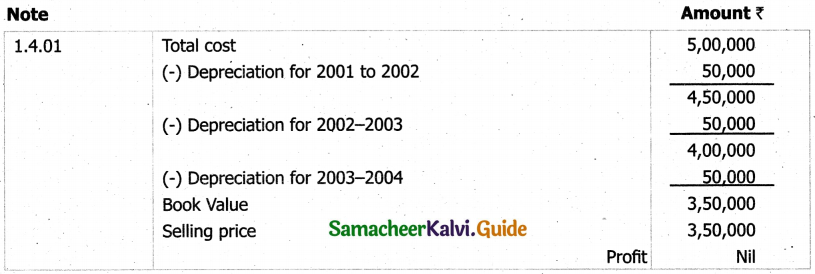

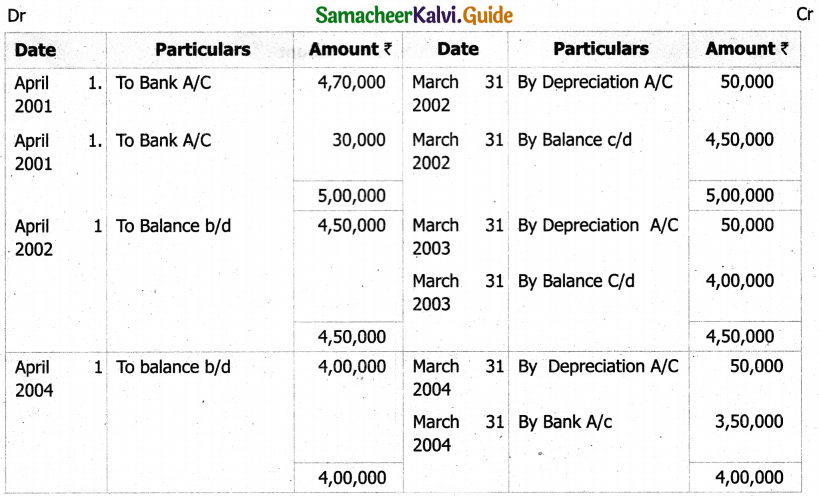

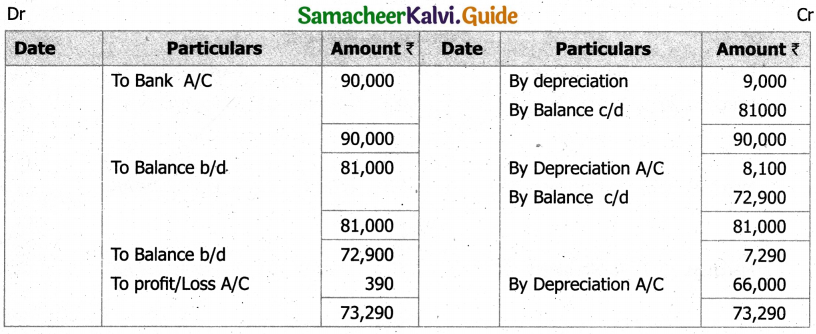

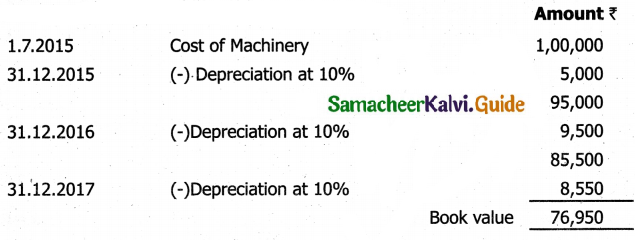

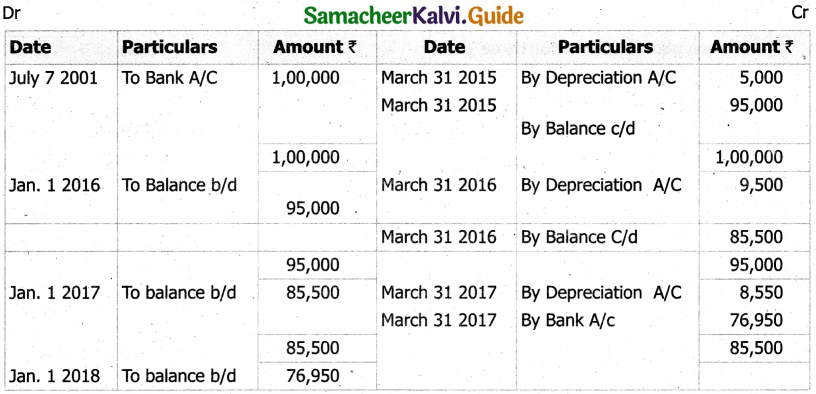

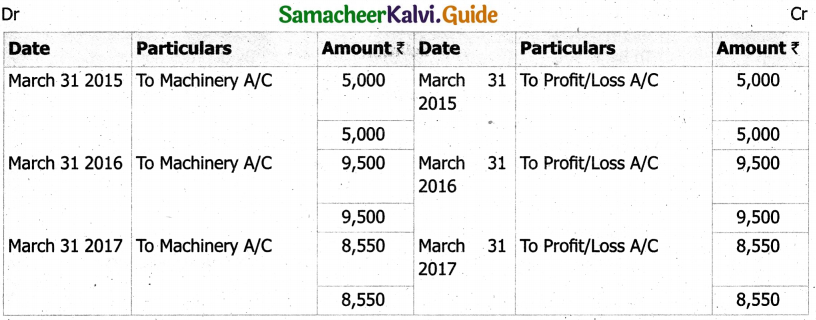

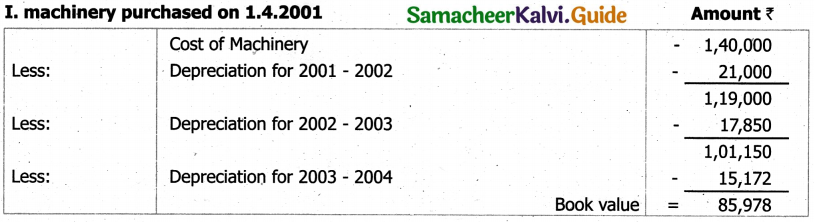

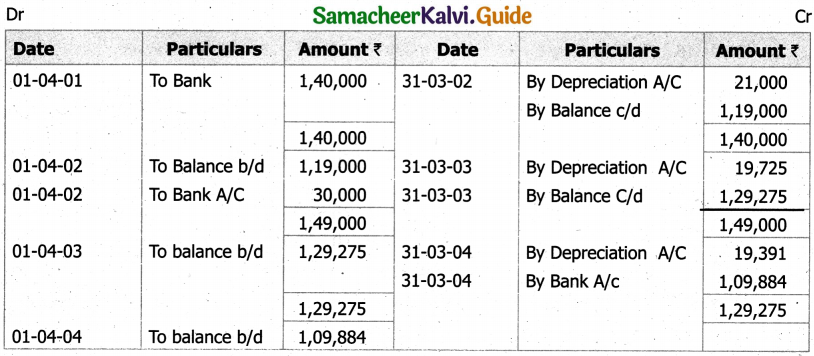

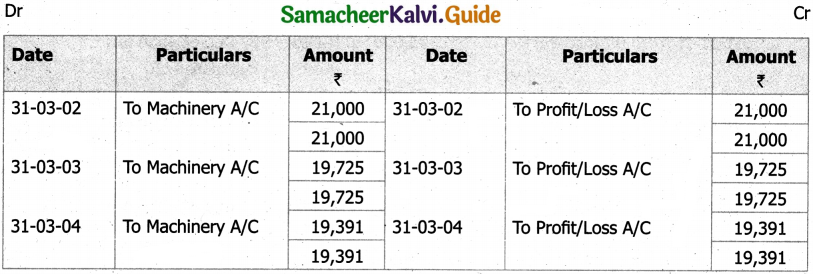

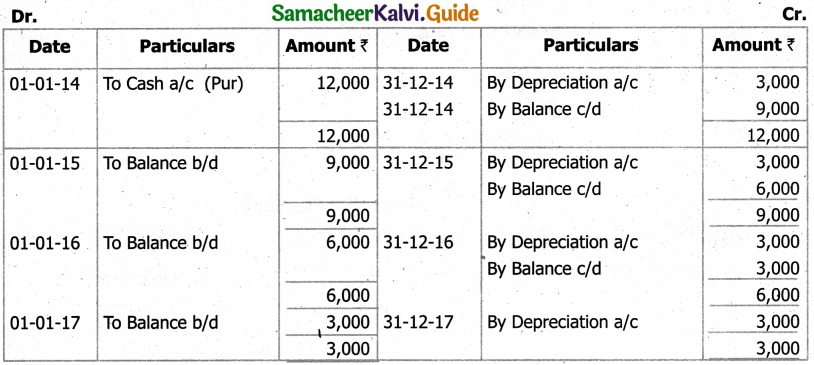

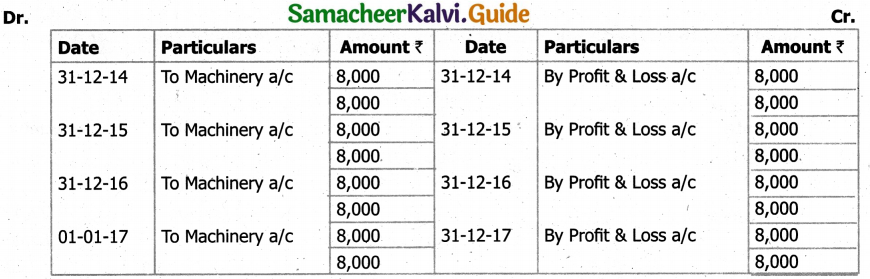

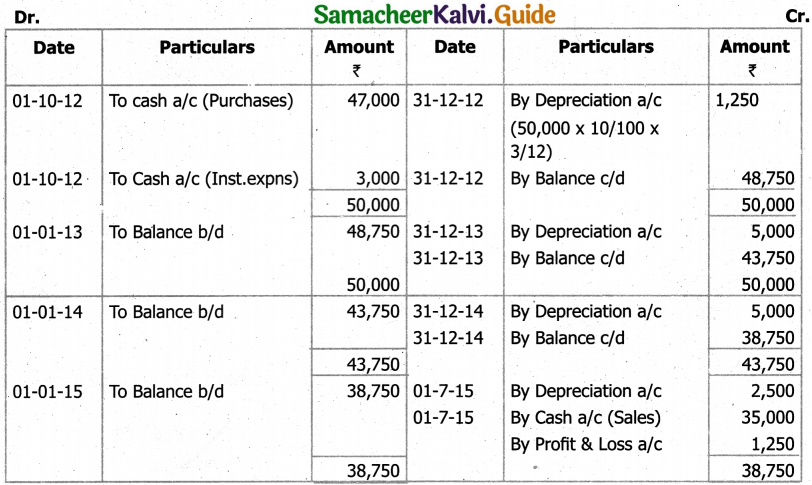

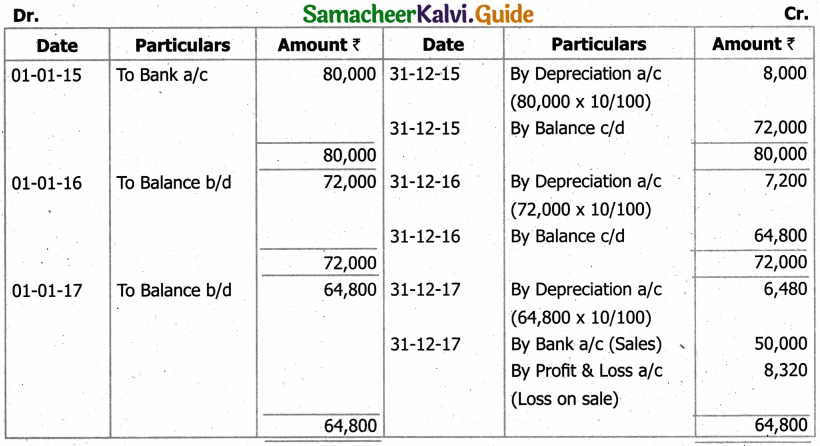

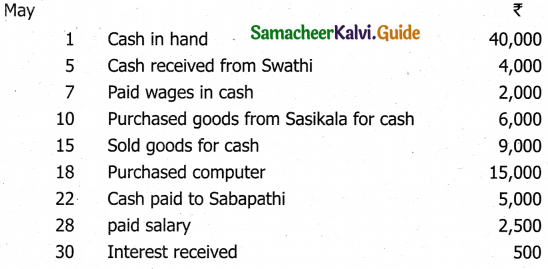

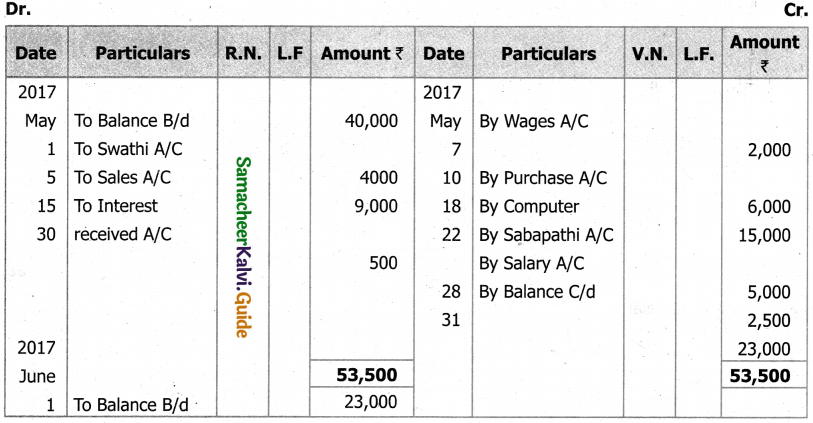

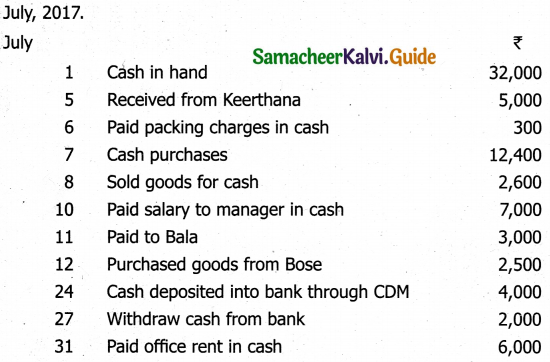

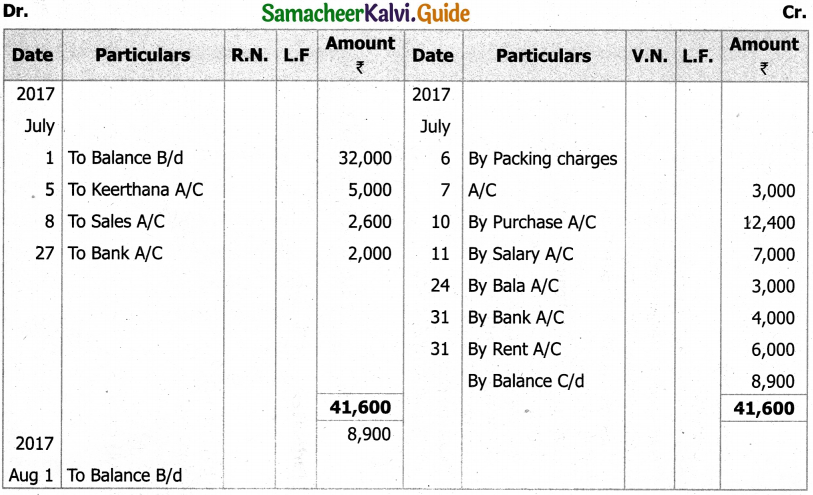

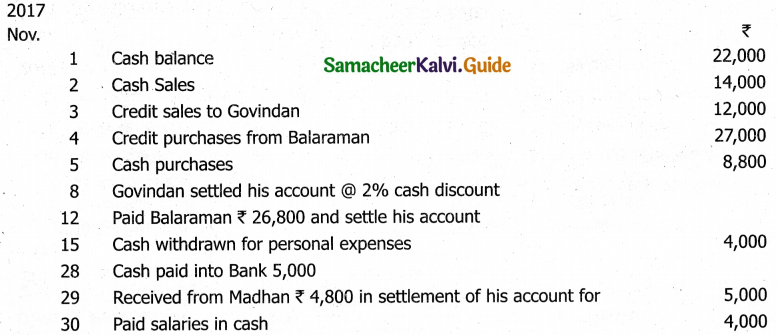

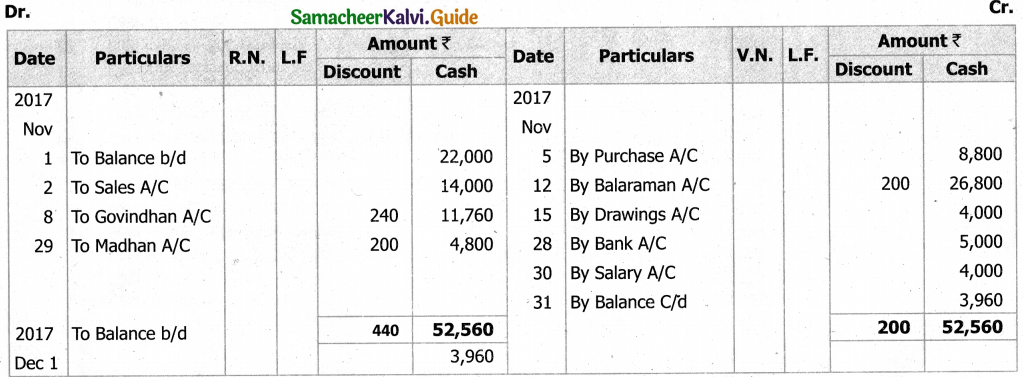

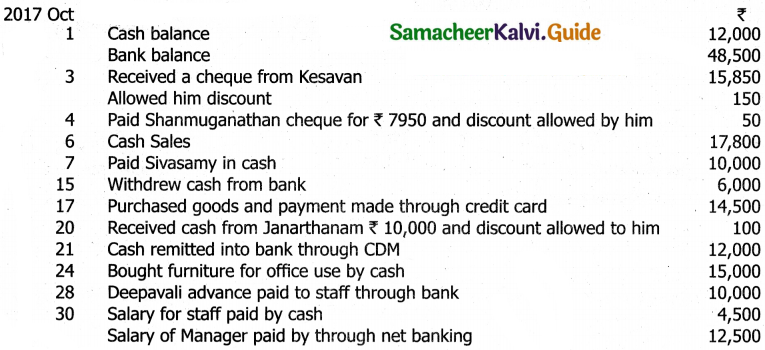

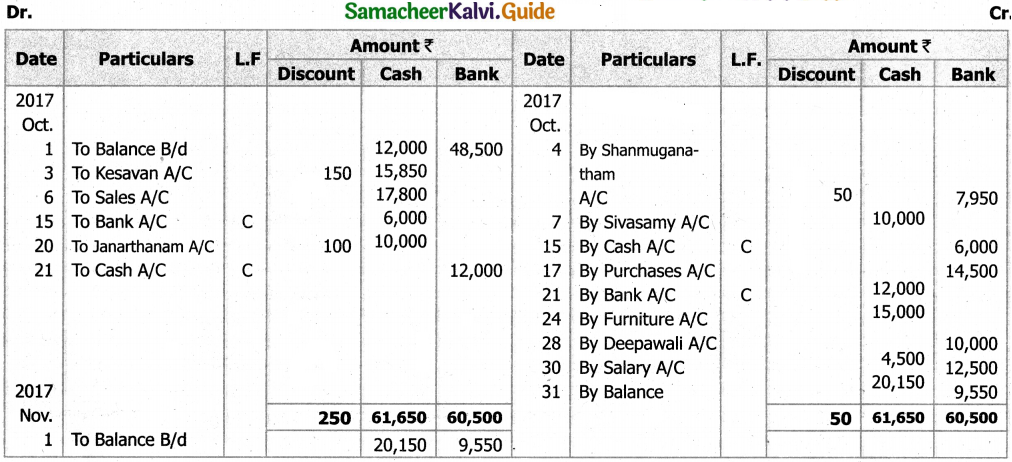

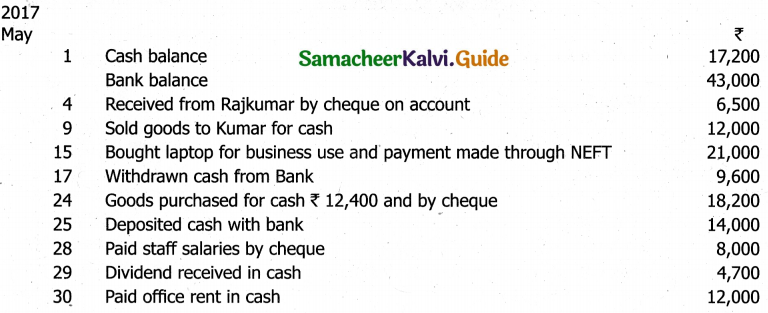

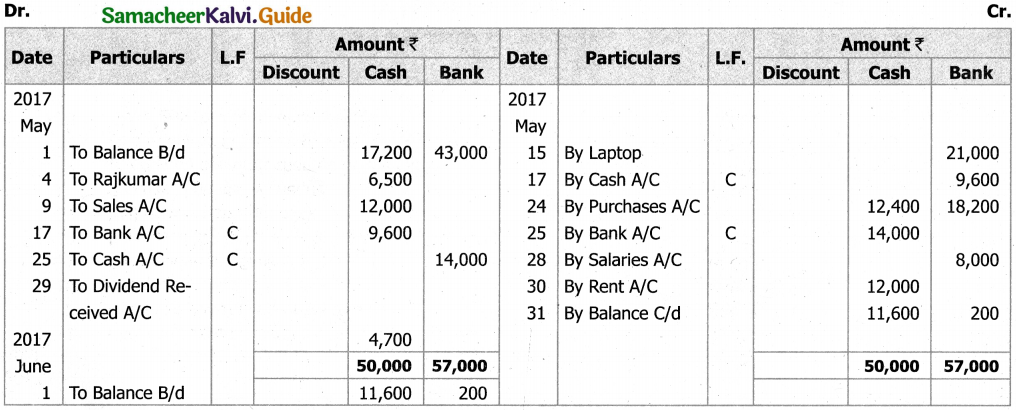

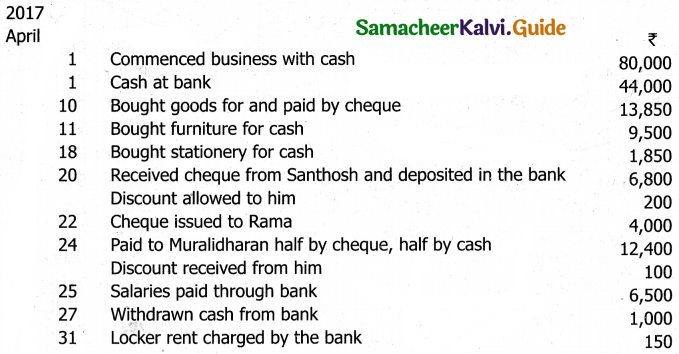

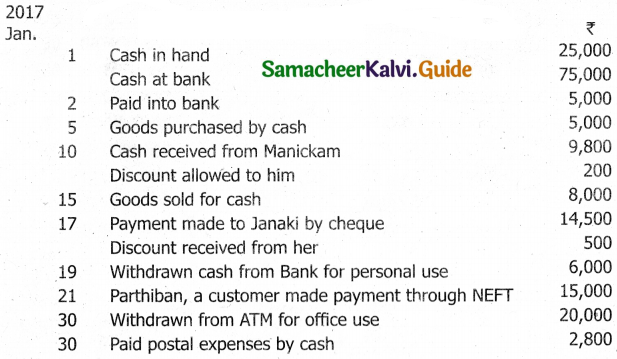

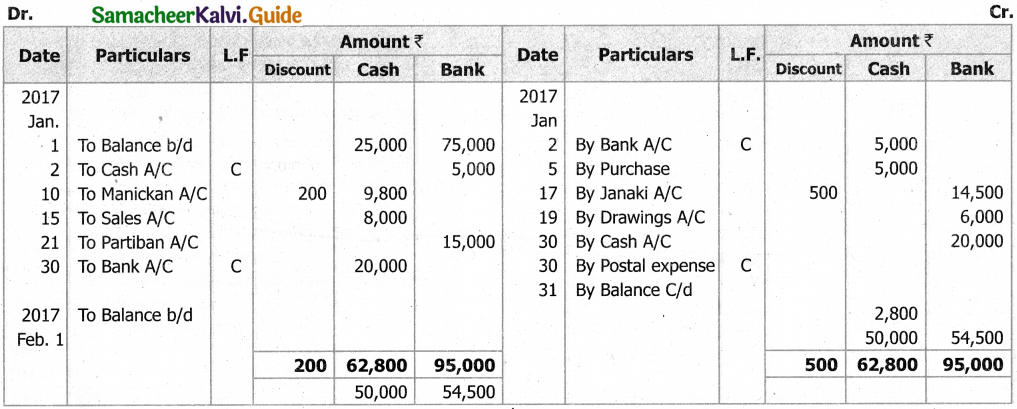

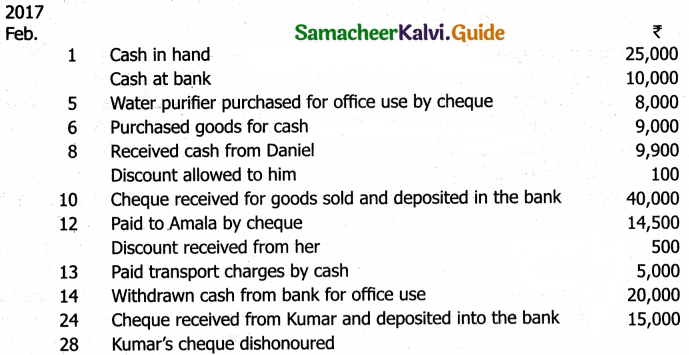

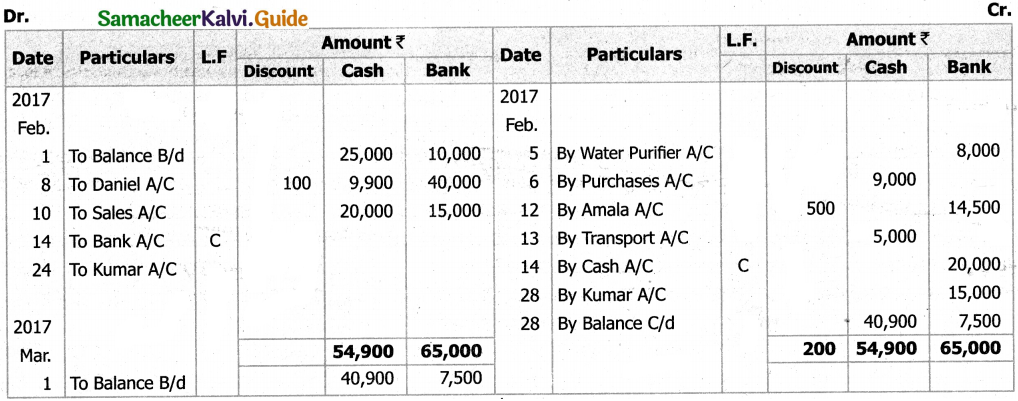

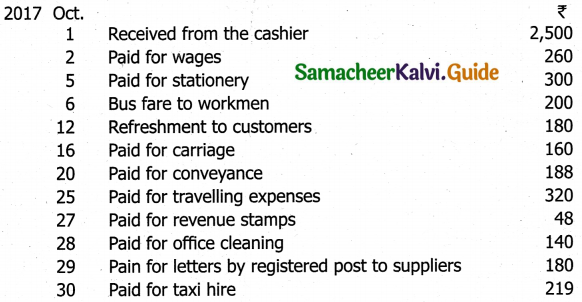

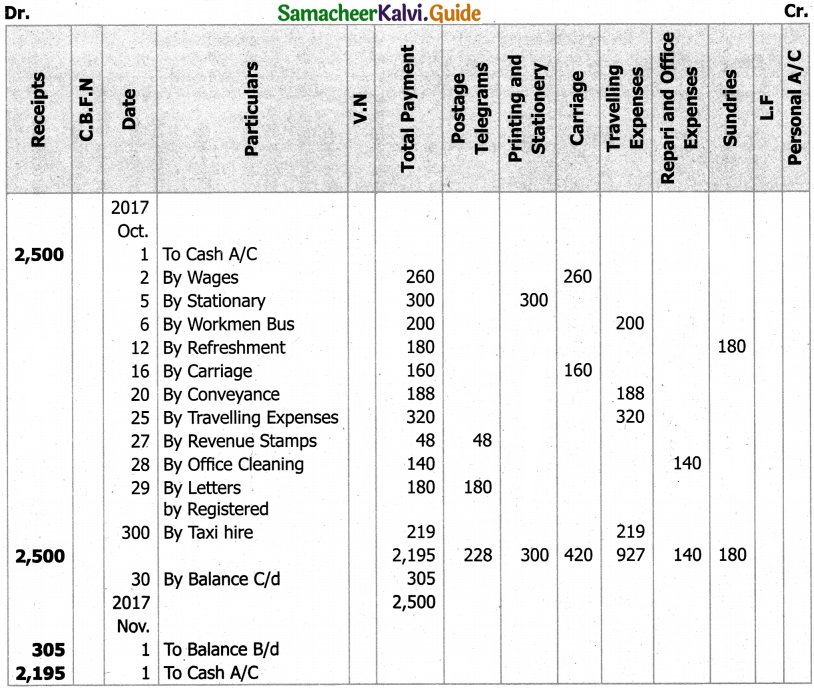

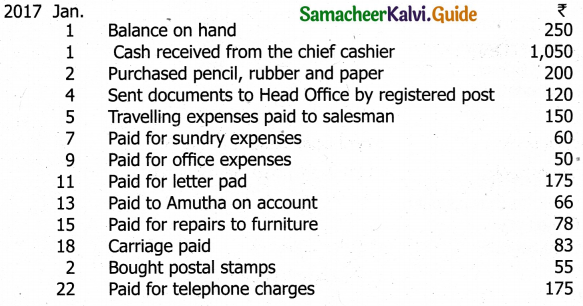

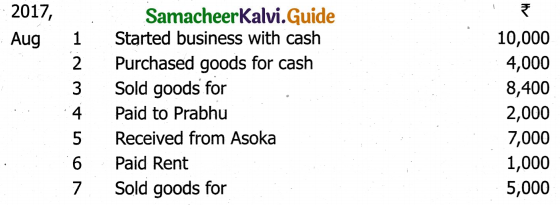

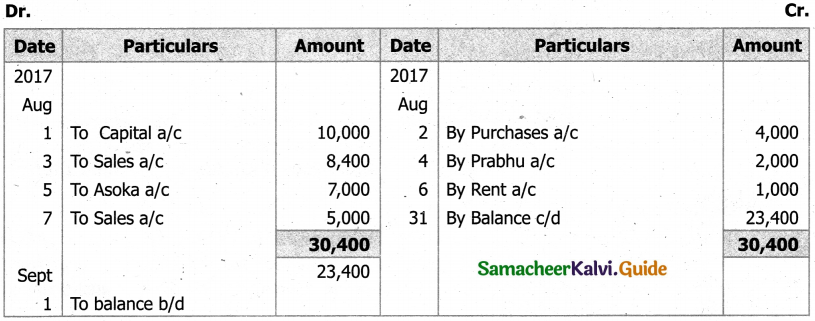

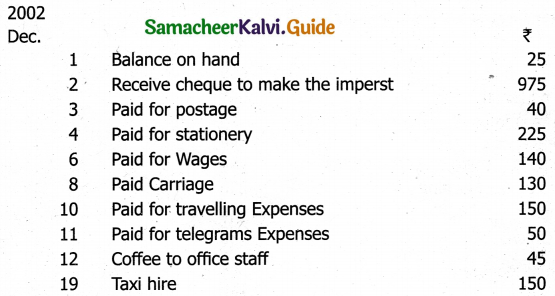

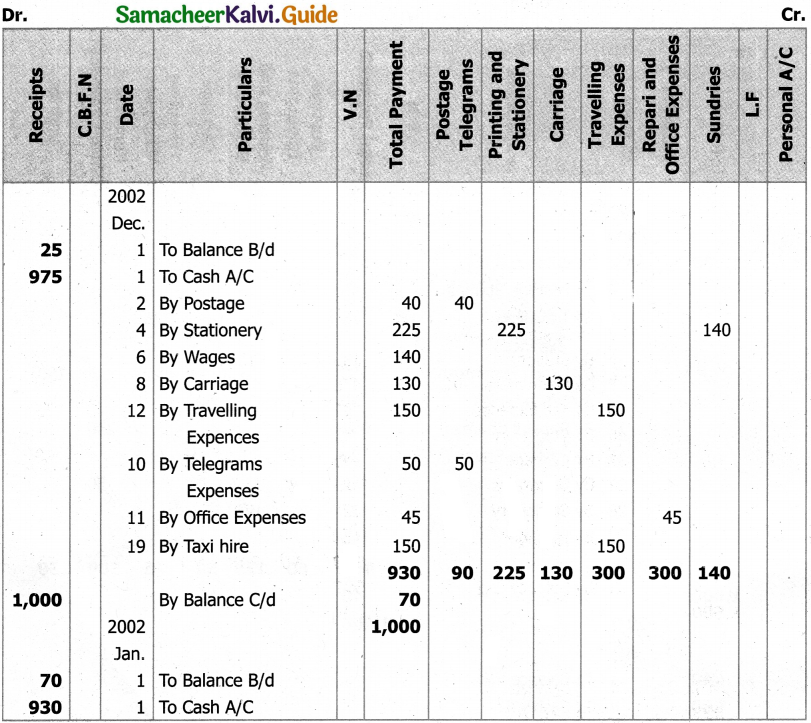

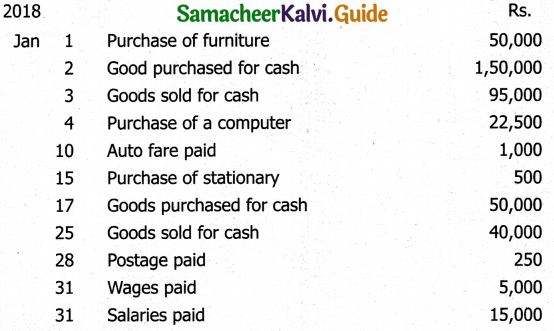

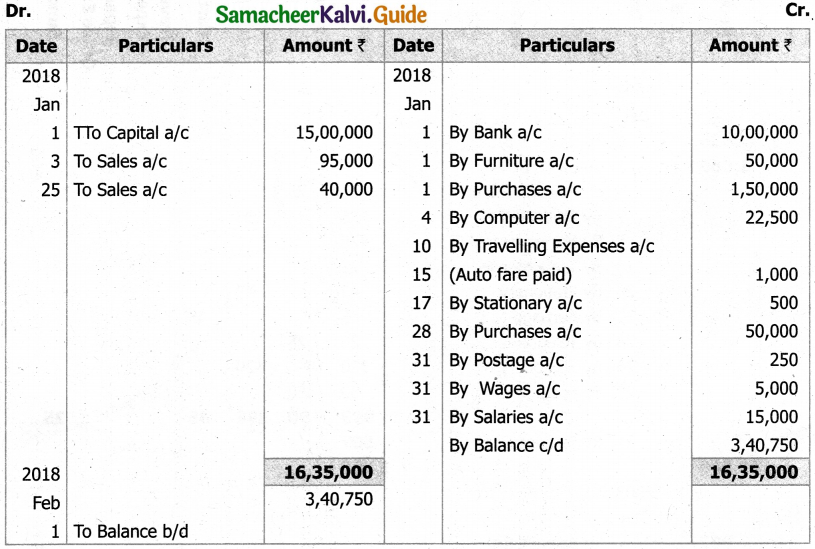

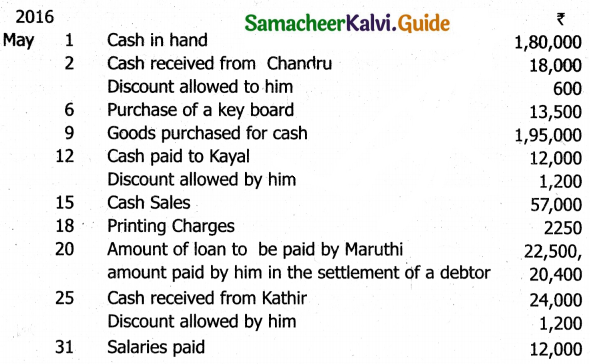

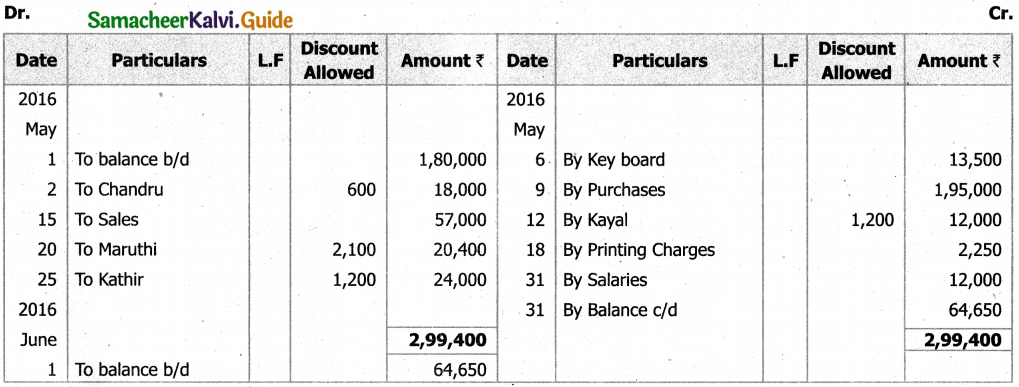

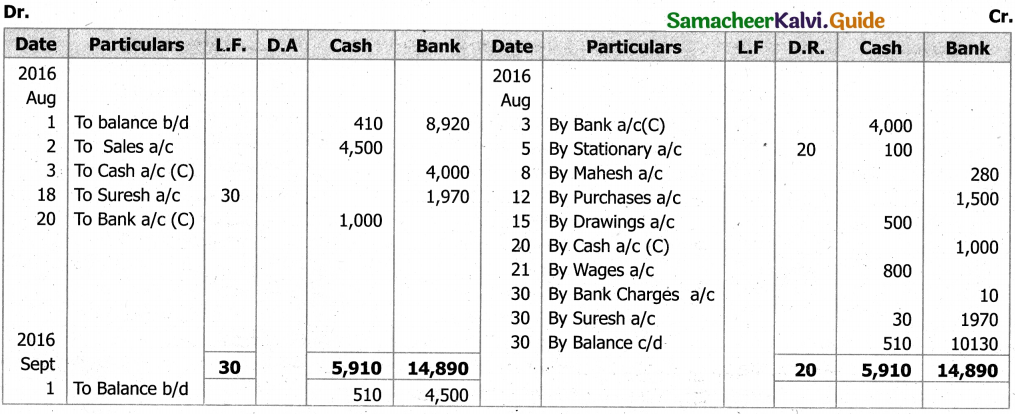

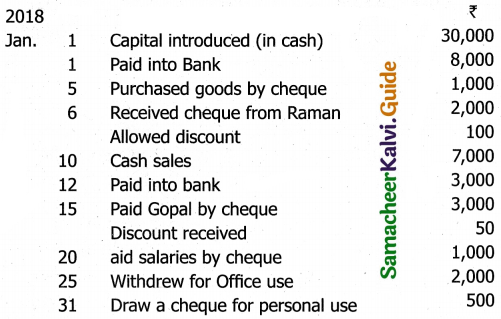

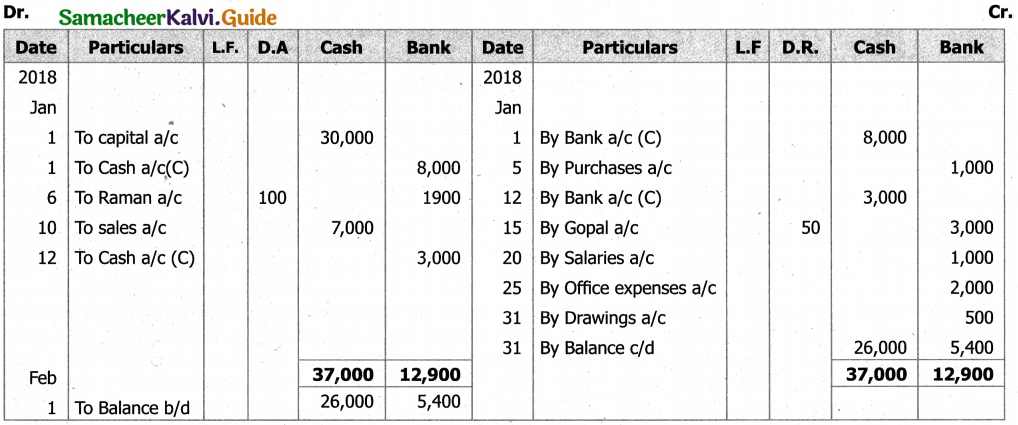

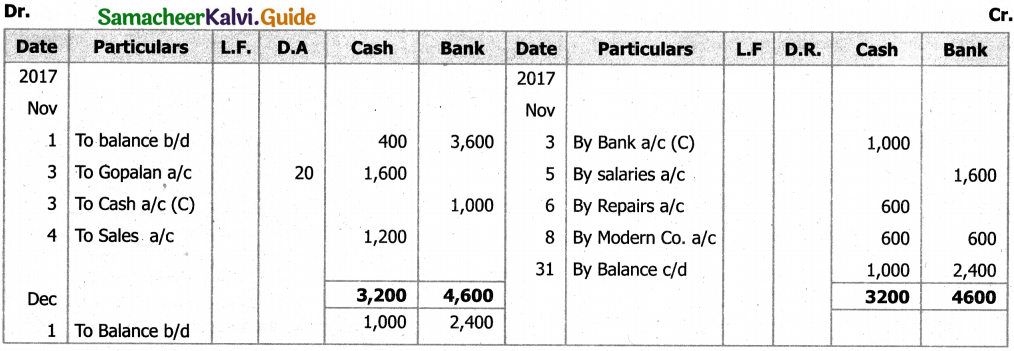

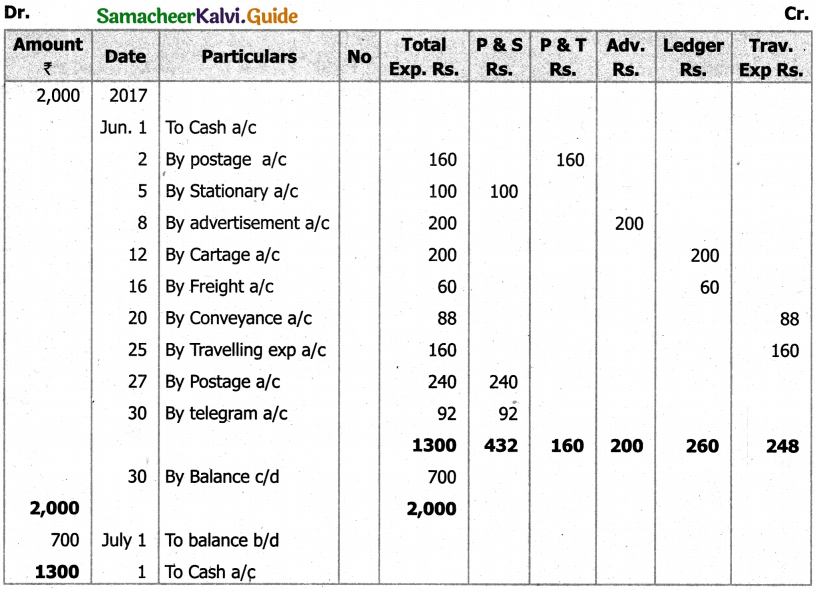

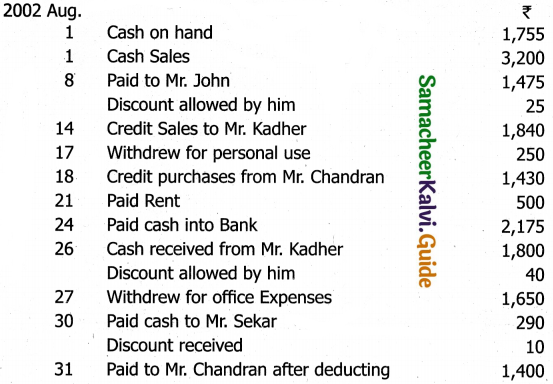

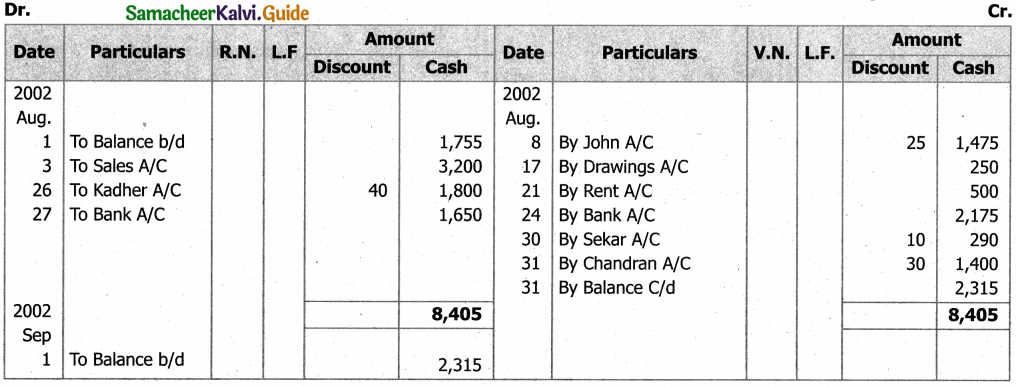

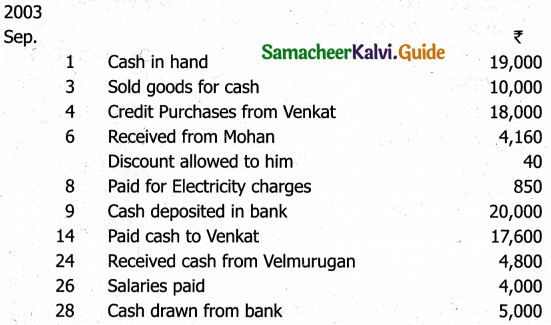

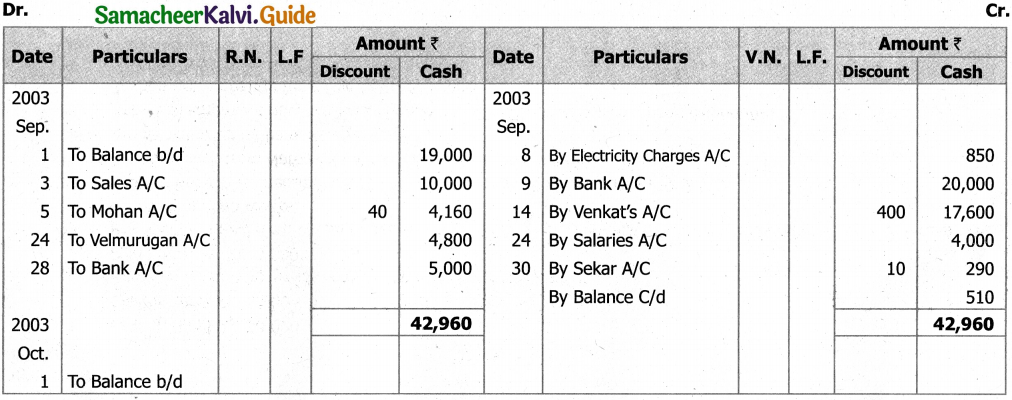

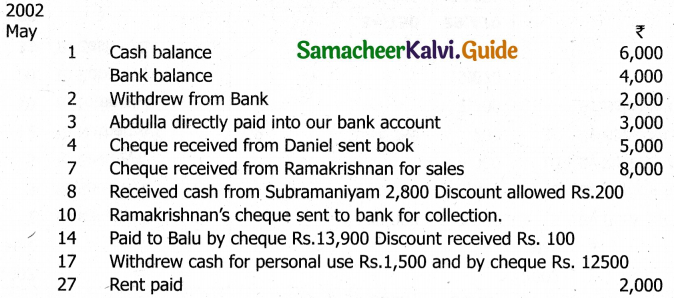

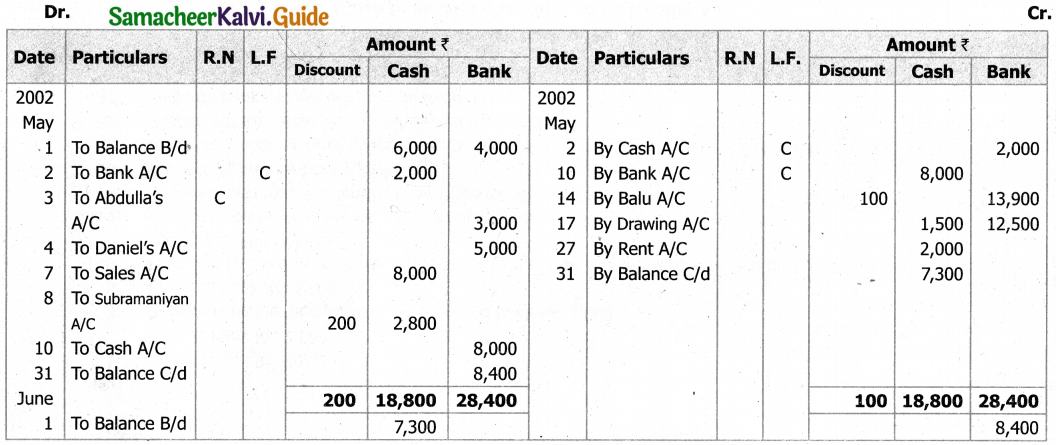

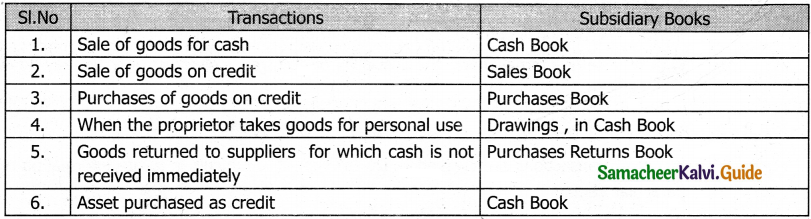

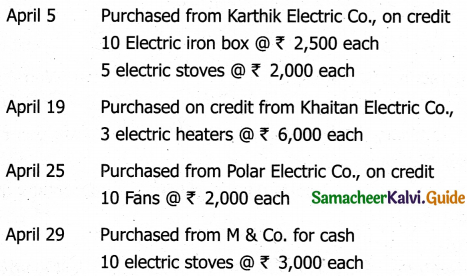

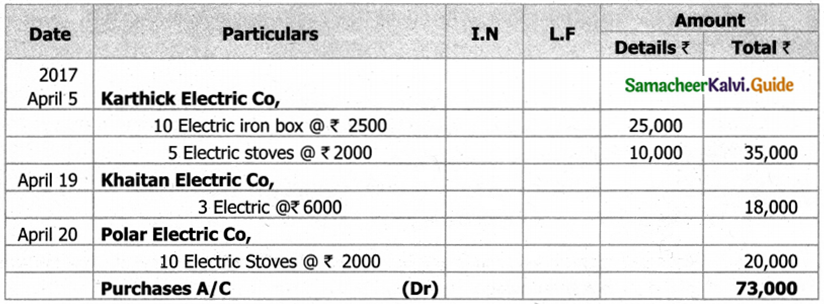

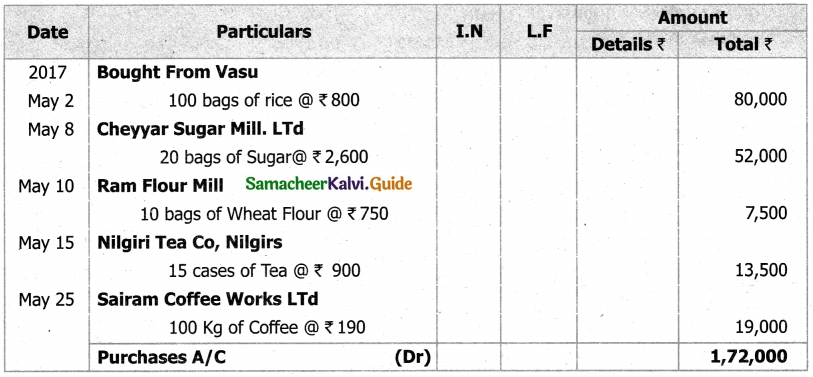

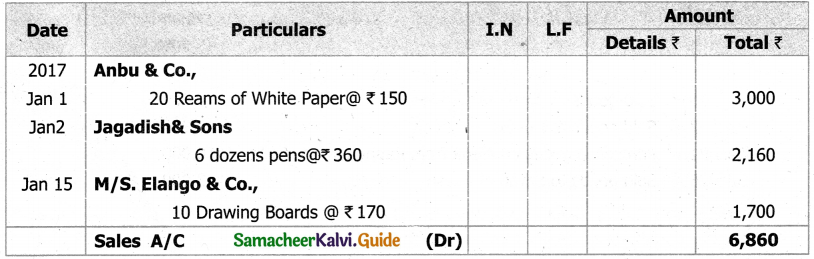

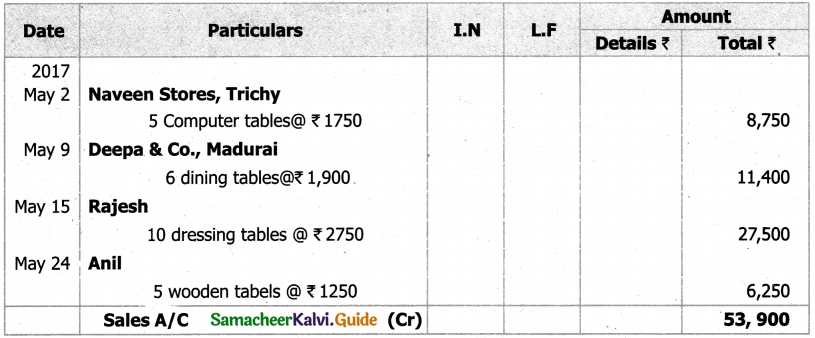

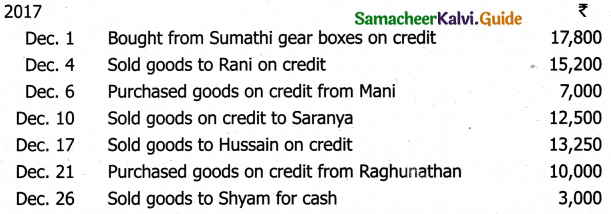

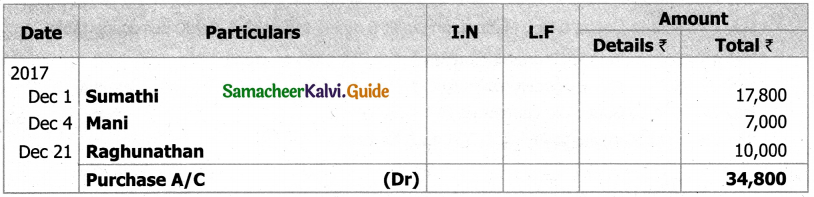

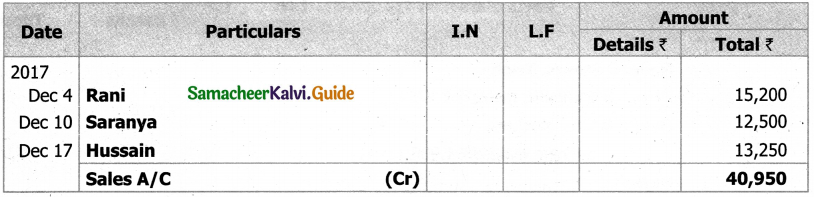

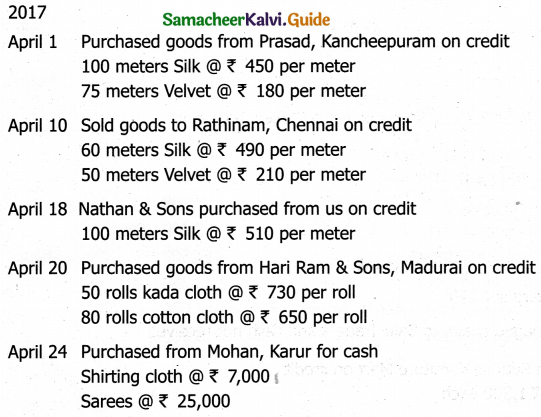

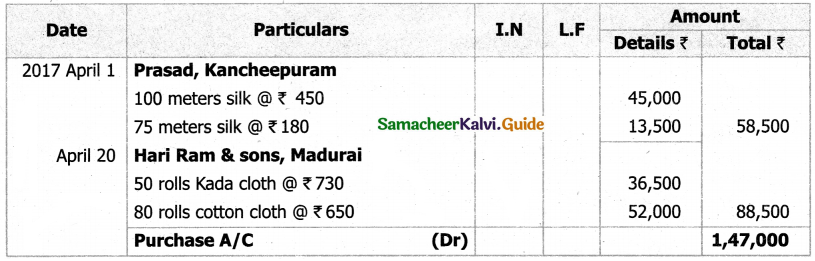

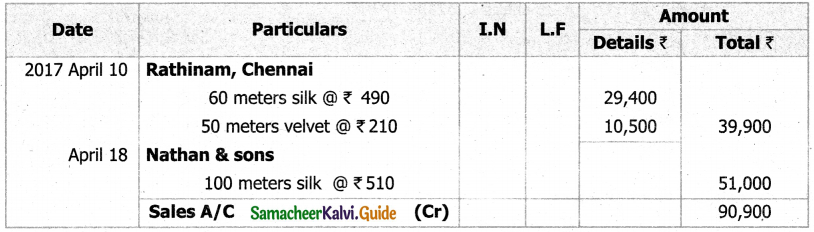

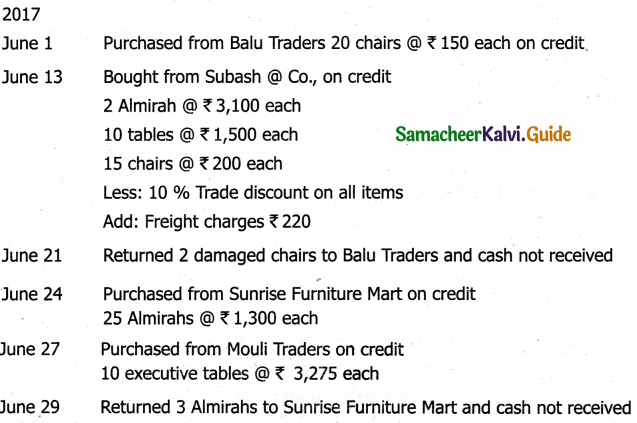

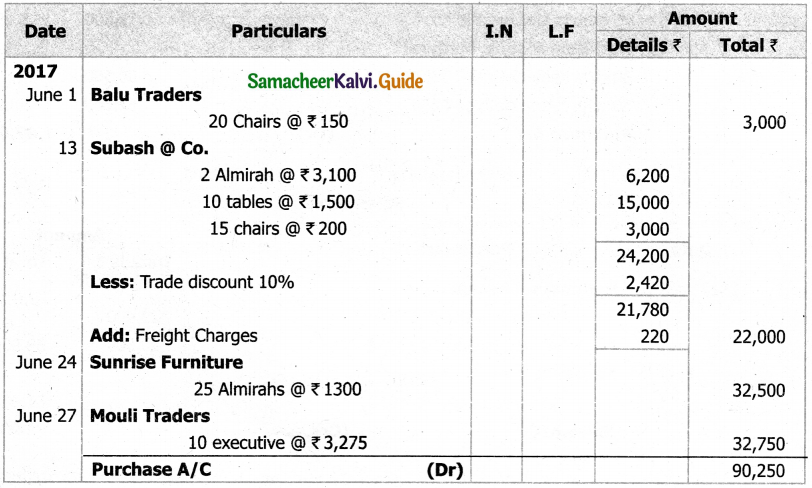

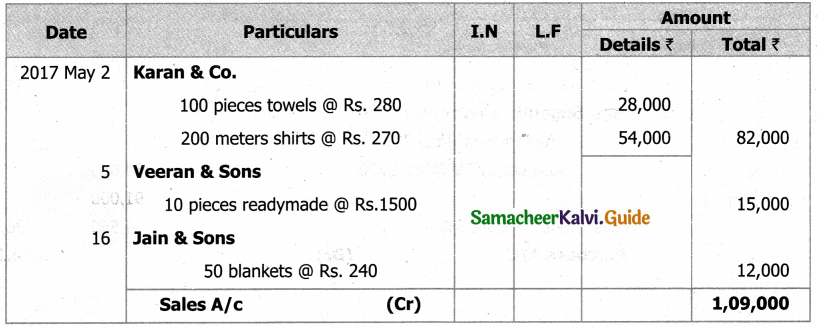

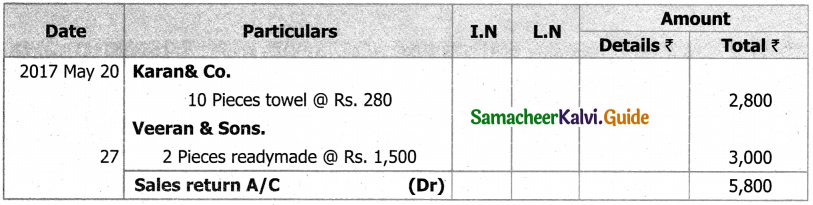

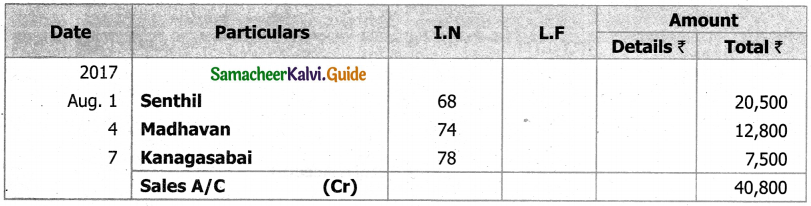

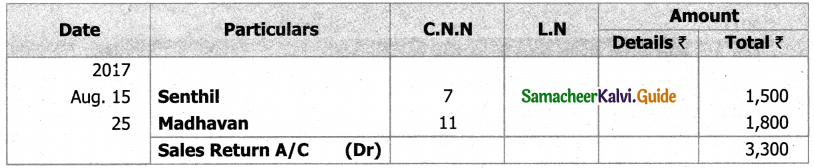

Kanagasabai Account

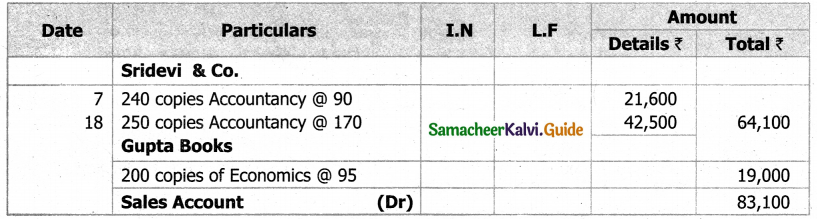

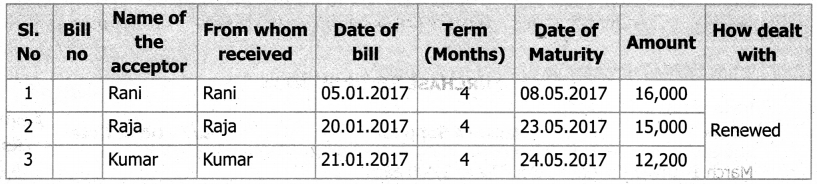

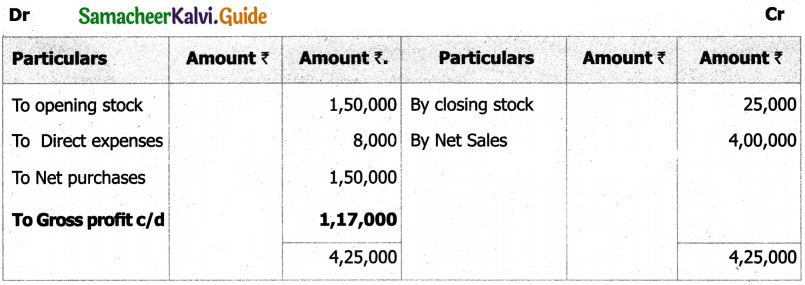

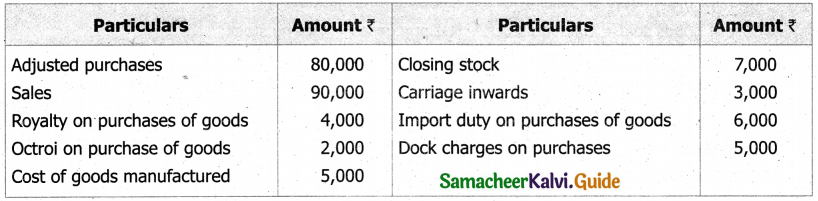

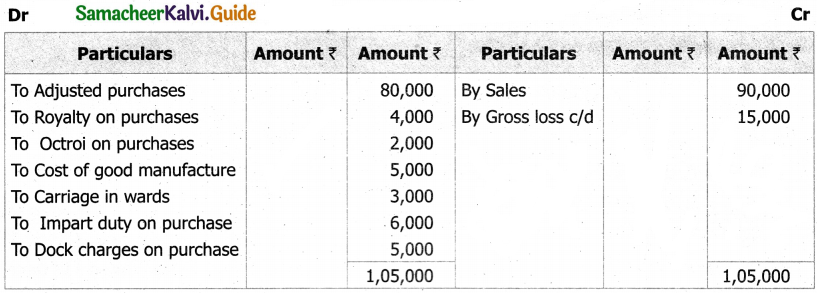

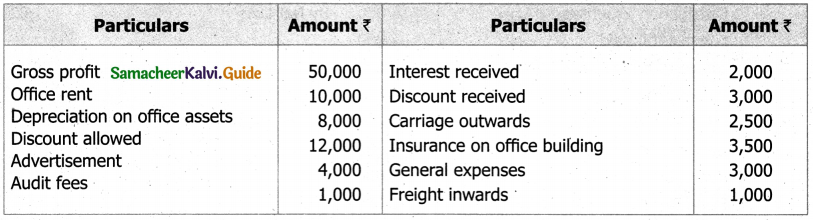

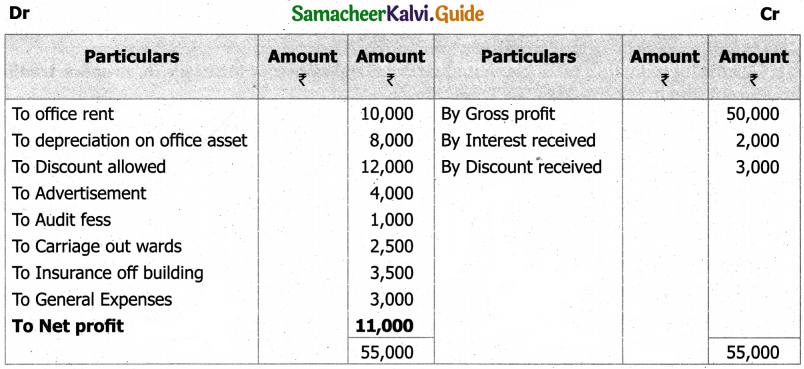

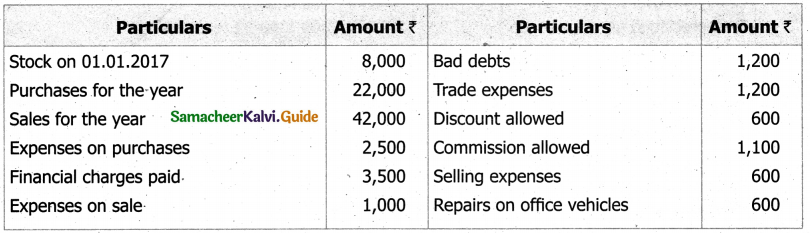

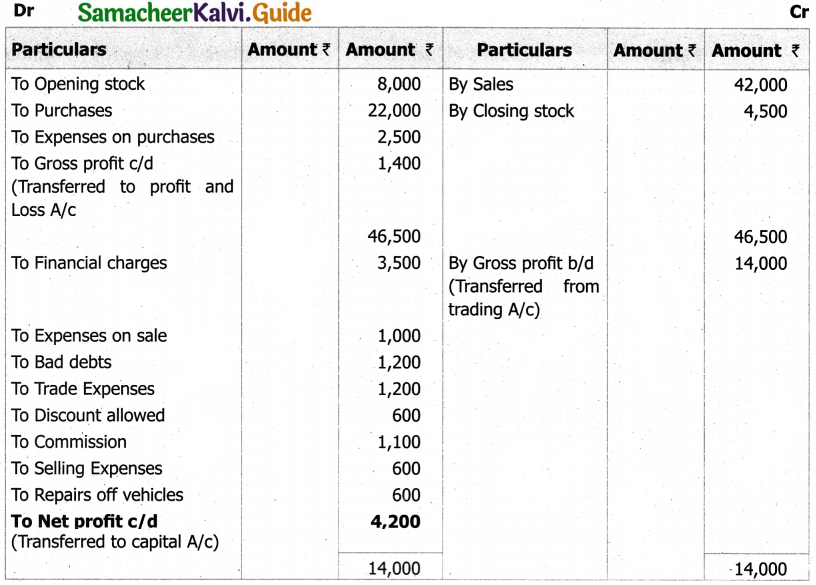

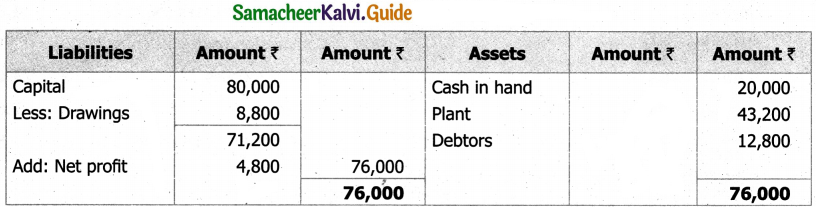

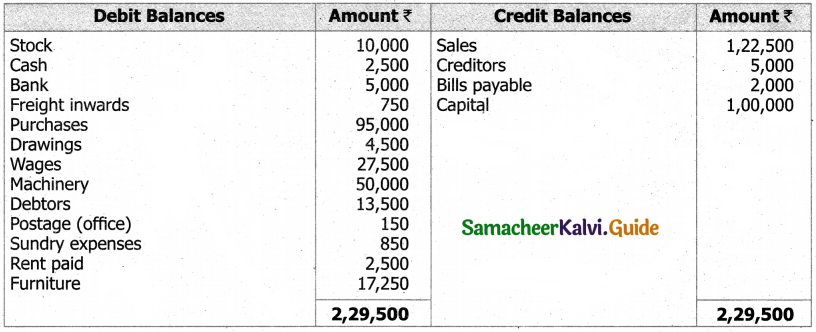

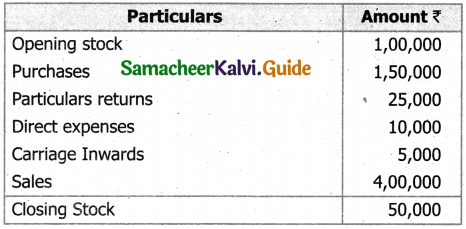

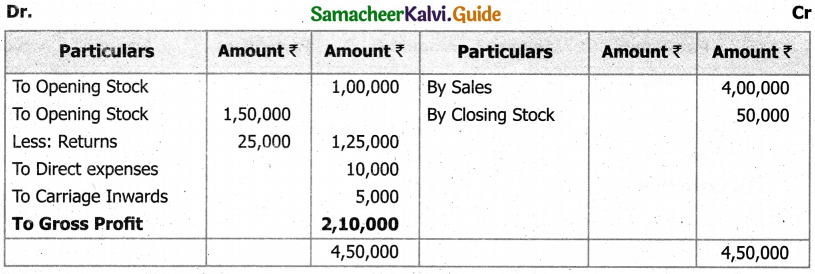

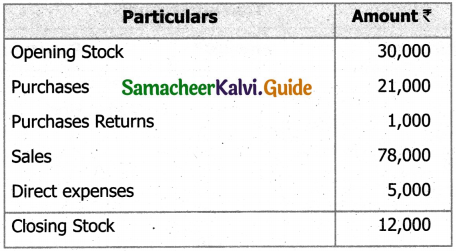

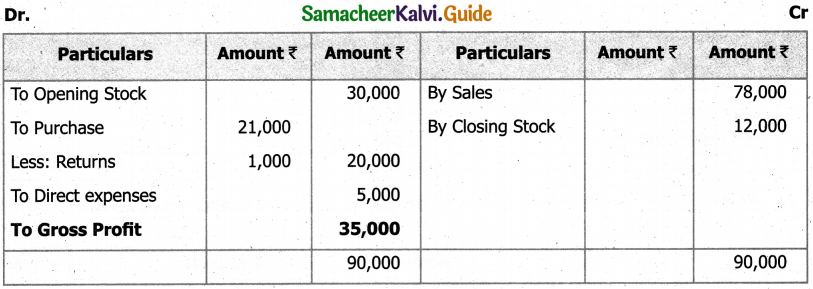

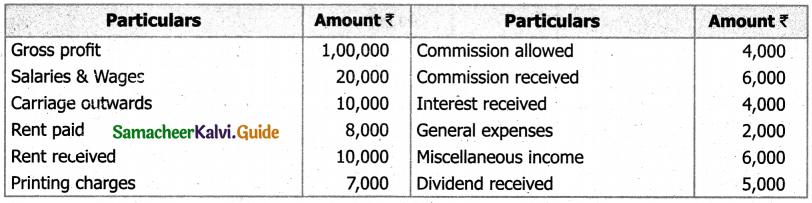

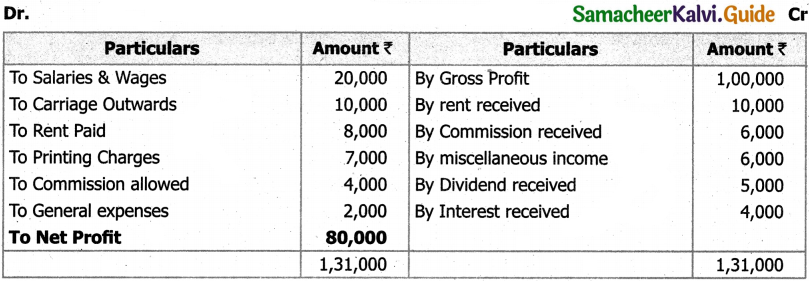

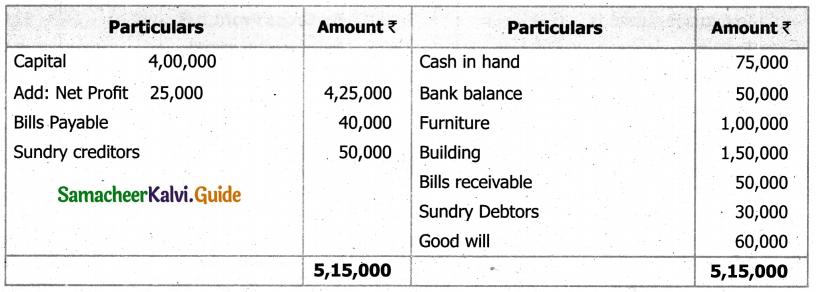

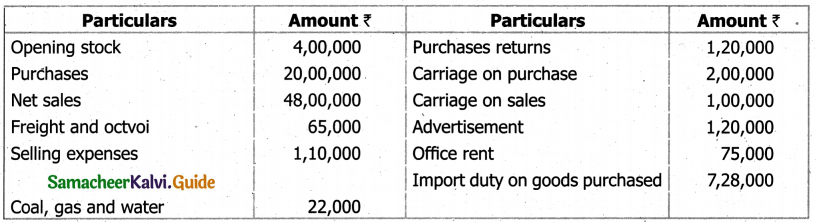

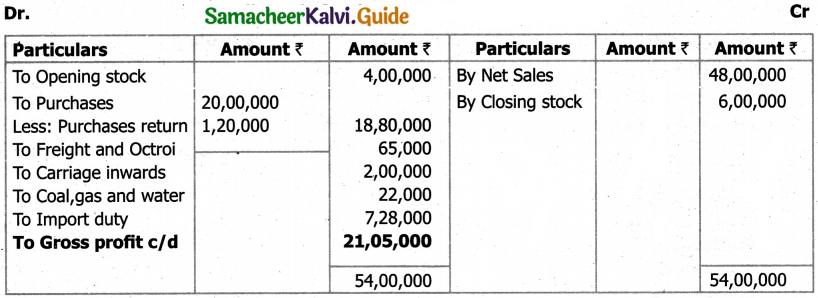

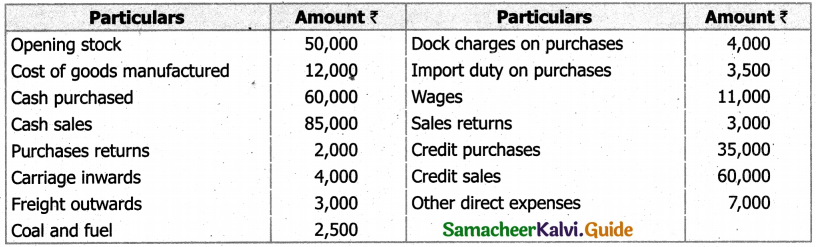

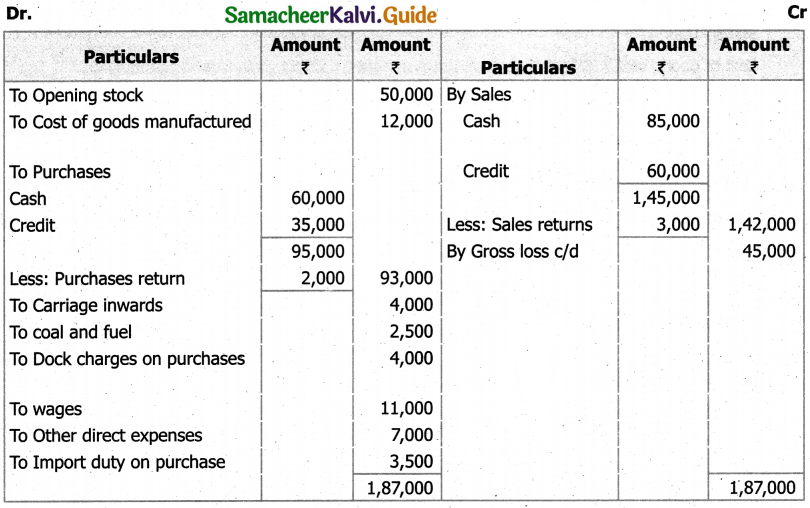

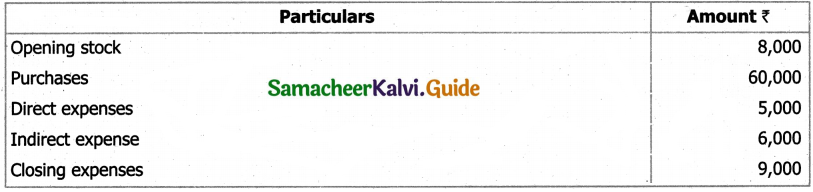

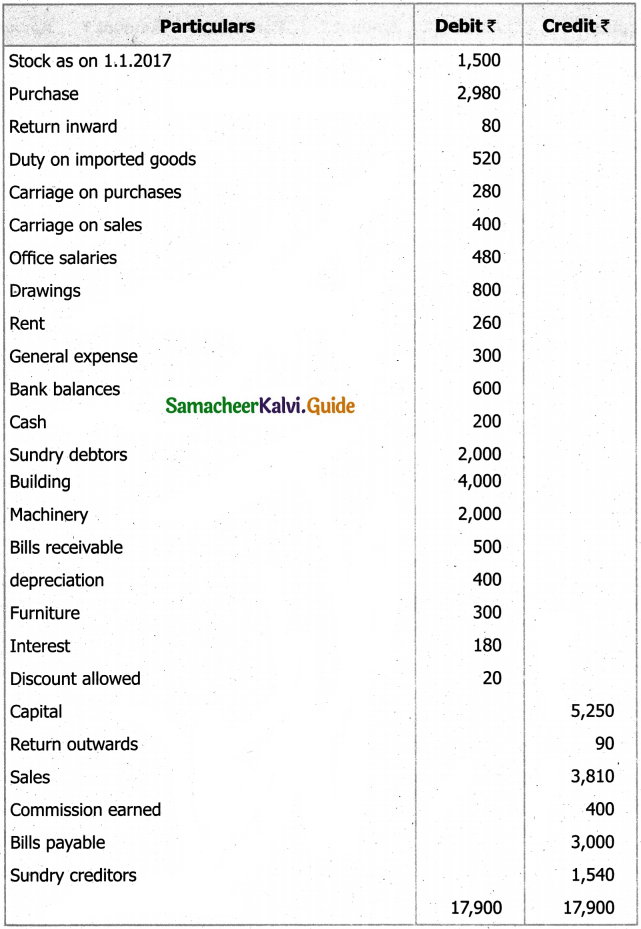

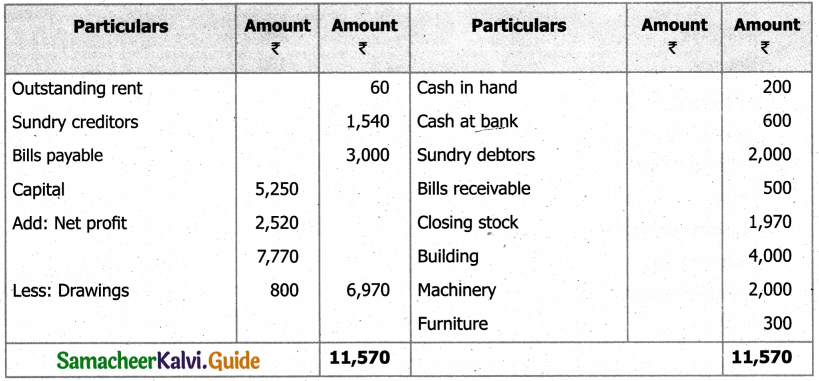

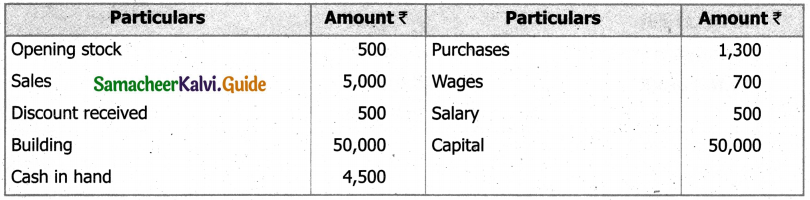

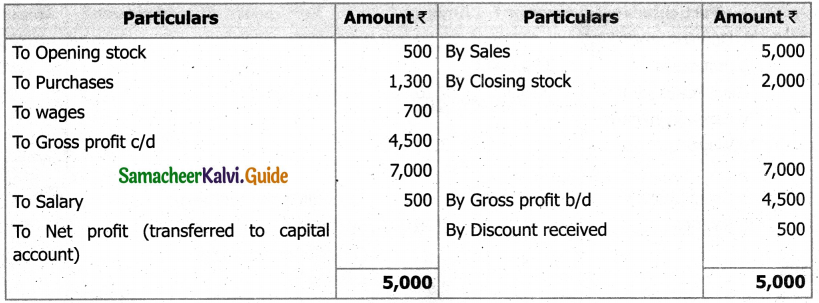

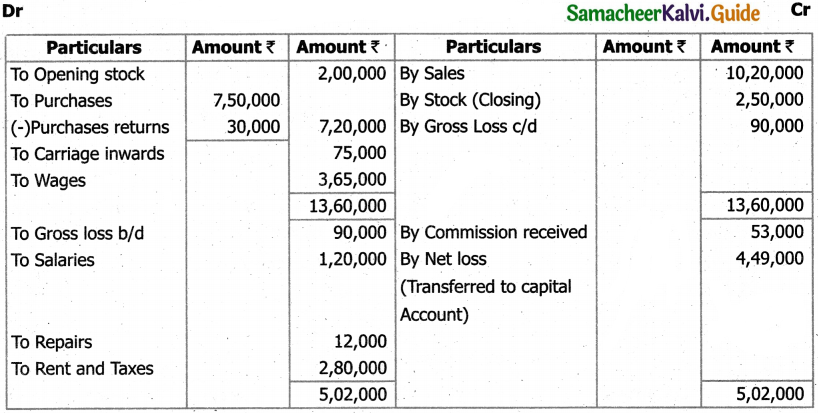

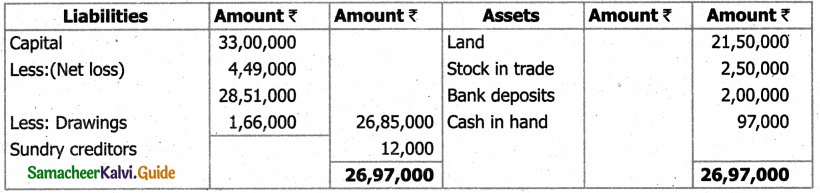

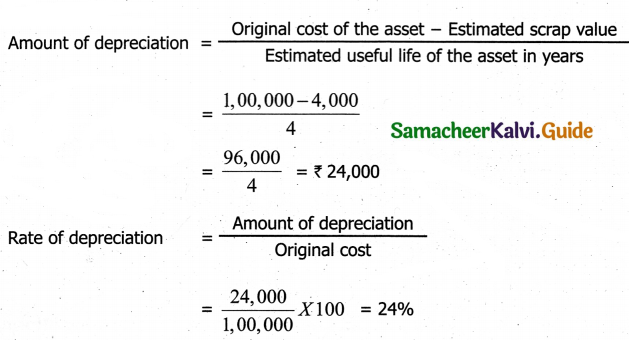

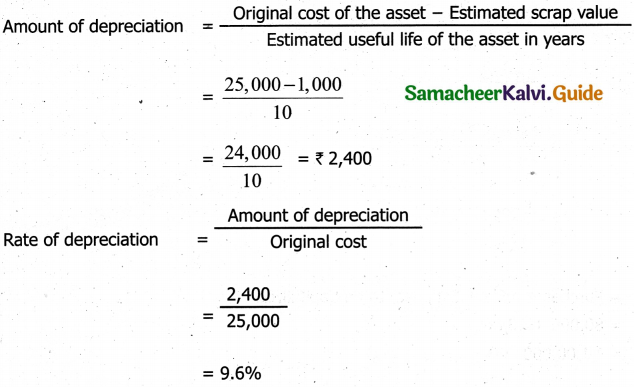

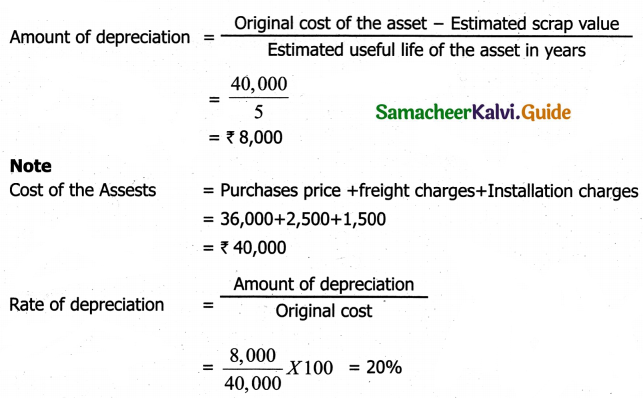

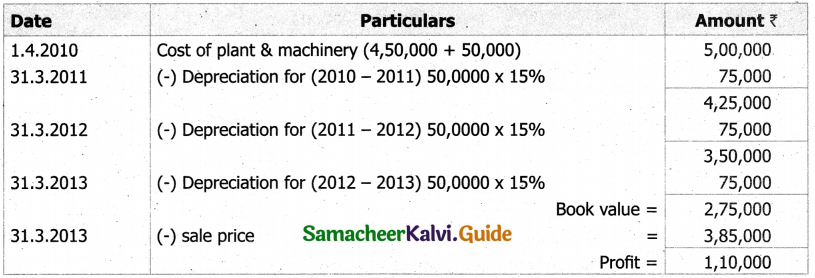

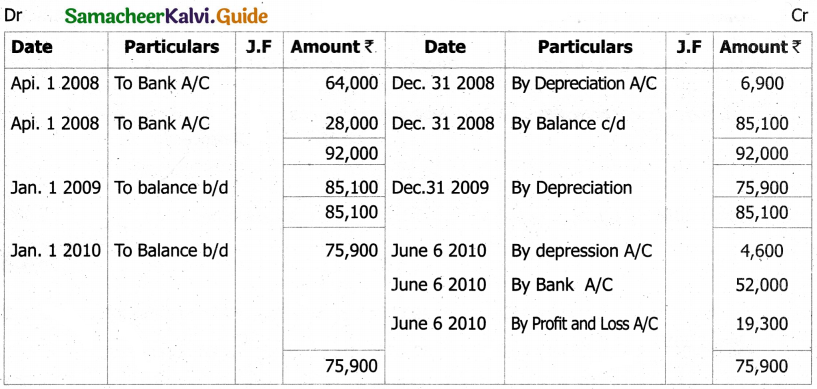

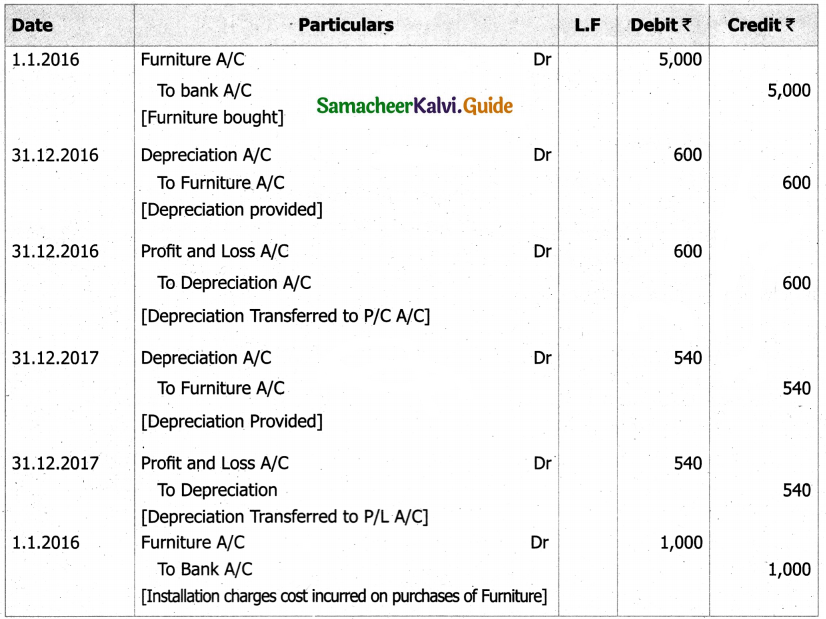

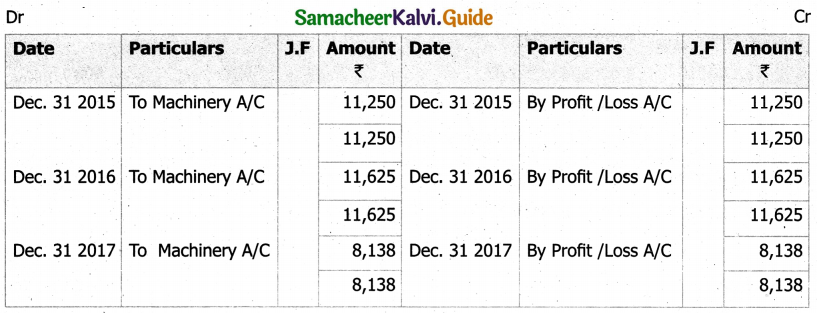

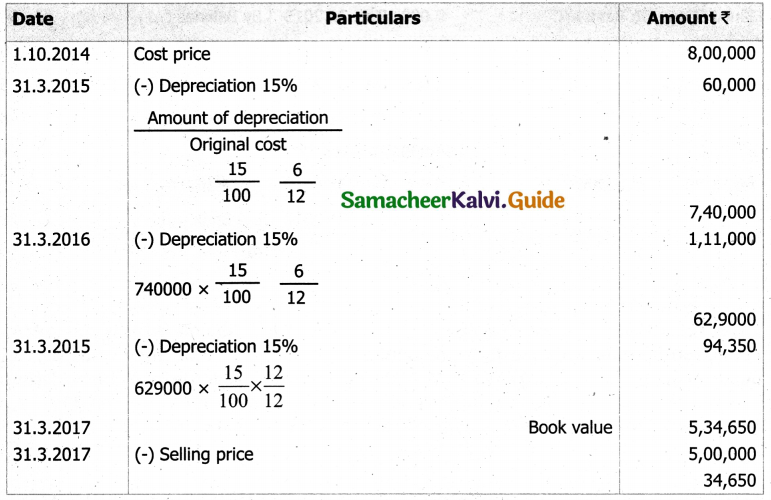

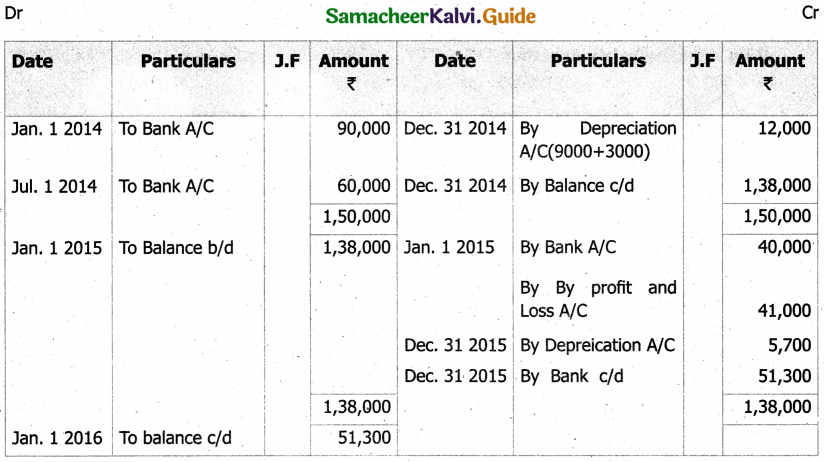

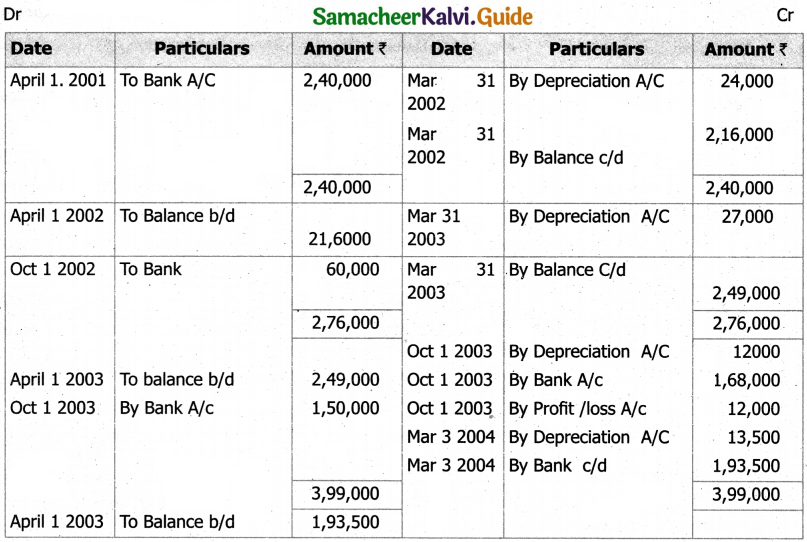

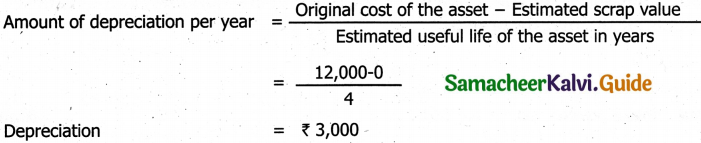

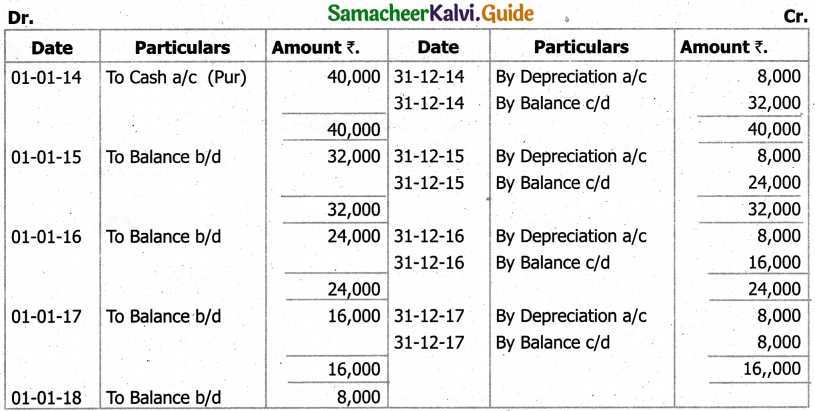

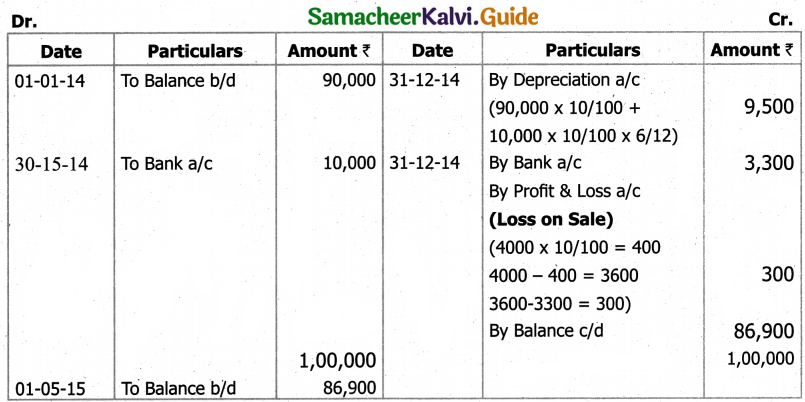

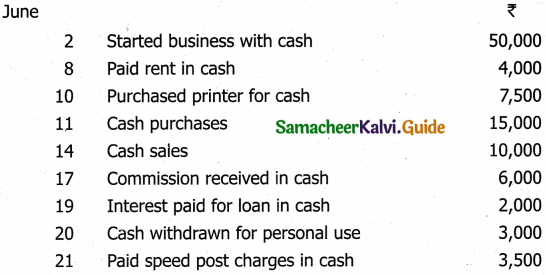

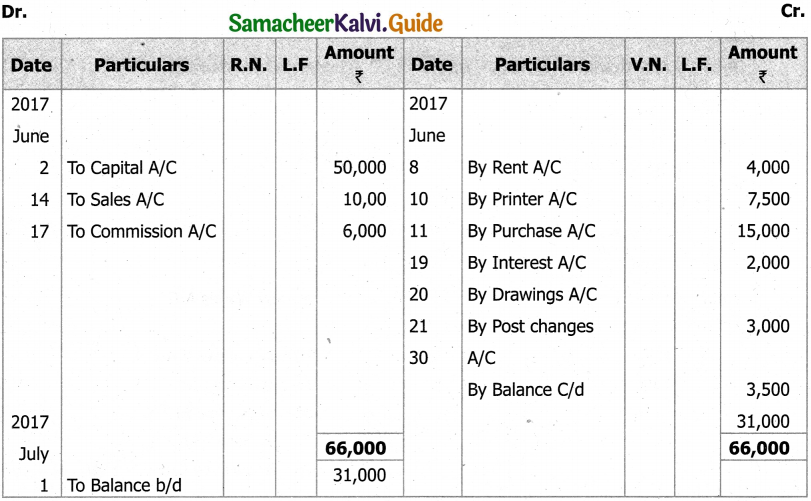

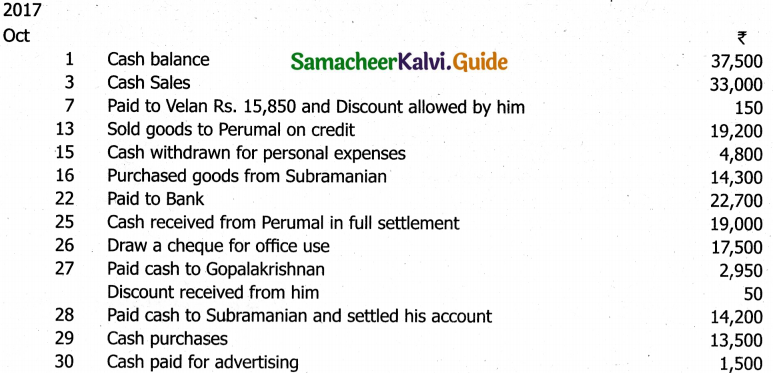

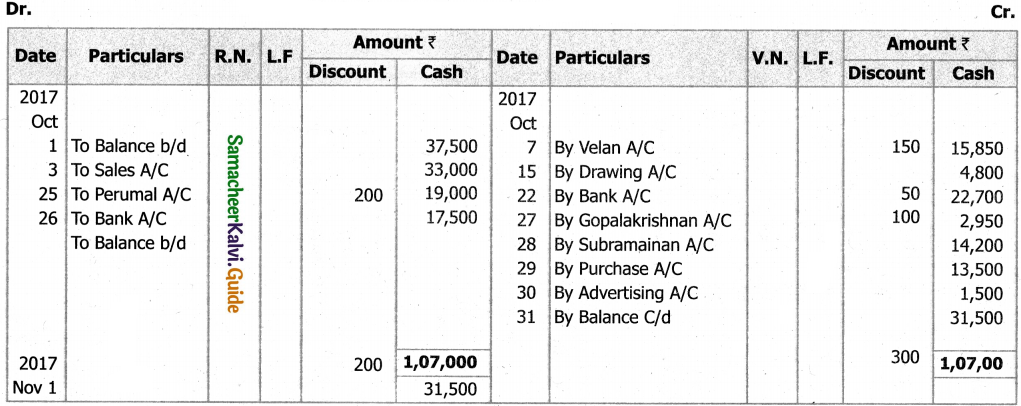

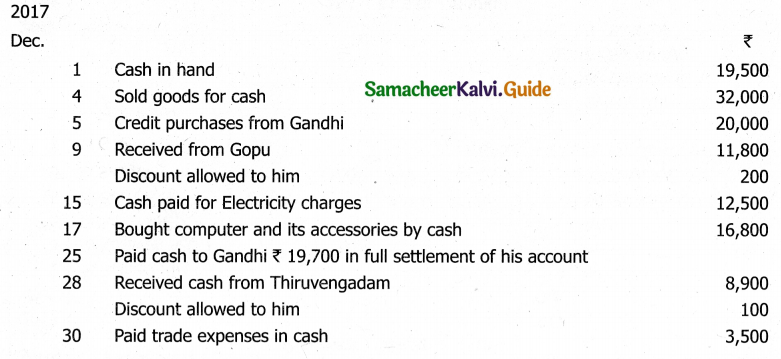

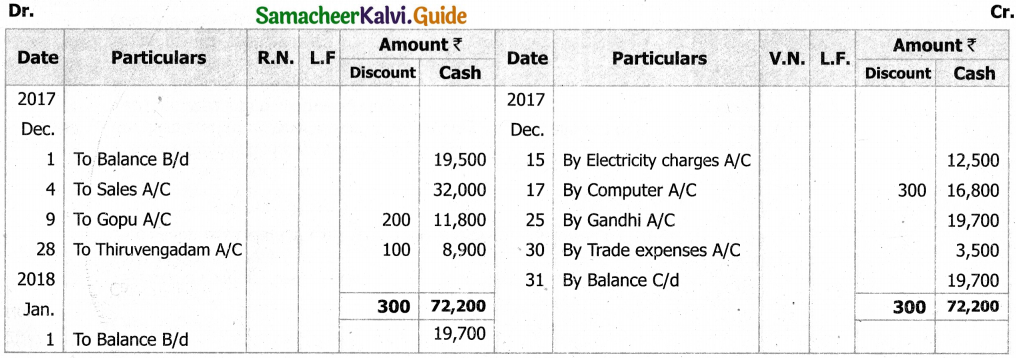

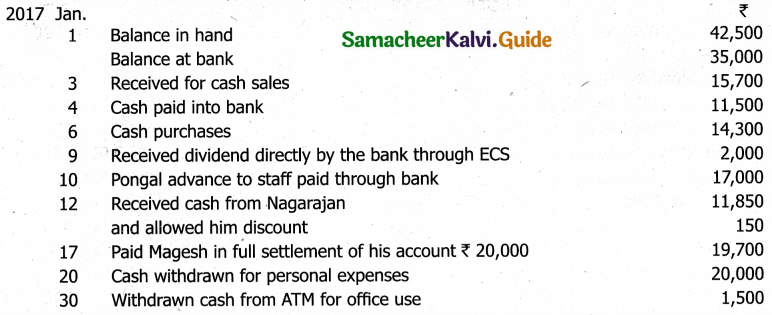

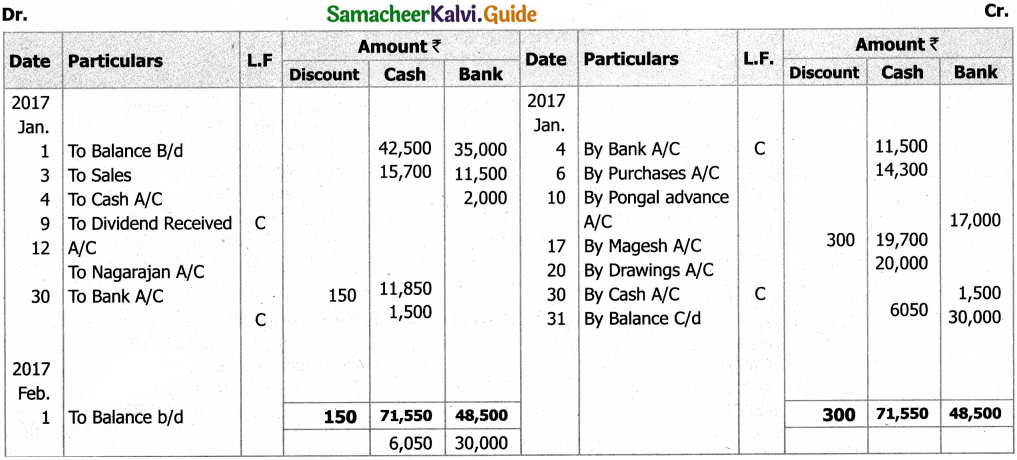

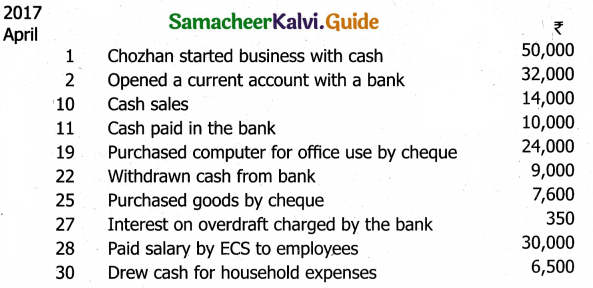

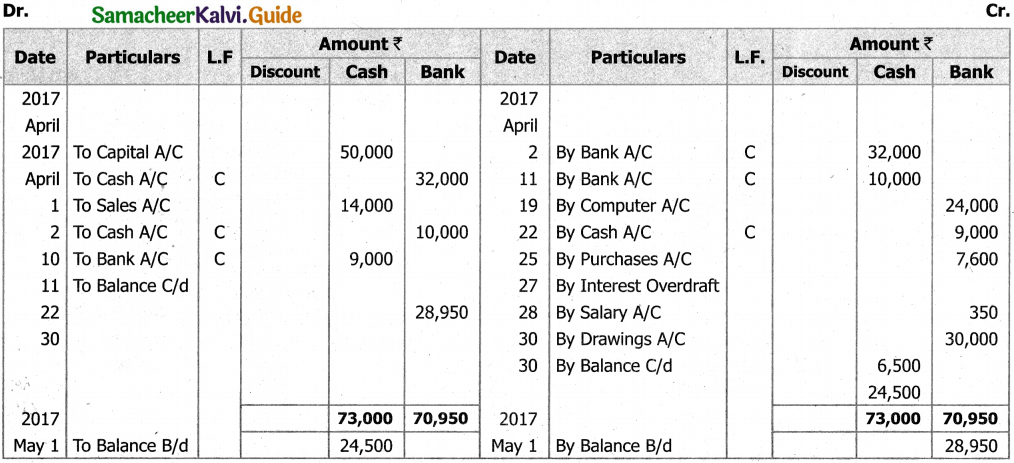

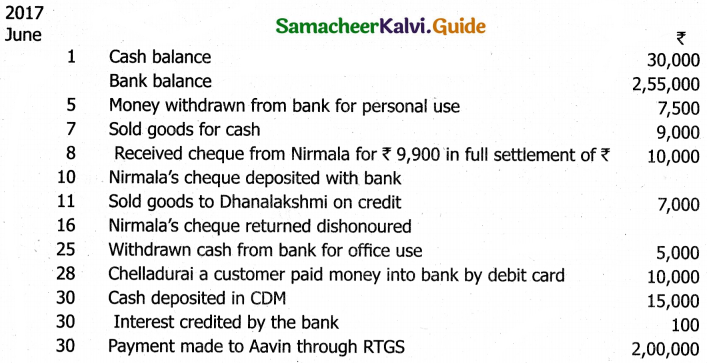

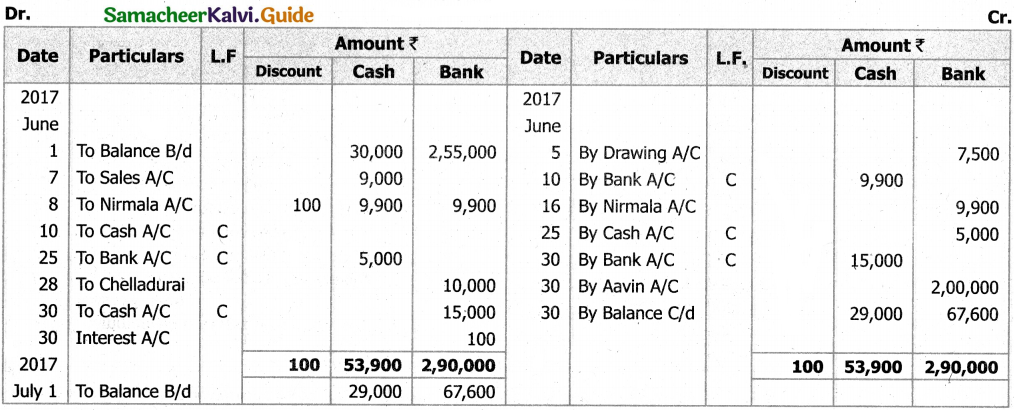

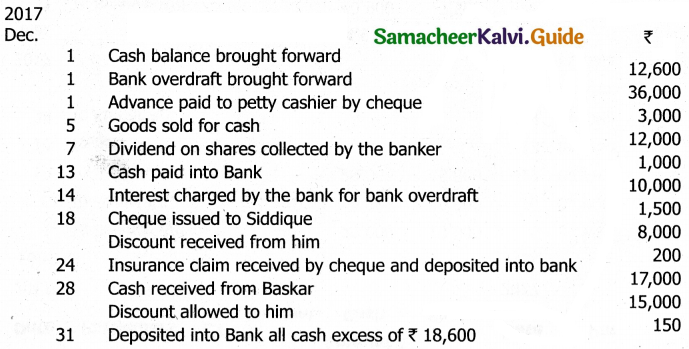

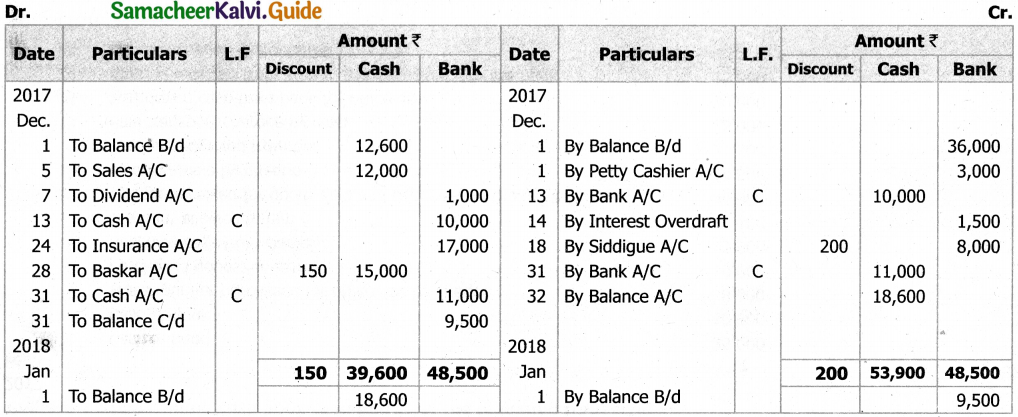

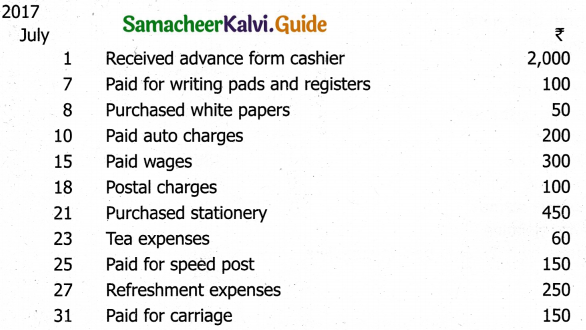

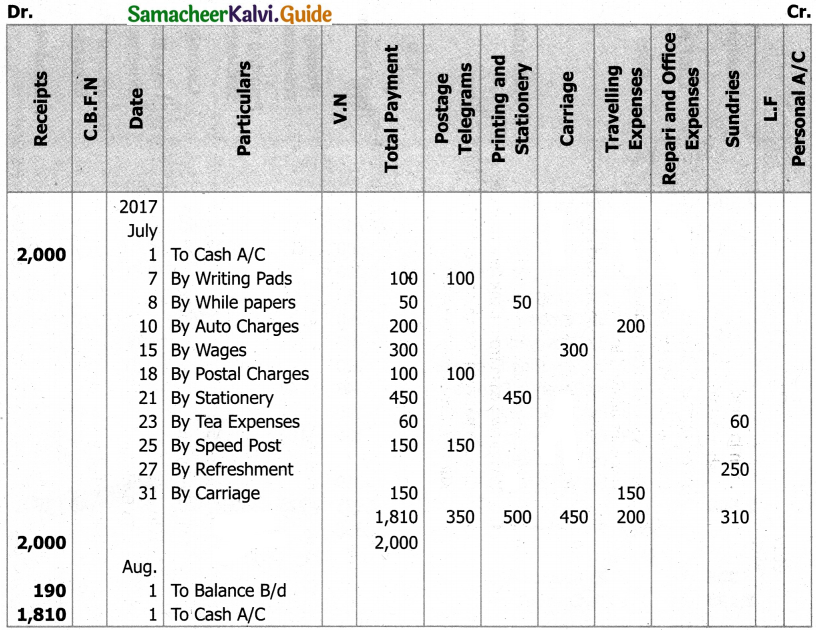

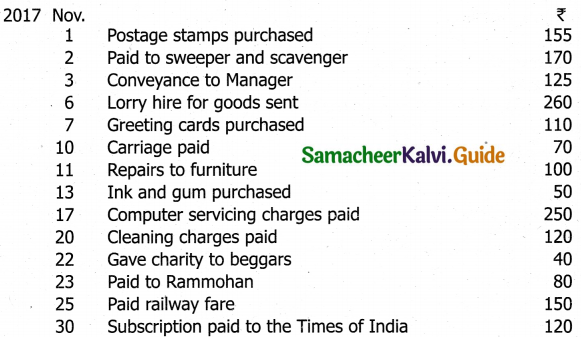

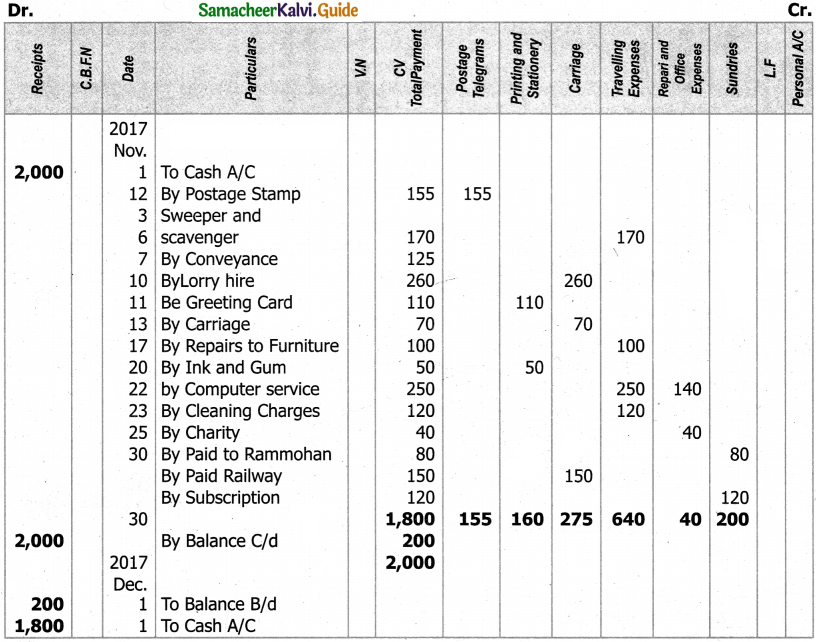

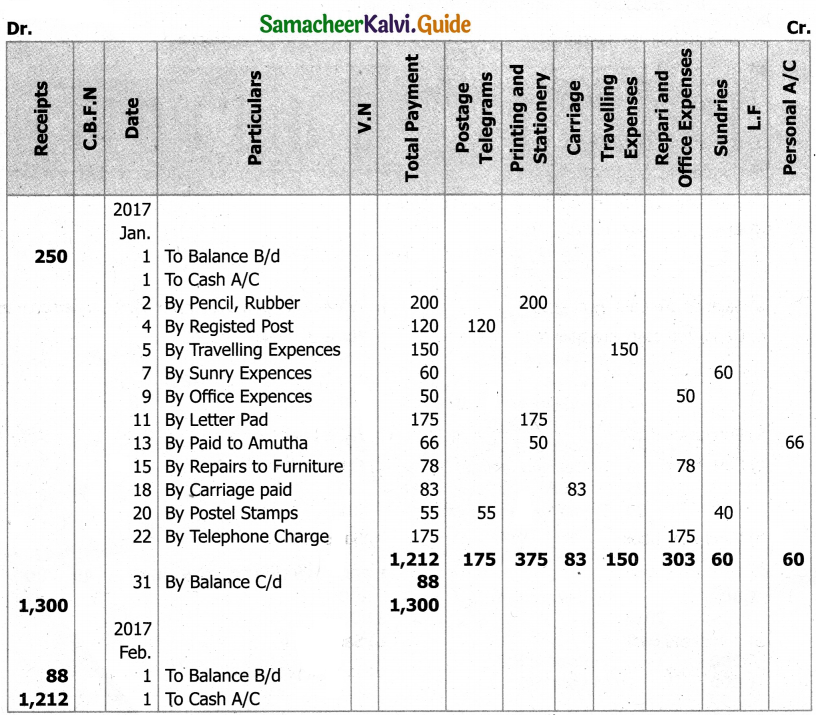

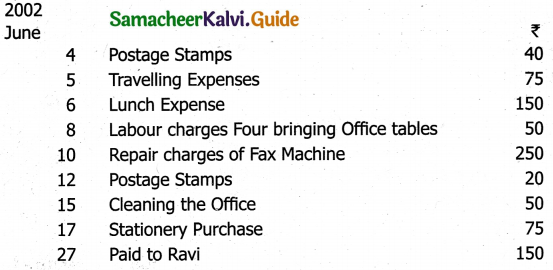

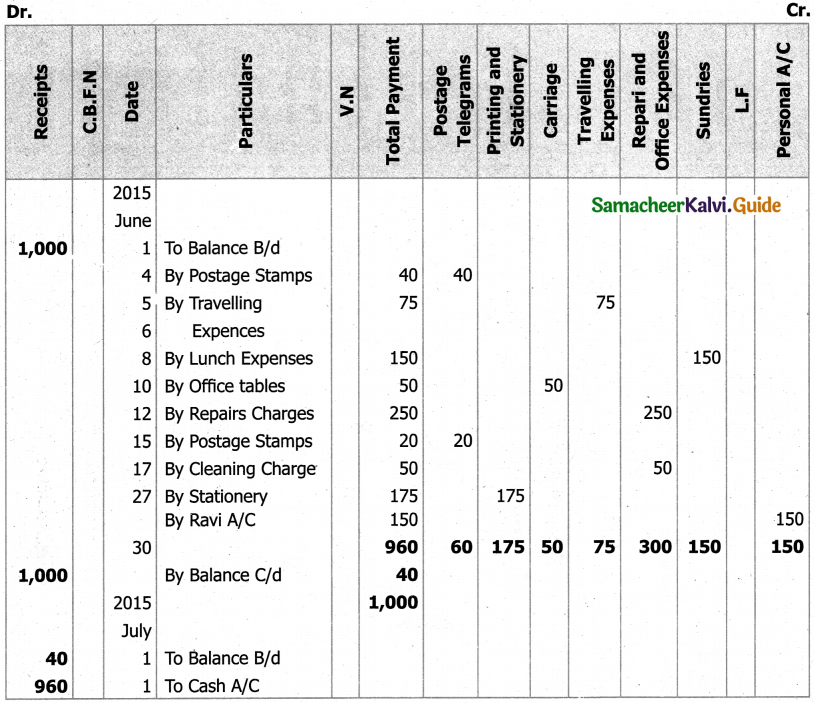

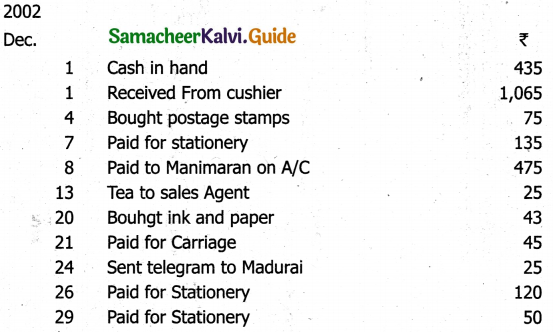

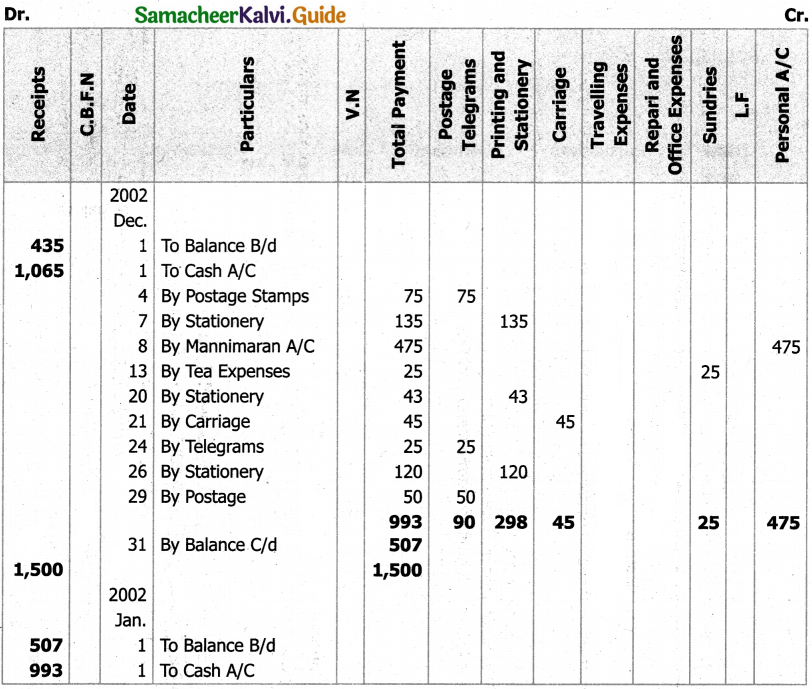

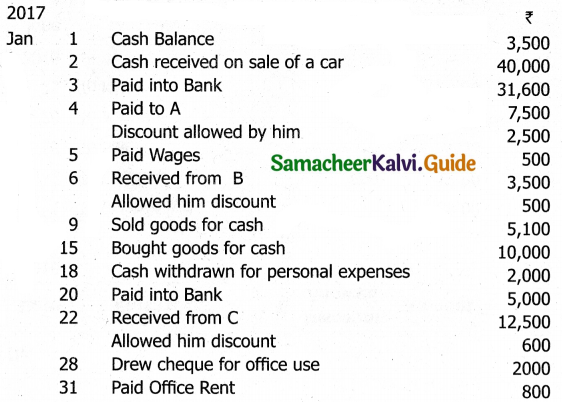

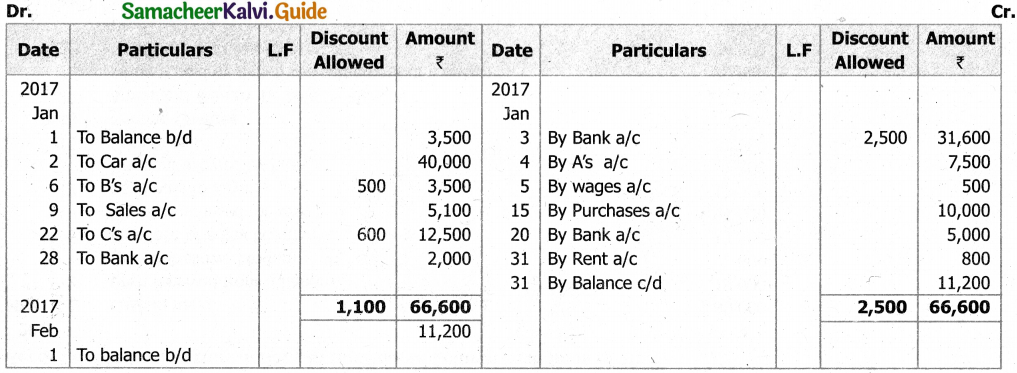

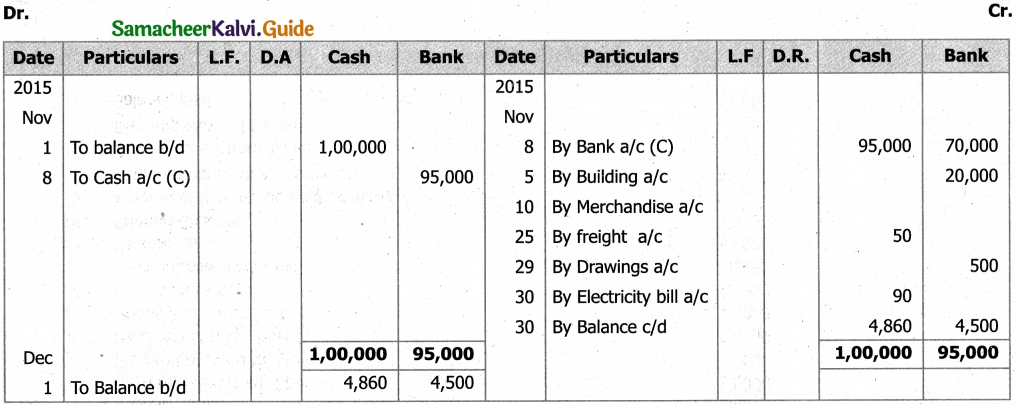

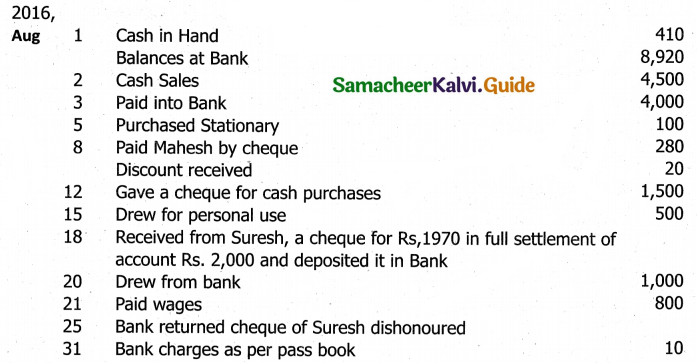

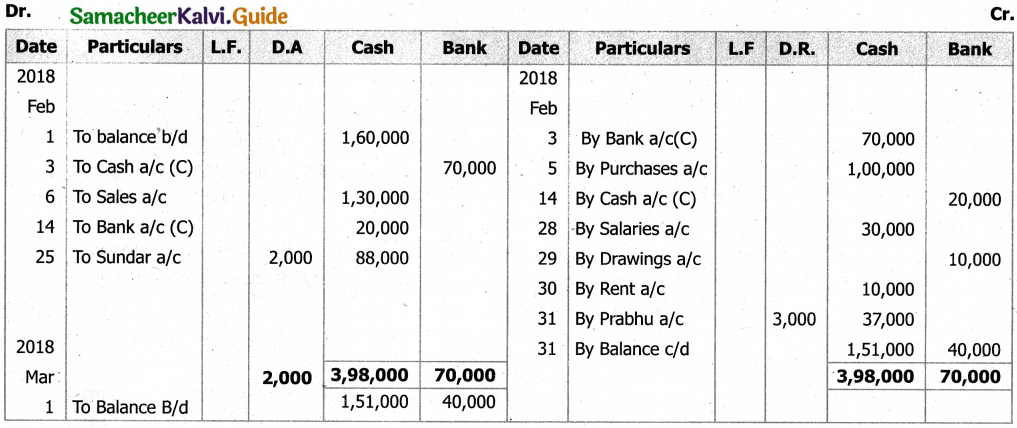

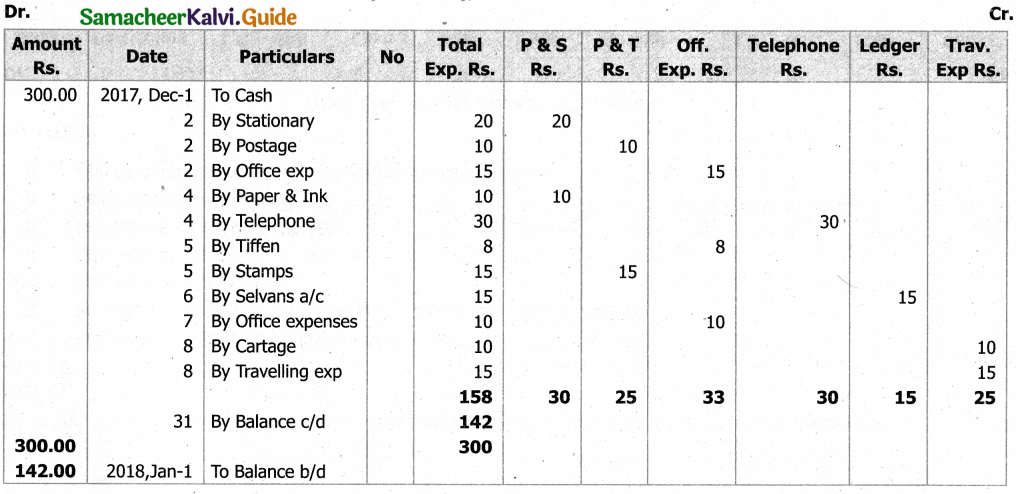

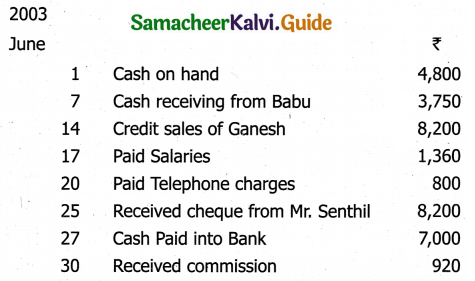

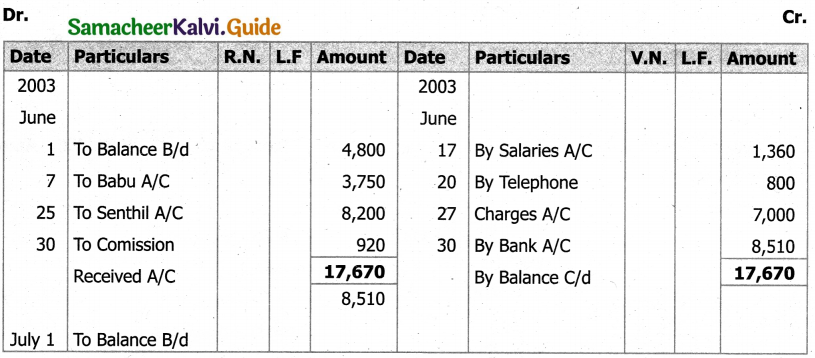

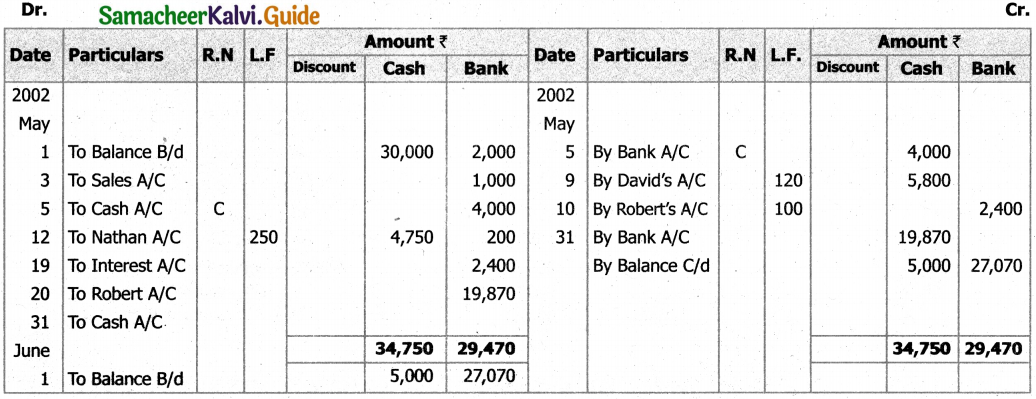

Kanagasabai Account