Tamilnadu State Board New Syllabus Samacheer Kalvi 11th Accountancy Guide Pdf Chapter 7 Subsidiary Books – II Text Book Back Questions and Answers, Notes.

Tamilnadu Samacheer Kalvi 11th Accountancy Solutions Chapter 7 Subsidiary Books – II

11th Accountancy Guide Subsidiary Books – II Text Book Back Questions and Answers

![]()

I. Multiple Choice Questions

Choose the correct answer.

Question 1.

Cash book is a ________.

a) Subsidiary book

b) Principal book

c) Journal proper

d) Both subsidiary book and principal book

Answer:

d) Both subsidiary book and principal book

Question 2.

The cash book records ________.

a) All cash receipts

b) All cash payments

c) Both (a) and (b)

d) All credit transactions

Answer:

c) Both (a) and (b)

Question 4.

A cash book with discount, cash and bank column is called ________.

a) Simple cash book

b) Double column cash book

c) Three column cash book

d) Petty cash book

Answer:

c) Three column cash book

Question 5.

In Triple column cash book, the balance of bank overdraft brought forward will appear in ________.

a) Cash column debit side

b) Cash column credit side

c) Bank column debit side

d) Bank column credit side

Answer:

d) Bank column credit side

Question 6.

Which of the following is recorded as contra entry?

a) Withdrew cash from bank for personal use

b) Withdrew cash from bank for office use

c) Direct payment by the customer in the bank account of the business

d) When bank charges interest

Answer:

b) Withdrew cash from bank for office use

![]()

Question 7.

If the debit and credit aspects of a transaction are recorded in the cash book, it is ________.

a) Contra entry

b) Compound entry

c) Single entry

d) Simple entry

Answer:

a) Contra entry

Question 8.

The balance in the petty cash book is ________.

a) An expense

b) A profit

c) An asset

d) A liability

Answer:

c) An asset

Question 9.

Petty cash may be used to pay ________.

a) The expenses relating to postage and conveyance

b) Salary to the Manager

c) Purchase of furniture and fixtures

d) Purchase of raw materials

Answer:

a) The expenses relating to postage and conveyance

Question 10.

Small payments are recorded in a book called ________.

a) Cash Book

b) Purchase Book

c) Bills Payable Book

d) Petty Cash Book

Answer:

d) Petty Cash Book

![]()

II. Very Short Answer Type Questions

Question 1.

What is cash book?

Answer:

The book in which only cash transactions are recorded in the chronological order is known as cash book. Cash receipts are recorded on the debit side and Cash payments are recorded on the credit side. It is like a subsidiary book and a principal book.

Question 2.

What are the different types of cash book?

Answer:

The main cash book may be of various types and following are the three most common types.

- Simple or single column cash book (only cash column)

- Cash book with cash and discount column (double column cash book)

- Cash book with cash, discount and bank columns (three column cash book).

- Apart from the main cash book, petty cash book may also be prepared to enter the petty expenses, i.e., expenses involving small amount.

Question 3.

What is simple cash book?

Answer:

- Single column cash book or simple cash book, like a ledger account has only one amount column, i.e., cash column on each side.

- Only cash transactions are recorded in this book.

- All cash receipts and payments are recorded systematically in this book.

Question 4.

Give the format of ‘Single column cash book’.

Answer:

Simple Cash Book

Question 5.

What is double column cash book?

Answer:

- It is a cash book with cash and discount columns.

- As there are two columns, i.e., discount and cash columns, both on debit and credit sides, this cash book is known as ‘double column cash book’.

- Discount column represents discount allowed on the debit side and discount received on the credit side.

Question 6.

Give the format of ‘Double column cash book’.

Answer:

Double Column Cash Book

Question 7.

What is three column cash book?

Answer:

- A three column cash book includes three amount columns on both sides, i.e., cash, bank and discount.

- This cash book is prepared in the same way as simple and double column cash books are prepared.

- The transactions which increase the cash and bank balance are recorded on the debit side of the cash and bank columns respectively.

- Opening balance of cash and favorable bank balance appear as the first item on the debit side of the three column cash book in case of existing business.

![]()

Question 8.

What is cash discount?

Answer:

- Cash discount is allowed to the parties making prompt payment within the stipulated period of time or early payment.

- It is discount allowed (loss) for the creditor and discount received (gain) for the debtor who makes payment.

- The discount is allowed when payment is received or made and hence, the entry for discount is also passed with the entry of payment.

- Cash discount motivates the debtor to make the payment at an earlier date to avail discount facility.

Question 9.

What is trade discount?

Answer:

- Trade discount is a deduction given by the supplier to the buyer on the list price or catalogue price of the goods.

- It is given as a trade practice or when goods are purchased in large quantities.

- It is shown as a deduction in the invoice.

- Trade discount is not recorded in the books of accounts.

- Only the net amount is recorded.

Example:

Suppose the sale of goods for ₹ 10,000 was made and 10% was allowed as trade discount, the entry regarding sales will be made for ₹ 9,000 (10,000 – 10 per cent of 10,000). In the same way, purchaser of goods will also record purchases as 19,000).

Question 10.

What is a petty cash book?

Answer:

- Business entities have to pay various small expenses like taxi fare, bus fare, postage, carriage, stationery, refreshment and other sundry items.

- These are small payments and repetitive in nature.

- If all these small payments are recorded in the main cash book, it will be loaded with lot of entries.

- Hence, all petty payments of the business may be recorded in a separate book, which is called as petty cash book and the person who maintains the petty cash book is called the petty cashier.

![]()

III. Short Answer Questions

Question 1.

Explain the meaning of imprest system of petty cash book.

Answer:

- Under this system, a fixed amount necessary or sufficient to meet petty payments determined on the basis of past experience is paid to the petty cashier on the first day of the period. (It may be a week or fortnight or month).

- The amount given to the petty cashier in advance is known as “Imprest Money”.

- The word imprest means payment in advance.

- The petty cashier makes payments from this amount and records them in petty cash book.

- At the end of a particular period, the petty cashier submits the petty cash book to the head cashier.

- The head cashier scrutinies the petty payments and gives amount equal to the amount spent by petty cashier so that the total amount with the petty cashier is now equal to the amount he had received in the beginning as advance.

- Under the system, the total cash with the petty cashier never exceeds the imprest at any time during the period.

- This method thus provides an effective control over petty payments.

Question 2.

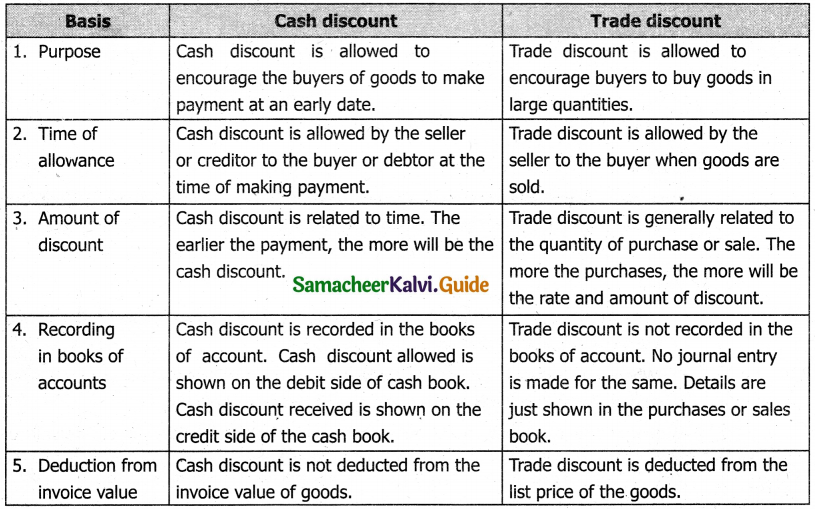

Bring out the differences between cash discount and trade discount.

Answer:

Following are the difference between cash discount and trade discount:

Question 3.

Write the advantages of maintaining petty cash book.

Answer:

Following are the advantages of maintaining petty cash book:

- There can be better control over petty payments.

- There is saving of time of the main cashier.

- Cash book is not loaded with many petty payments.

- Posting of entries from main cash book and petty cash book is comparatively easy.

Question 4.

Write a brief note on accounting treatment of discount in cash book.

Answer:

- Discount column represents discount allowed on the debit side and discount received on the credit side.

- In the discount columns, cash discount, i.e., cash discount allowed and cash discount received are recorded.

- The net amount received is entered in the amount column on the debit side and the net amount paid is entered in the amount column on the credit side.

- For the seller who allows cash discount, it is a loss and hence it is debited and shown on the debit side of the cash book.

- For the person making payment, discount received is a gain because less payment is made and it is credited and shown on the credit side of the cash book.

- The cash columns are balanced. Discount columns are not balanced, since debit represents discount allowed and credit represents discount received. They are totalled, separately.

The periodical totals of discount columns are posted as under:

- Debit Discount allowed account as ‘To Sundry Accounts as per Cash book’, with the periodical total of the discount allowed column.

- Credit Discount received account as ‘By Sundry Accounts as per Cash Book’ with the periodical total of the discount received column.

![]()

Question 5.

Briefly explain about contra entry with examples.

Answer:

1. When the two accounts involved in a transaction are cash account and bank account, then both the aspects are entered in cash book itself. As both the debit and credit aspects of a transaction are recorded in the cash book, such entries are called contra entries.

Example:

- When cash is paid into bank, it is recorded in the bank column on the debit side and in the cash column on the credit side of the cash book.

- When cash is drawn from bank for office use, it is entered in cash column on the debit side and in the bank column on the credit side of the cash book.

2. To denote that there are contra entries, the alphabet ‘C is written in L.F. column on both sides.

3. Contra means that particular entry is posted on the other side (contra) of the same book, because Cash account and Bank account are there in the cash book only and there are no separate ledger accounts needed for this purpose,

4. The alphabet ‘C’ indicates that no further posting is required and the relevant account is posted on the opposite side.

IV. Exercises

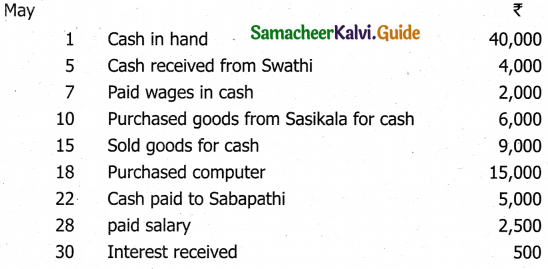

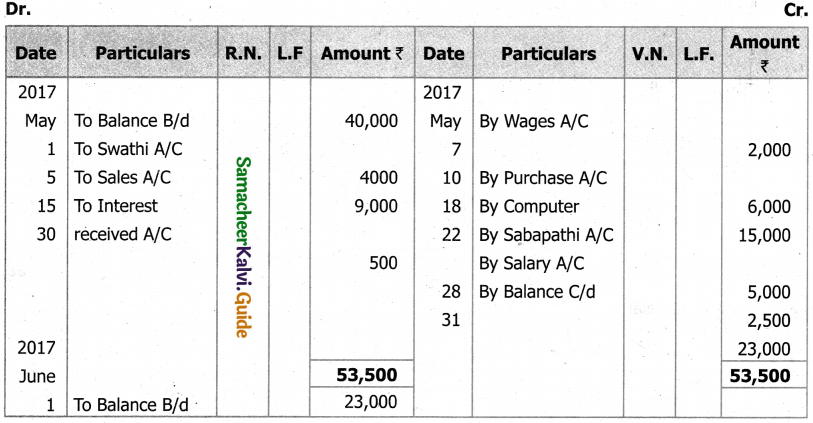

Question 1.

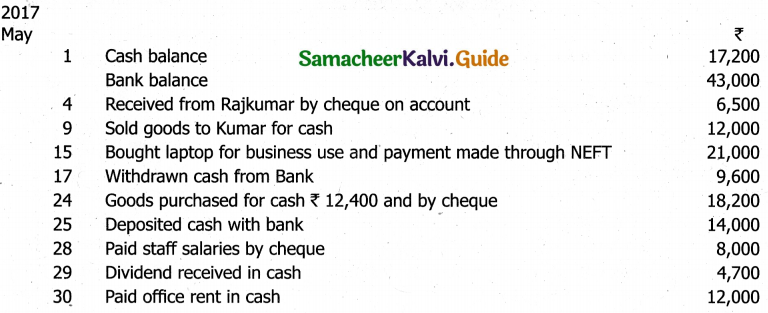

Enter the following transactions in a single column cash book of Seshadri for May, 2017.

Solution:

In the book of Seshadri

Cash book (single column)

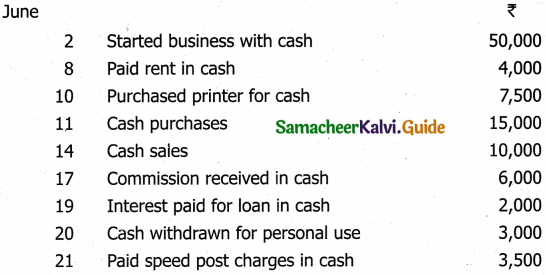

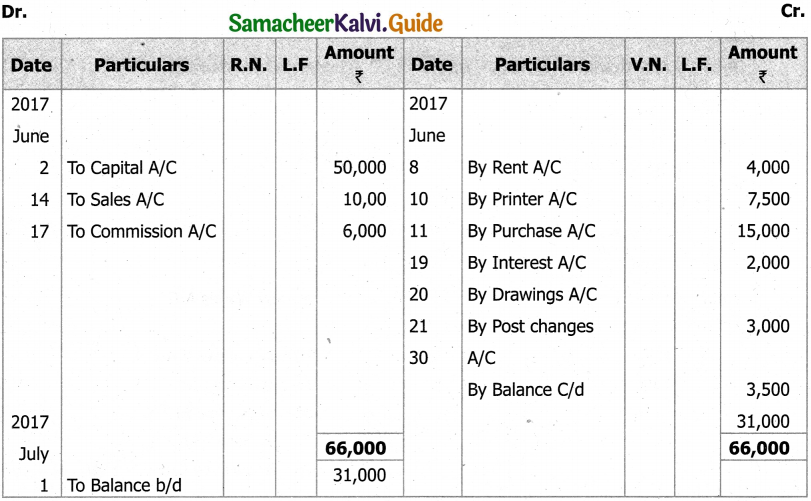

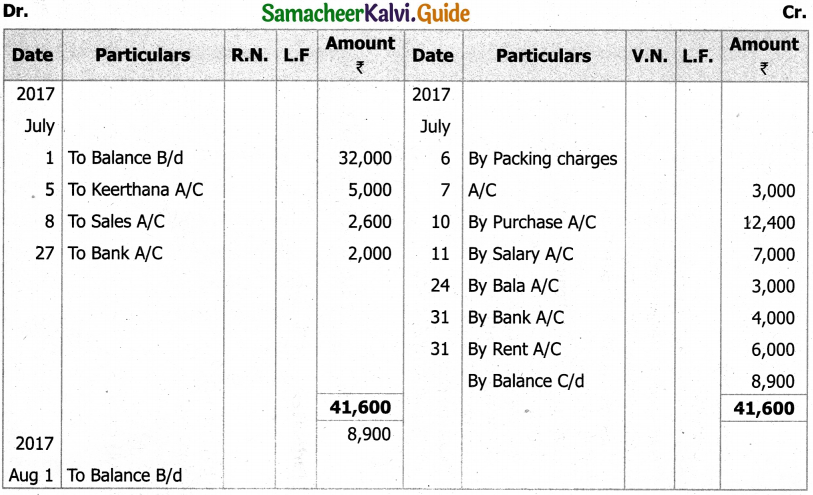

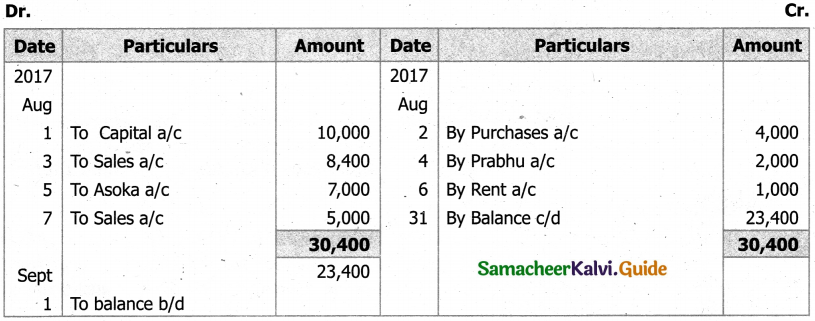

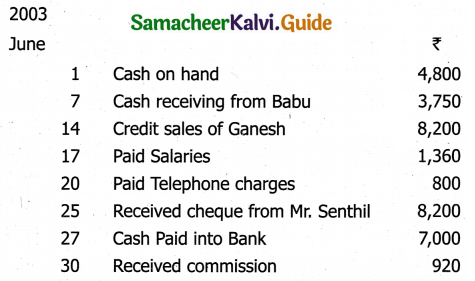

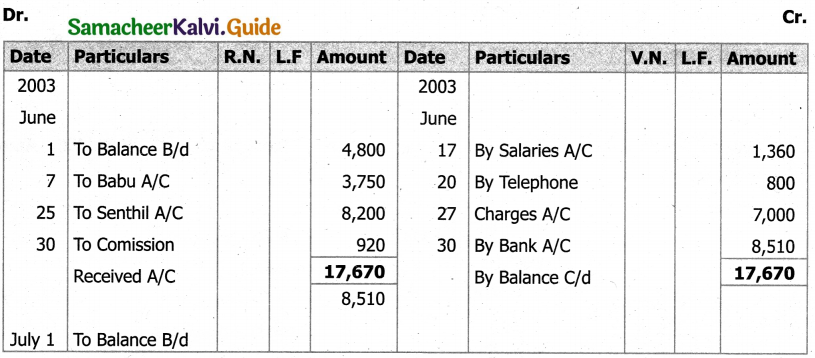

Question 2.

Enter the following transactions in a single column cash book of Pandeeswari for the month of June, 2017

Solution:

In the book of Pandeeswari

Cash book (single column)

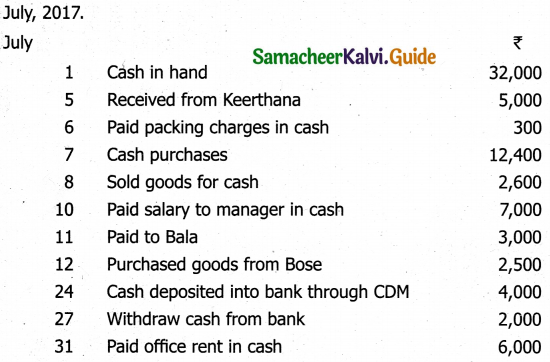

Question 3.

Enter the following transactions in a single column cash book of Ramalingam for month of July, 2017.

Solution:

Single column cash book of Mr. Ramalingam

Question 4.

Enter the following transaction in Chandran’s cash book with cash and discount columns.

Solution:

In the book of Mr. chandran

Cash book (with cash and discount columns)

Question 5.

Enter the following transaction in Chandran’s cash book with cash and discount column.

Solution:

In the book of Mr. chandran

Cash book (with cash and discount columns)

![]()

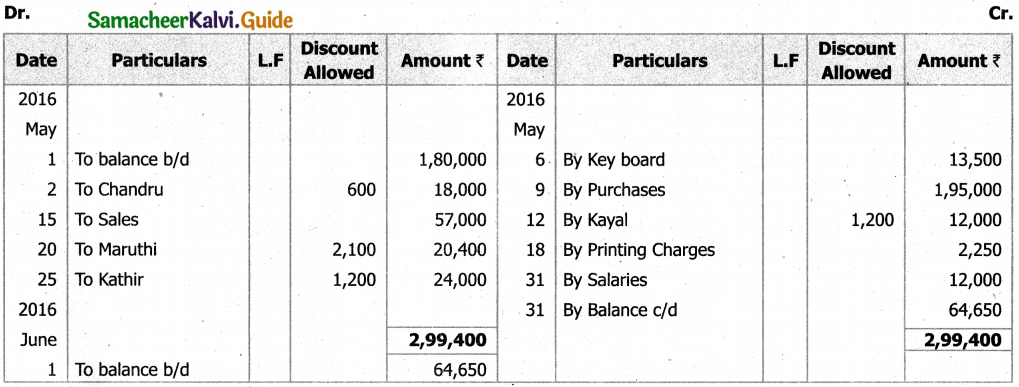

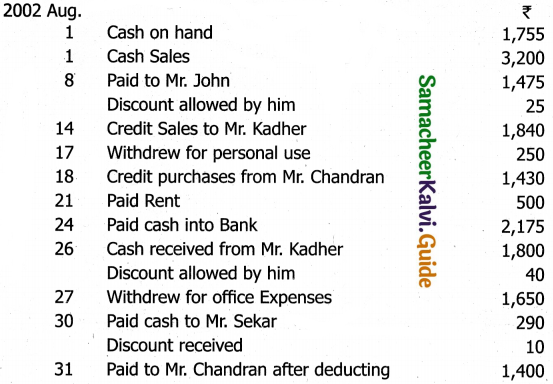

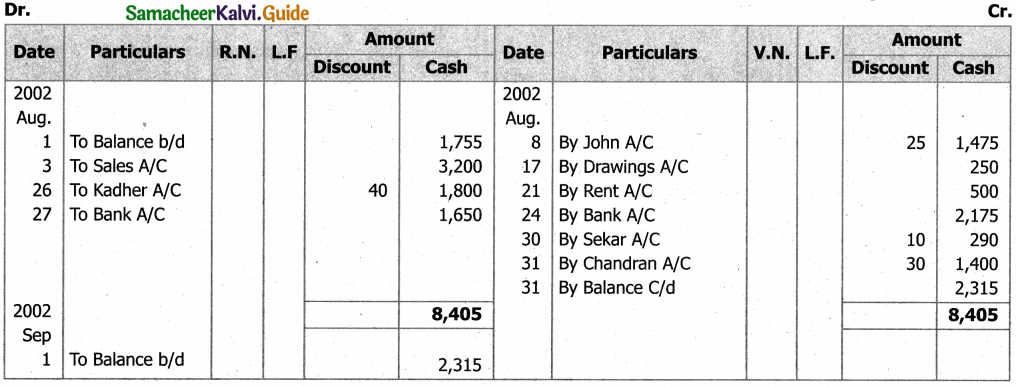

Question 6.

Enter the following transactions in cash book with discount and cash column of Anand.

Solution:

In the book of Anand

Cash book (with cash and Discount columns)

Question 7.

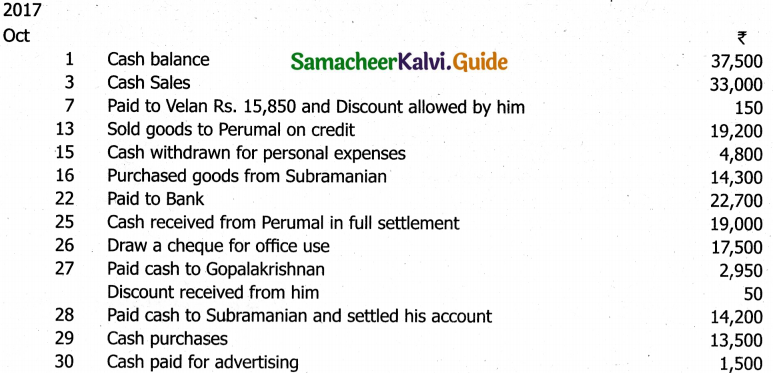

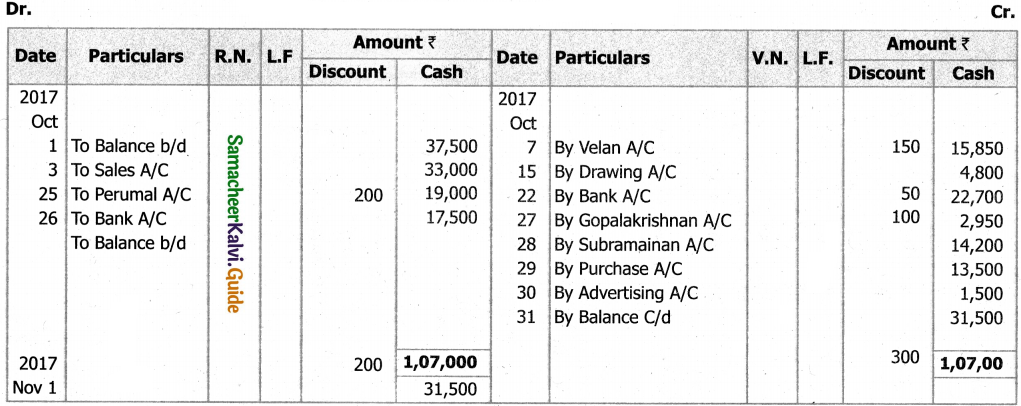

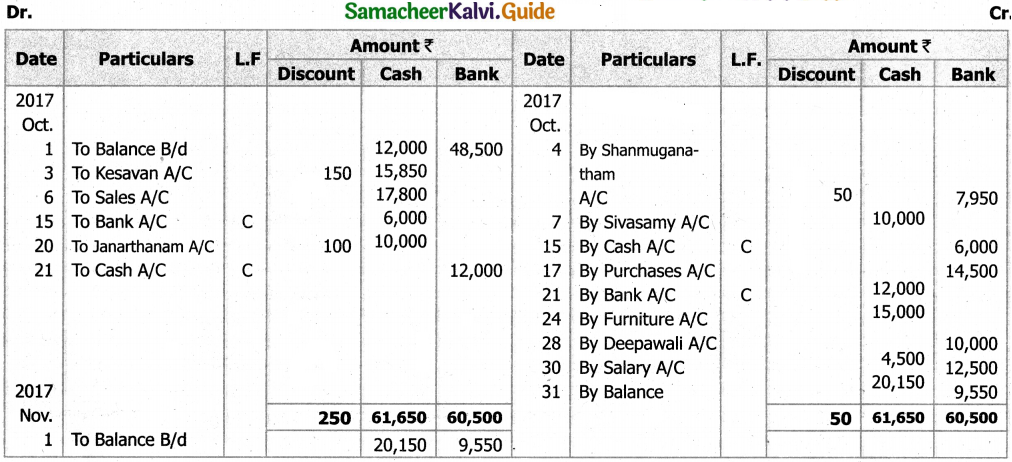

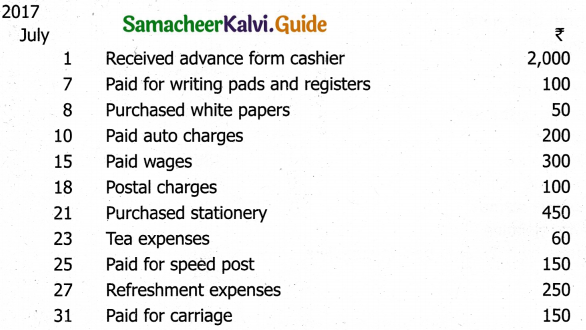

Write out a cash book with discount, cash and bank columns in the books of Mahendran. 2017 Oct?

Solution:

IIn the books of Mr. Mahendran

Three columns cash book

Question 8.

Enter the following transactions in the three column cash book of Kalyana Sundaram.

Solution:

IIn the books of Mr. Mahendran

Three columns cash book

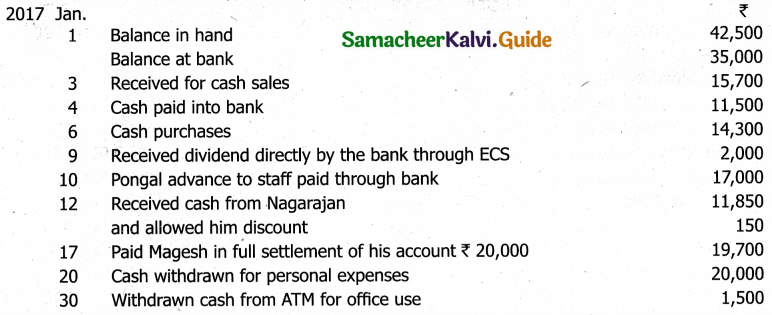

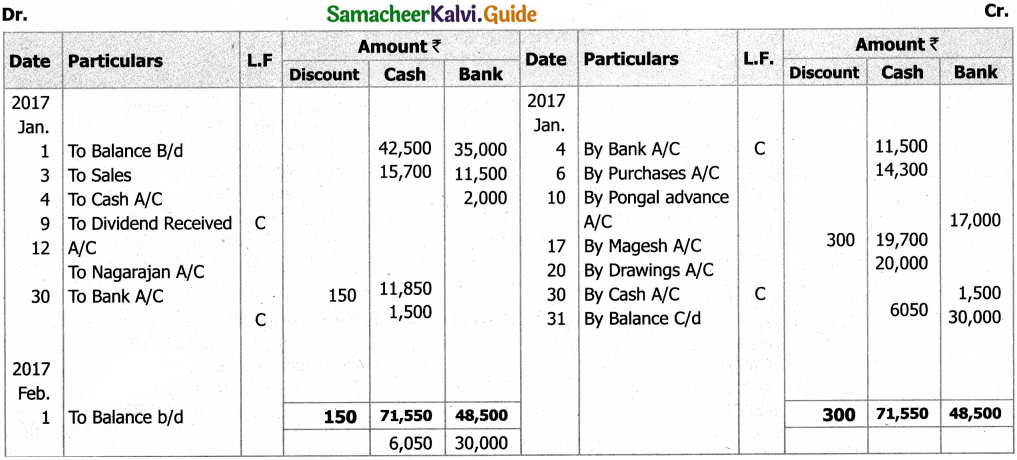

Question 9.

Enter the following transactions of Fathima in the cash book with a sh, bank and discount columns for the month of May, 2017.

Solution:

In the books of Fathima

Dr. Three columns cash book

Question 10.

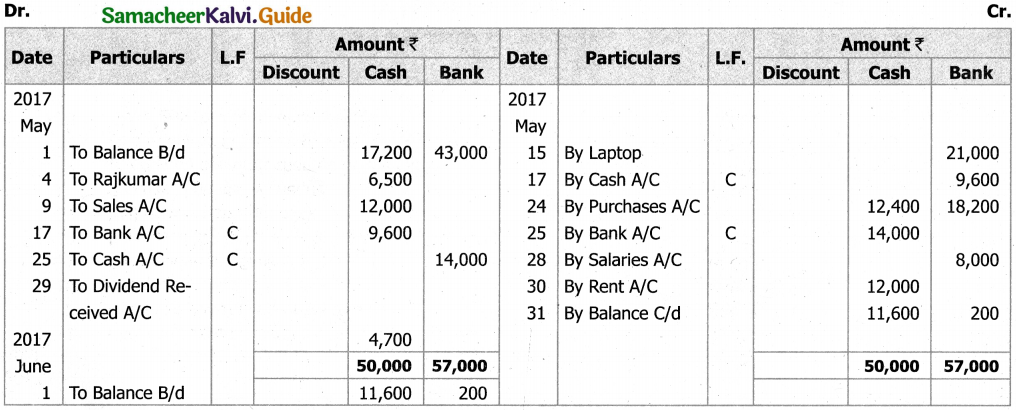

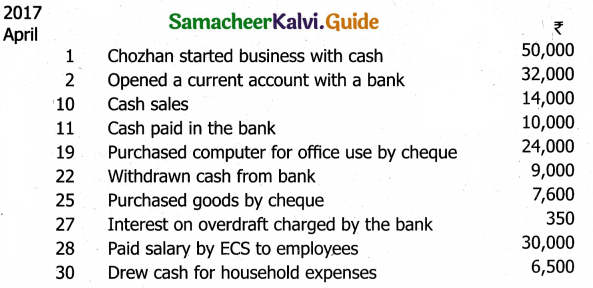

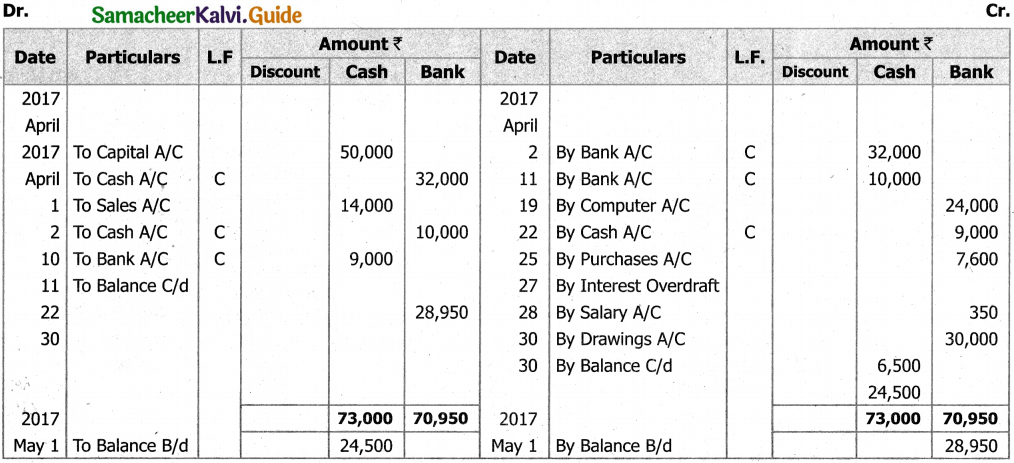

Enter the fallowing transactions in the three column cash book of Chozhan.

Solution:

In the books of Sri Chozhan

Three Columns Cash Book

![]()

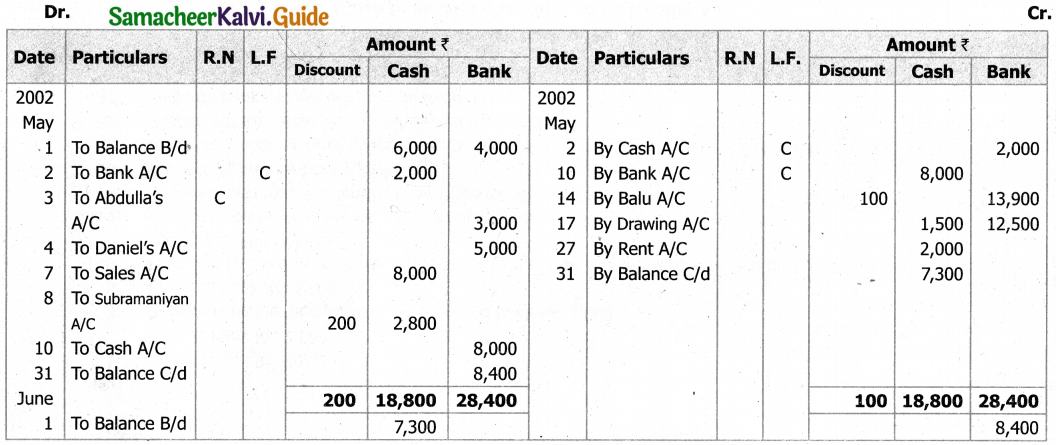

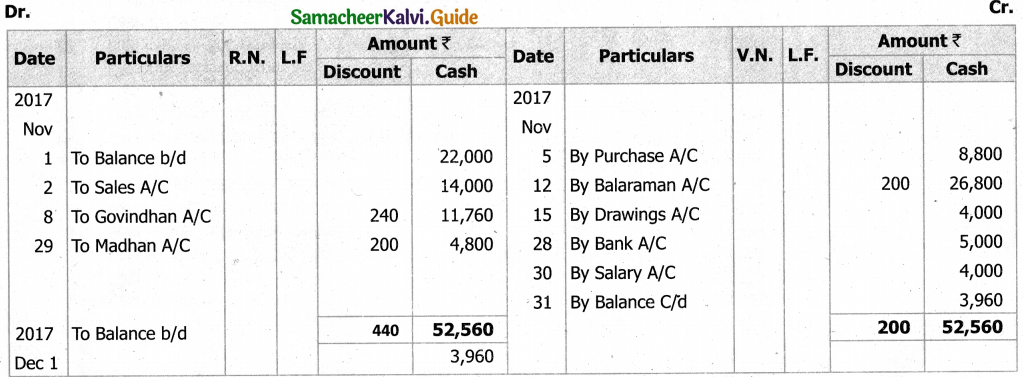

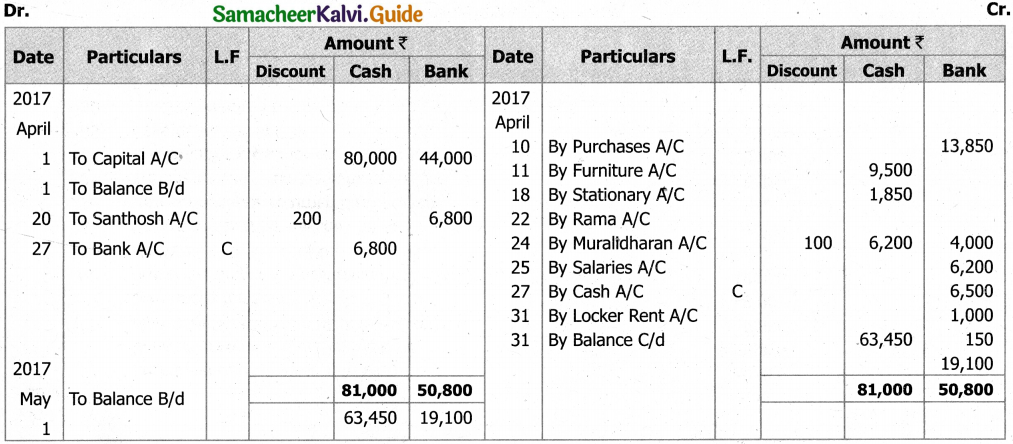

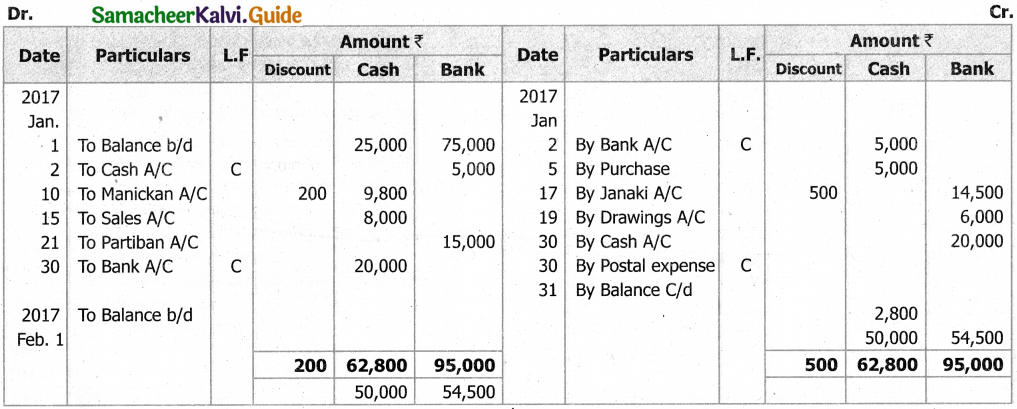

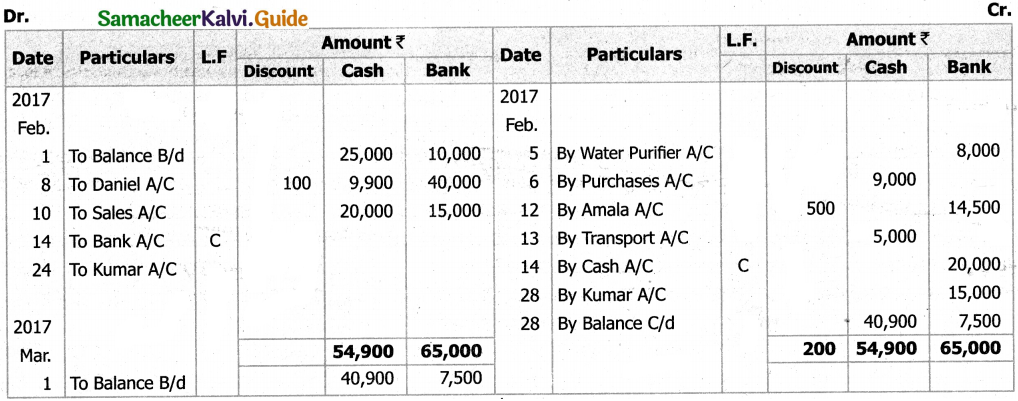

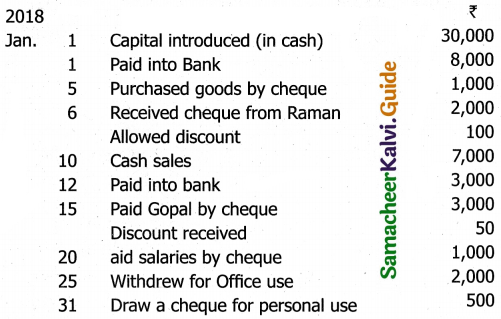

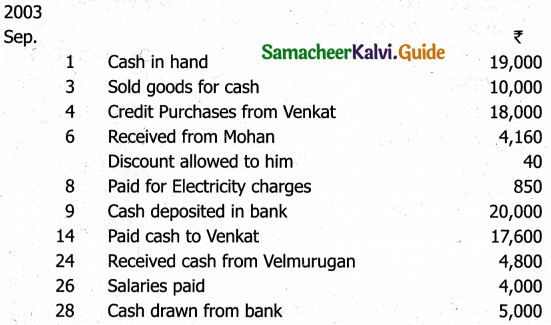

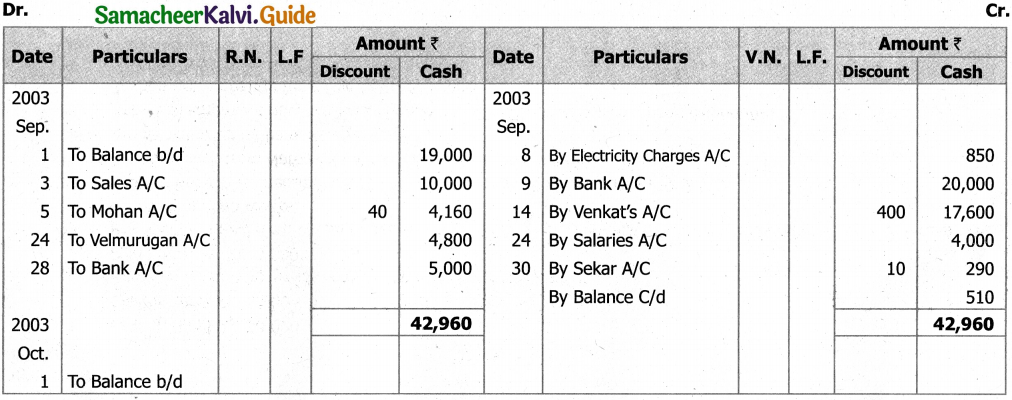

Question 11.

Enter the following transactions, in a cash book with cash, bank and discount columns of Sundari.

Solution:

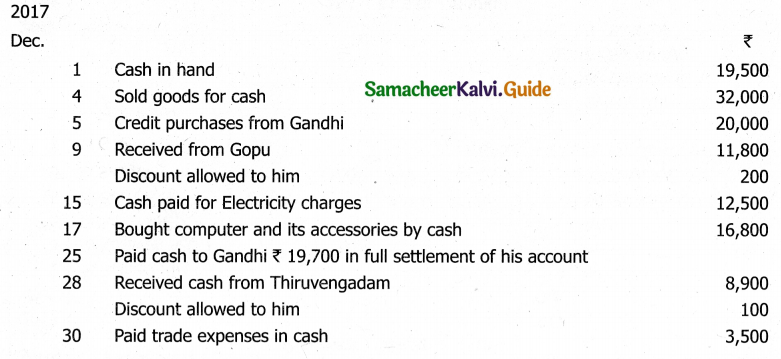

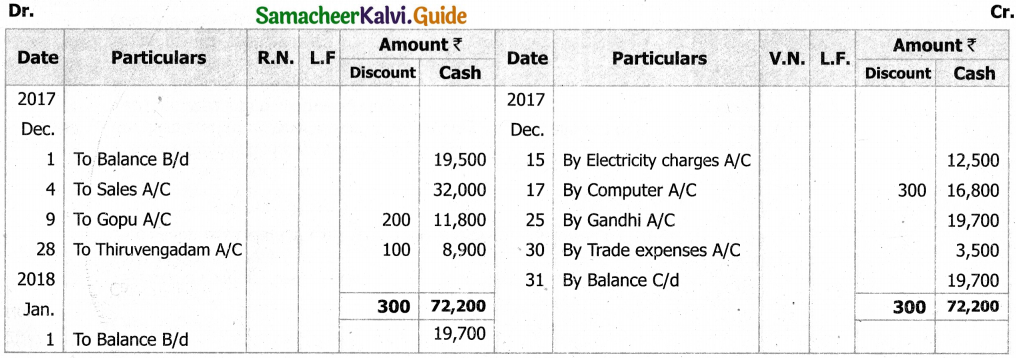

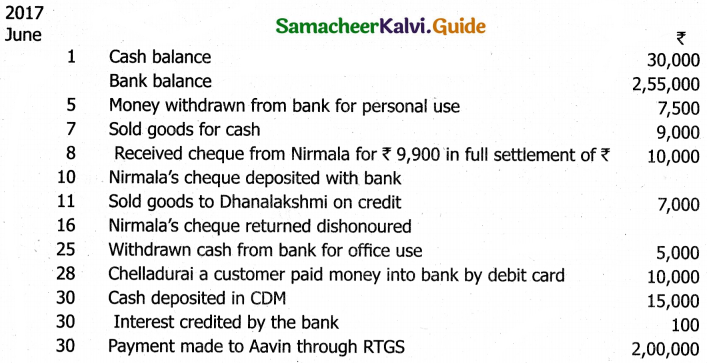

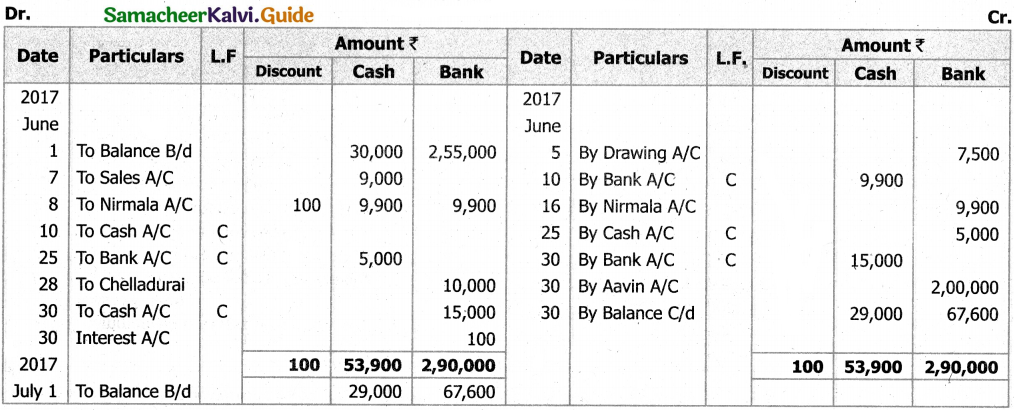

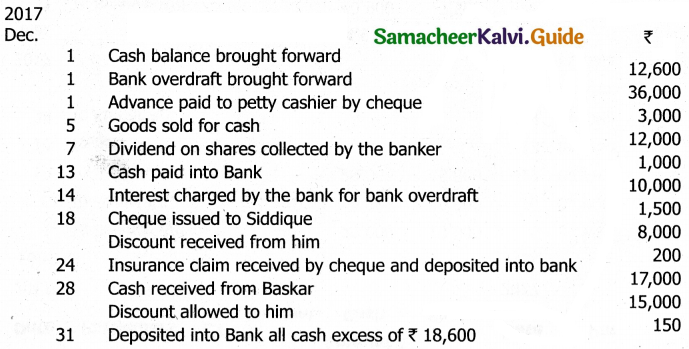

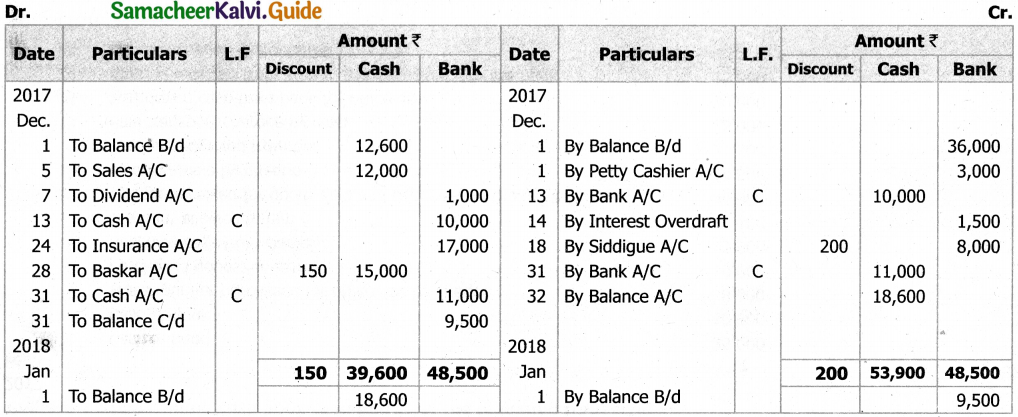

Question 12.

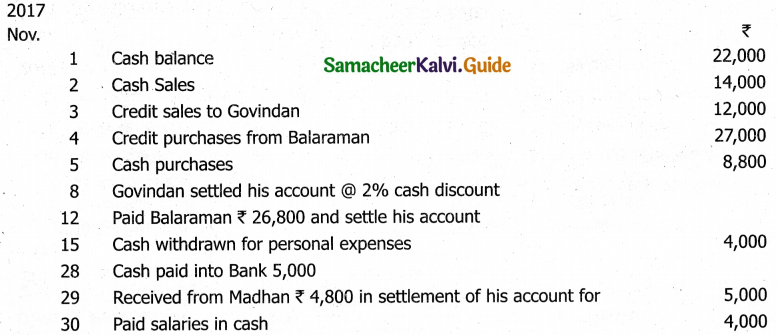

Record the following transaction in the three column cash book of Rajeswari for the month of June, 2017.

Solution:

In the book of Miss. Rajeswari

Three columns cash book

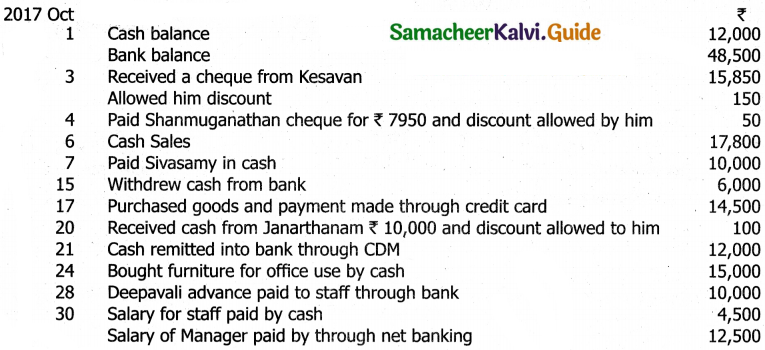

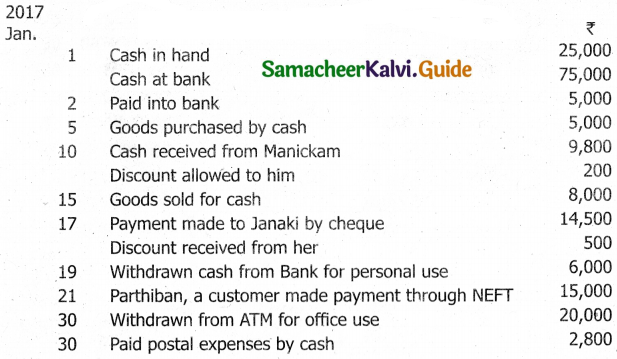

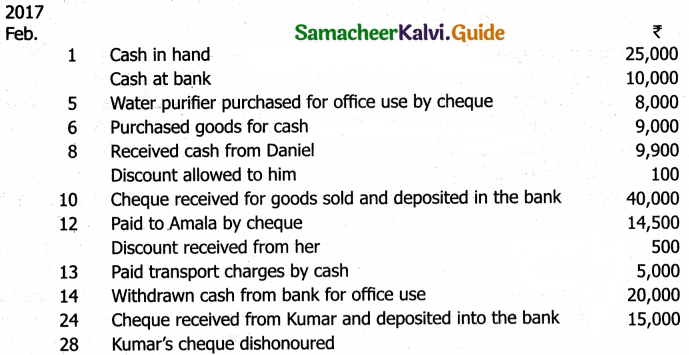

Question 13.

Record the following transactions in three column cash book of Ramachandran.

Solution:

In the book of Mr. Ramachandran

Three columns cash book

Question 14.

Record the. following transactions in the three column cash book of John Pandian.

Solution:

In the book of Mr. John Pandian

Three columns cash book

![]()

Question 15.

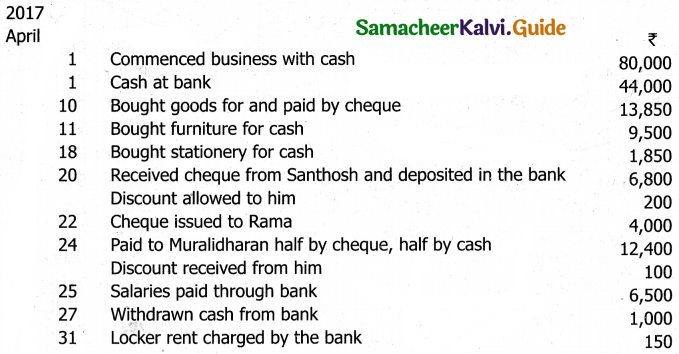

Prepare a triple column cash book of Rahim from the following transactions:

Solution:

In the book of Mr. Rahim

Three Columns cash book

Question 16.

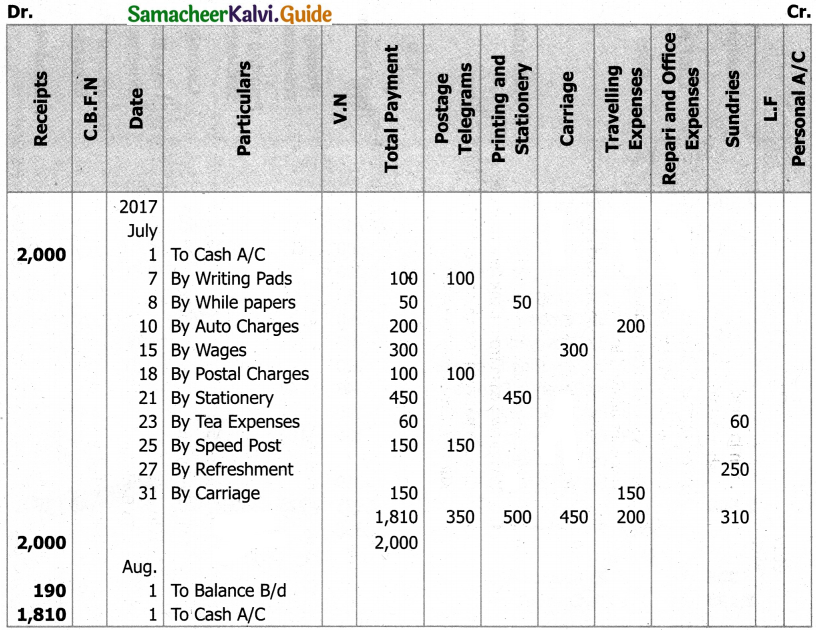

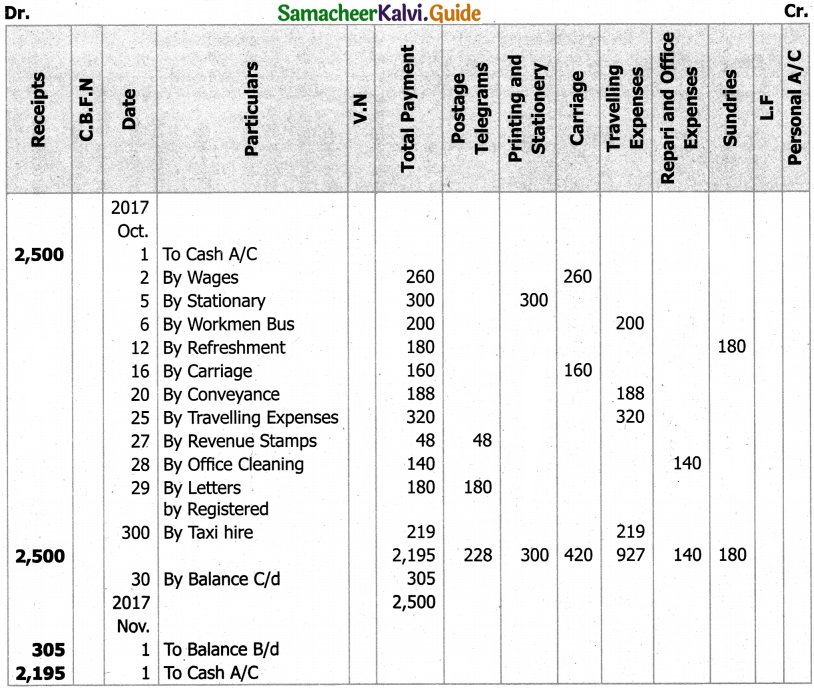

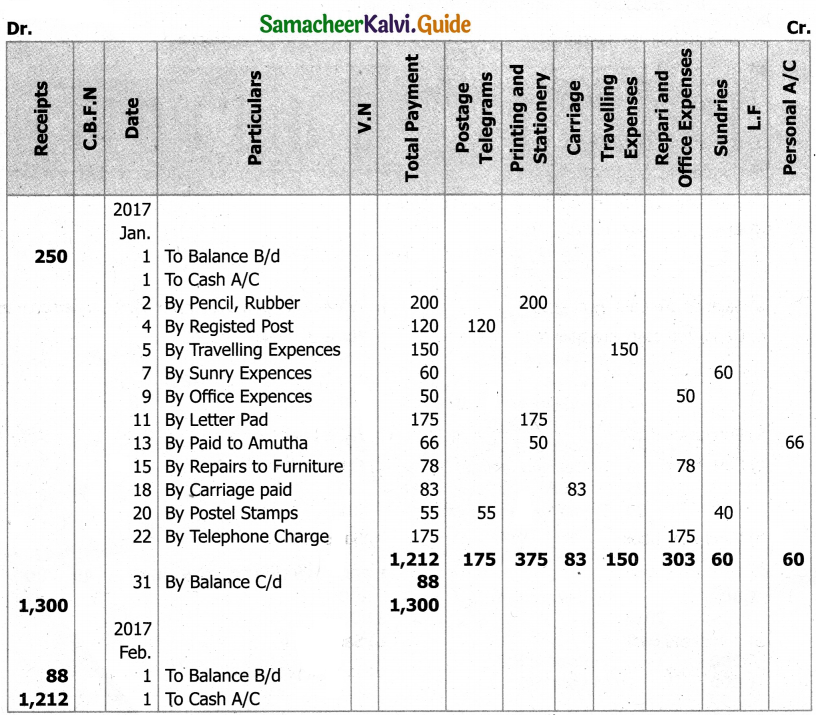

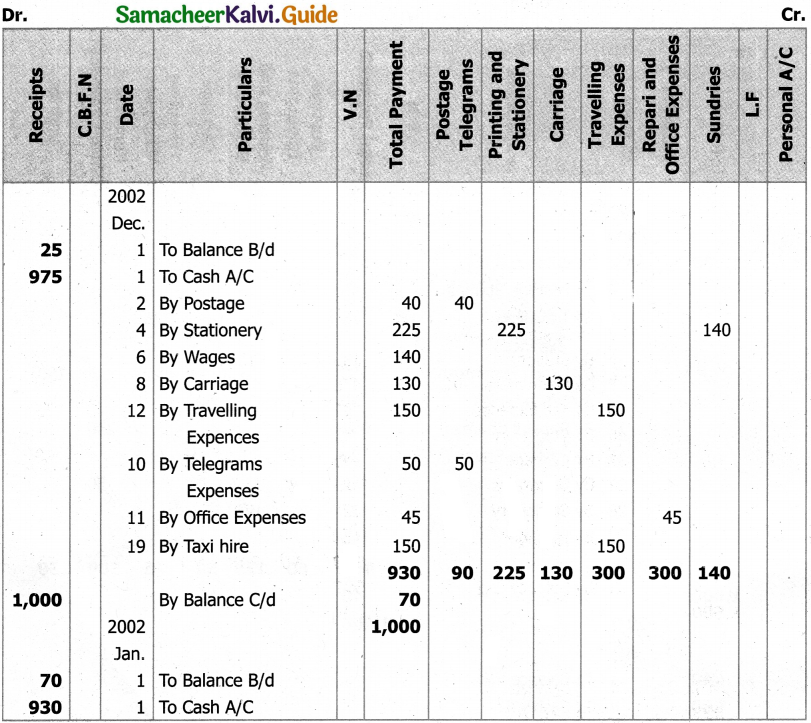

Prepare analytical petty cash book from the following particulars under imprest system:

Solution:

Analytical petty cash book – Analysis of payments (in ₹)

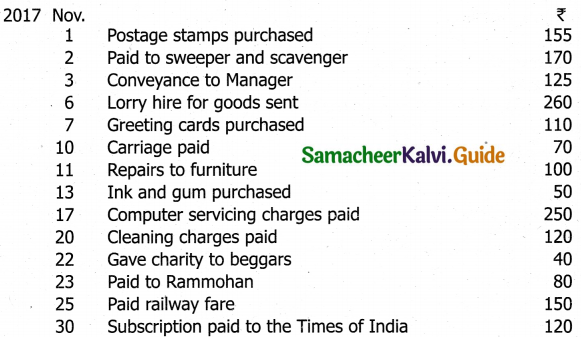

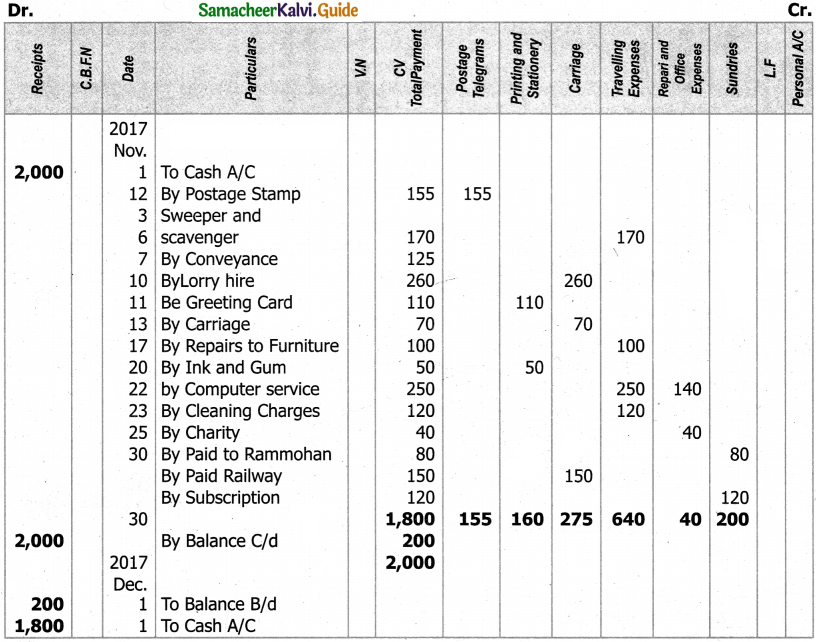

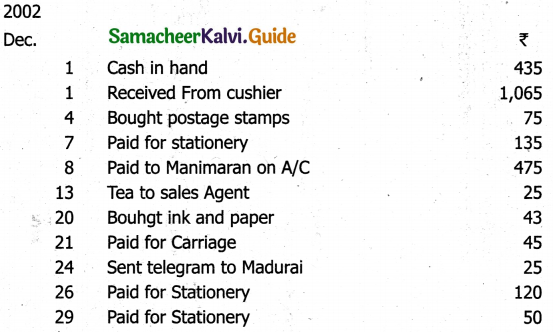

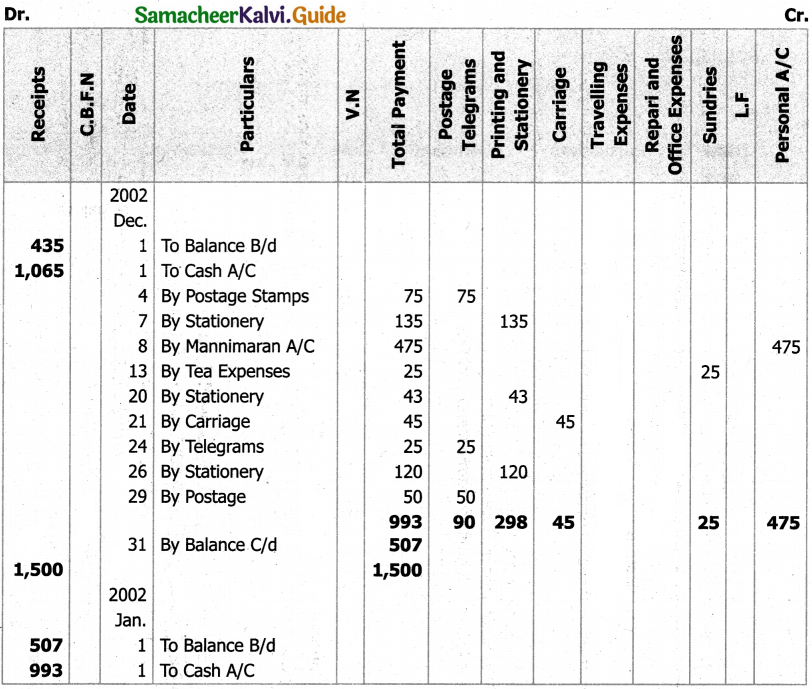

Question 17.

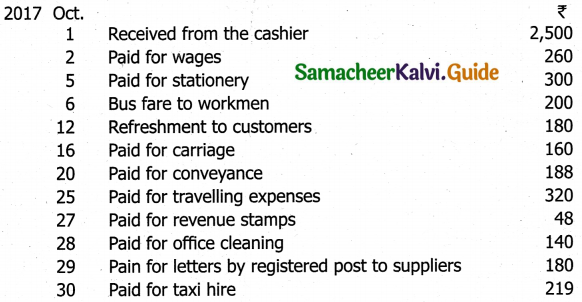

From the following information prepare an analytical petty cash book under imprest system:

Solution:

Analytical petty cash book – Analysis of payments

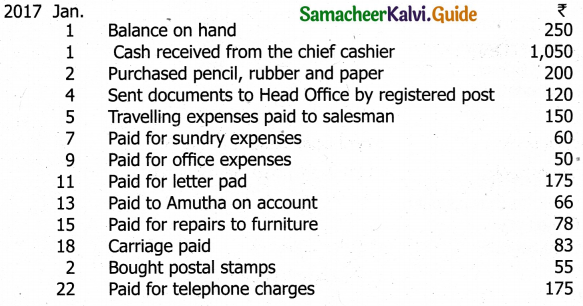

Question 18.

Record the following transactions in an analytical petty cash hook and balance the same. On 1st November, 2017, the petty cashier started with imprest cash ₹ 2,000.

Solution:

Analytical petty cash book – Analysis of payments

Question 19.

Enter the following transactions in Iyyappan’s petty cash hook with analytical columns under imprest system.

Solution:

![]()

11th Accountancy Guide Subsidiary Books – II Additional Important Questions and Answers

I. Choose the correct answer.

Question 1.

Cash Book is a type of ________ but treated as a ________ of accounts.

a) Subsidiary book, Principal book

b) Principal book, subsidiary book

c) Subsidiary book, subsidiary book

d) Principal book, principal book

Answer:

a) Subsidiary book, Principal book

Question 2.

The imprest system pertains to ________.

a) Purchases book

b) Sales book

c) Cash book

d) Petty cash book

Answer:

d) Petty cash book

Question 3.

While balancing three column cash book, the discount columns are:

a) Totalled but not adjusted

b) Totalled and also adjusted

c) Totalled but not balanced

d) Balanced but not totalled

Answer:

c) Totalled but not balanced

Question 4.

In three column cash book, when does contra entry occur?

a) Withdrawal of cash from bank

b) Payment to creditors

c) Withdrawal of cash from bank for personal use

d) All of the above

Answer:

a) Withdrawal of cash from bank

Question 5.

Double entry in cash book is completed when:

a) Salaries are paid by cheque

b) Withdrawal of money from bank for personal use

c) Deposited cash into bank

d) None of these

Answer:

c) Deposited cash into bank

![]()

Question 6.

A book where small items of expenditure like postage, carriage, coolies, stationery etc., are entered is called ________.

a) Purchases book

b) Sales book

c) Cash book

d) Petty cash book

Answer:

d) Petty cash book

Question 7.

Cash sales are entered in the ________.

a) Purchases book

b) Sales book

c) Cash book

d) Petty cash book

Answer:

c) Cash book

Question 8.

Cash discount is recorded in the ________.

a) Purchases book

b) Sales book

c) Cash book

d) Journal proper

Answer:

c) Cash book

Question 9.

Subsidiary books are maintained in ________.

a) Big business concerns

b) Small business concerns

c) Banks

d) None of the above

Answer:

a) Big business concerns

Question 10.

Which of the following books should be used to record purchase of furniture on credit?

a) Purchases book

b) Goods account

c) Cash book

d) Journal proper

Answer:

d) Journal proper

Question 11.

The credit balance in the Bank account is ________.

a) An asset

b) A liability

c) An expense

d) None of the above

Answer:

b) A liability

Question 12.

Double entry means ________.

a) Entry in two sets of books

b) Entry in two pages

c) Entry for two aspects of a transaction

d) None

Answer:

c) Entry for two aspects of a transaction

Question 13.

Which of the following is not true?

a) Double Column cash book contains cash and bank columns

b) Discount columns are not balanced

c) The dosing balance of bank columns is called cash at bank

d) None of the above

Answer:

a) Double Column cash book contains cash and bank columns

![]()

Question 14.

Dishonour of a discounted bill, not recorded in the cash book will be added in the BRS, if the balance given is ________.

a) Unfavourable balance as per cash book

b) Favourable balance as per Pass book

c) Both (a) & (b)

d) None of the above

Answer:

c) Both (a) & (b)

Question 15.

The total of the purchases day book is posted periodically to the debit of ________.

a) Purchases account

b) Journal proper

c) Cash book

d) None of these

Answer:

a) Purchases account

Question 16.

Goods given as charity should be credited to ________.

a) Purchases account

b) Journal proper

c) Cash book

d) Charity Account

Answer:

a) Purchases account

Question 17.

“Bills payable discounted in cash by creditor”. This transaction will be recorded in ________.

a) Journal

b) Ledger

c) Bank book

d) No entry required to be made

Answer:

d) No entry required to be made

Question 18.

Contra entries are passed only when ________.

a) Double column cash book is prepared

b) Three-column cash books is prepared

c) Simple Cash book is prepared

d) None of these

Answer:

b) Three-column cash books is prepared

Question 19.

Which of the following is a type of cash receipt journal + cash payment journal?

a) Bank Statement

b) Cash flow statement

c) Cash book

d) None of these

Answer:

c) Cash book

Question 20.

Credit balance of the bank column in cash book shows:

a) Overdraft

b) Cash deposited in the bank

c) Cash withdrawn from the bank

d) None of these

Answer:

a) Overdraft

Question 21.

A cash book with discount and cash column is called ________.

a) Simple cash book

b) Double column cash book

c) Three column cash book

d) Petty cash book

Answer:

b) Double column cash book

![]()

Question 22.

When goods are purchased for cash, the entry will be recorded in the ________.

a) Cash book

b) purchases book

c) Sales book

d) journal

Answer:

a) Cash book

Question 23.

The balance of cash book indicates ________.

a) Net income

b) cash in hand

c) Debtors

d) creditors

Answer:

b) cash in hand

Question 24.

In triple column cash book, cash withdrawn from bank for office use Will appear in ________.

a) Debit side of the cash book only

b) both sides of the cash book,

c) Credit side of the cash book only.

d) Journal proper

Answer:

b) both sides of the cash book,

Question 25.

If a cheque sent for collection is dishonoured, the debit is given to ________.

a) suppliers A/c

b) bank A/c

c) customers A/c

d) A and B

Answer:

c) customers A/c

Question 26.

If a cheque issued by us is dishonoured the credit is given to ________.

a) supplier’s A/c

b) customer’s A/c

c) bank A/c

d) A and B

Answer:

a) supplier’s A/c

Question 27.

Cash book always shows.

a) debit balance

b) credit balance

c) nill balance

d) credit balance and debit balance

Answer:

a) debit balance

Question 28.

Bank book always shows ________.

a) debit balance

b) credit balance

c) nil balance

d) credit balance and debit balance

Answer:

d) credit balance and debit balance

Question 29.

On Jan 1st 2017, Rs.1,000 given to petty cashier. He has spent Rs.960during the month of January. On Feb 1st to make the imprest he will receive cheque for Rs. ________.

a) Rs. 1,000

b) Rs. 960

c) Rs. 1,960

d) Rs. 40

Answer:

b) Rs. 960

Question 30.

The dosing balance of petty cash book is considered as ________.

a) Liability

b) Asset

c) Expenses

d) Income

Answer:

b) Asset

![]()

Question 31.

Payment of rent expenses is recorded on which side of cash book ?

a) Receipts

b) Payments

c) Income

d) Expense

Answer:

b) Payments

Question 32.

The most common imprest system is the ________ systems.

a) pretty cash

b) cash book

c) cash receipt

d) discount

Answer:

a) pretty cash

![]()

II. Short Answer Questions

Question 1.

Enter the following transactions in the simple column cash book.

Solution:

III. Additional Questions & Answers

Question 1.

What is the importance’s of cash book?

Answer:

Serves as both journal and ledger – When cash book is maintained, it is not necessary to open a separate cash account in the ledger. Thus, cash book serves the purpose of a journal and a ledger.

Saves time and labour – When cash transactions are recorded through journal entries, a lot of time and labour will be involved. To avoid this, all cash transactions are straightaway recorded in the cash book, which saves time and labour.

Shows the cash and bank balance – It helps to know the cash and bank balance at any point of time by comparing the total cash receipts and cash payments.

Benefit of division of labour – As cash book is a separate subsidiary book, an independent person can maintain it. Hence, business can get the benefit of division of labour.

Effective cash management – Cash book provides all information regarding total receipts and payments of the business concern during a particular period. It helps in formulating effective policy for cash management.

Prevents errors and frauds – Balance as per cash book and the balance in the cash box can be compared daily. If there is any deficit or surplus, it can be found easily. It helps in preventing any fraud or error in cash dealings.

Question 2.

What are the various types of petty cash book?

Answer:

There are two types of petty cash books. They are:

- Simple petty cash book

- Analytical petty cash book

Simple petty cash book –

A simple petty cash book resembles the single column cash book. But the columns are different. On the debit side, only the advance received from the head cashier is recorded. On the credit side, all payments are recorded in only one column. This is known as simple petty cash book.

Analytical petty cash book –

In analytical petty cash book, a separate column is provided for different heads of payments and one column for total payments. When the petty expenses are recorded in the total payment column, same amount is also recorded in the appropriate expense column. This is known as analytical petty cash book.

![]()

Question 3.

What is Simple petty cash hook?

Answer:

A simple petty cash book resembles the single column cash book. But the columns are different. On the debit side, only the advance received from the head cashier is recorded. On the credit side, all payments are recorded in only one column. This is known as simple petty cash book.

Question 4.

What is Analytical petty cash book?

Answer:

In analytical petty cash book, a separate column is provided for different heads of payments and one column for total payments. When the petty expenses are recorded in the total payment column, same amount is also recorded in the appropriate expense column. This is known as analytical petty cash book.

Question 5.

Give any two Examples for a Contra Entry.

Answer:

- Cash paid into bank.

- Money withdrawn from bank for office use.

Additional Sums:

Question 1.

Enter the following in the simple column cash book.

Solution:

Single Column Cash Book

Question 2.

Enter the Following transactions in a petty cash book of Mr, Kishore Kumar with analytical columns the petty cashier beigns with an imprest amount of Rs.1,000.

Solution:

Question 3.

Prepare petty cash book on imperst system from the Following Particulars given below.

Solution:

Question 4.

Prepare the analytical petty cash book of Mr. Keerthivasan from the Following.

Solution:

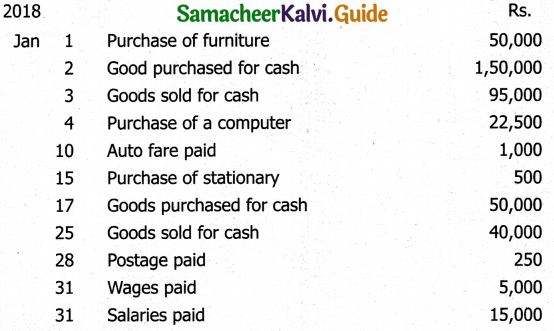

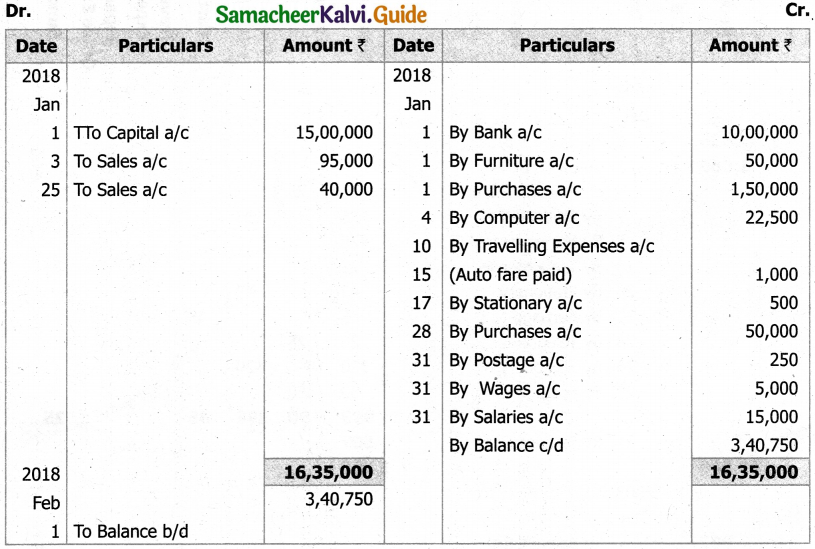

Question 5.

Thiru.Suganthan started business with the capital of Rs.15,00,000 on 01.01.2018. He paid into Bank Rs.10,00,000. He tarried out the following transactions during the month is given below; prepare the cash of Suganthan.

Solution:

Single Column Cash Book of Mr. Suganthan

![]()

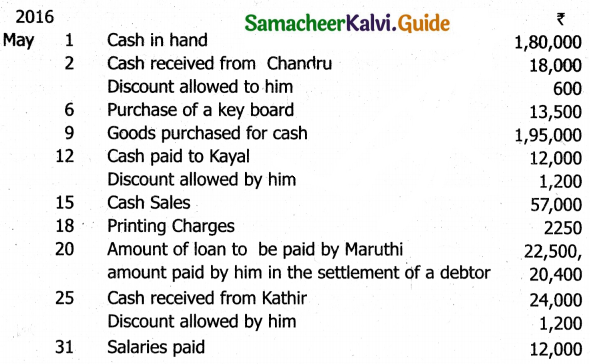

Question 6.

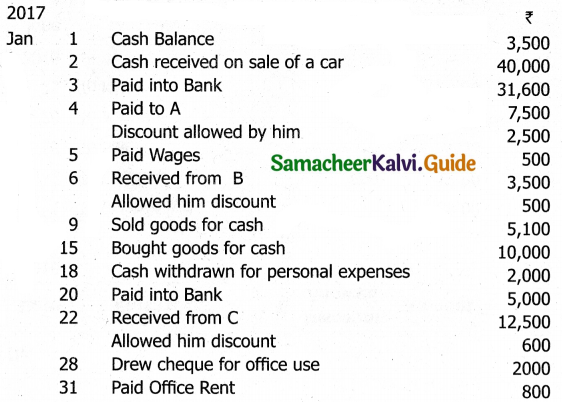

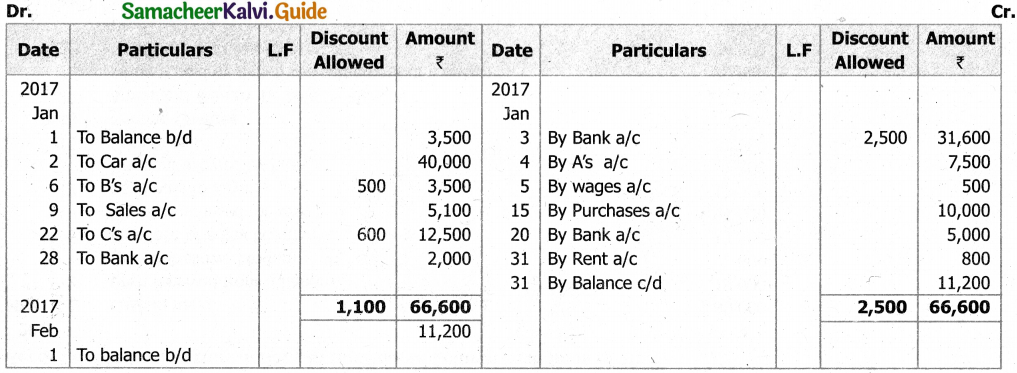

Enter the lowing transactions of Royce in Double Column Cash Book.

Solution:

Double Column Cash Book of Royce

Question 7.

Record the following transactions in the Double CoSusium cash book of Mr. X

Solution:

Double Column Cash Book of Mr. X

Question 8.

Enter the following transactions of a trader in a triple column cash book.

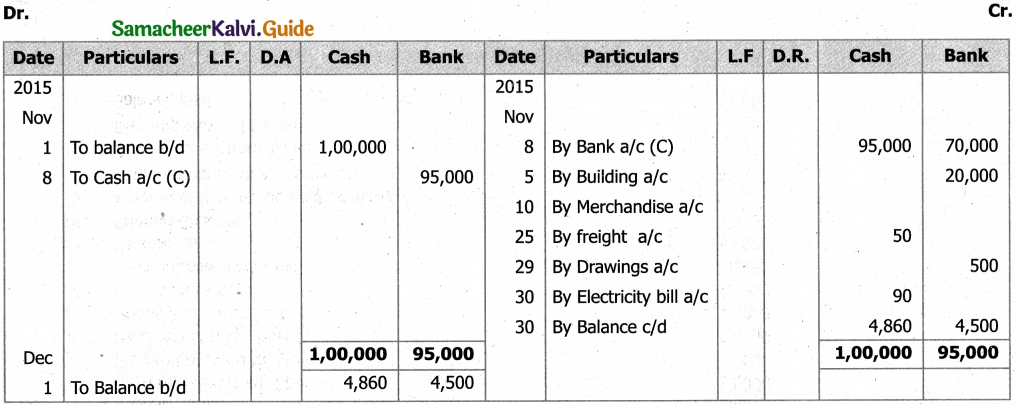

2015,

Nov.

1 – Nizam started business with ₹ 1,00,000

2 – Deposited into bank of Baroda ₹ 95,000

5 – Purchased a building for ₹ 70,000 and paid by cheque

10 – Purchased merchandise ₹ 20,000 and paid by cheque

25 – Paid freight ₹ 50

29 – Withdrew from bank for personal use ₹ 500

30 – Cleared electricity bills ₹ 90

Solution:

Cash Book of a Trader

Question 9.

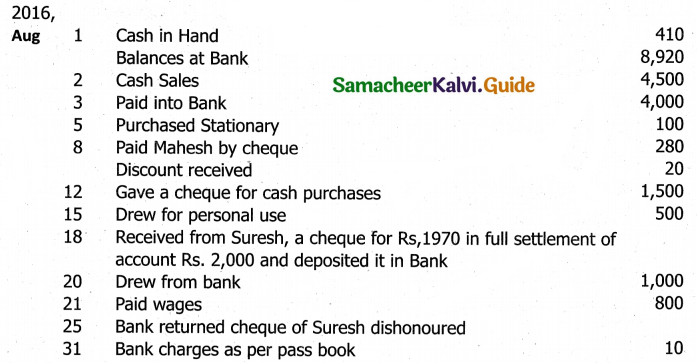

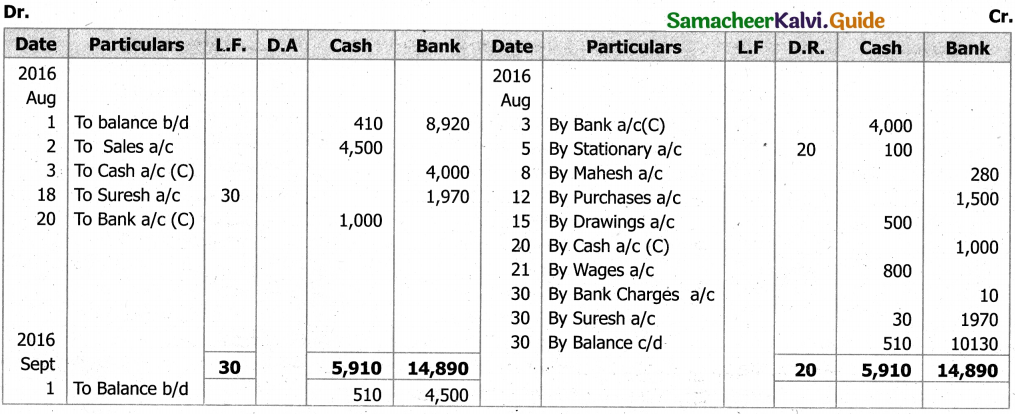

Enter the following transactions in the three columnar cash book of Mr.Z

Solution:

Three Column Cash Book of Mr.Z

Question 10.

Enter the following transactions in Gopi’s Three Column Cash Book:

Solution:

Three Column Cash Book of Mr.Z

![]()

Question 11.

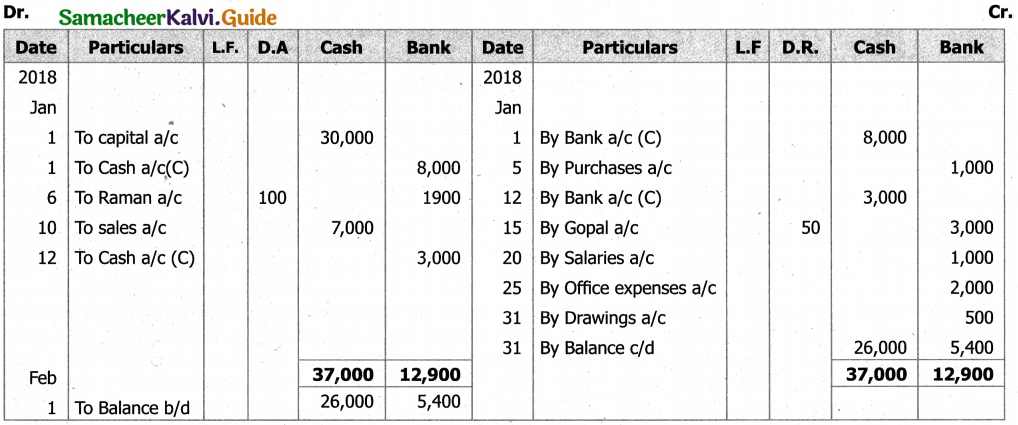

Enter the following transactions in cash book of Mr. K with cash, bank and discount columns

2018

Feb.

1 – Cash in hand Rs. 1,60,000

3 – Opened bank account with Rs. 70,000

5 – Cash purchases Rs. 1,00,000

6 – Cash Sales Rs. 1,30,000

14 – Withdrew cash for office use Rs. 20,000

20 – Sold goods to Sundar Rs. 90,000

25 – Cash received from Sundar Rs. 88,000 in full settlement

28 – Paid Salaries Rs. 30,000

29 – With drew Rs. 10,000 from bank for domestic purpose

30 – Paid Rent Rs. 10,000

31 – Paid to Prabhu Rs. 37,000 in full settlement against his claim of Rs. 40,000 during 2017

Solution:

Triple Column Cash Book of Mr. K

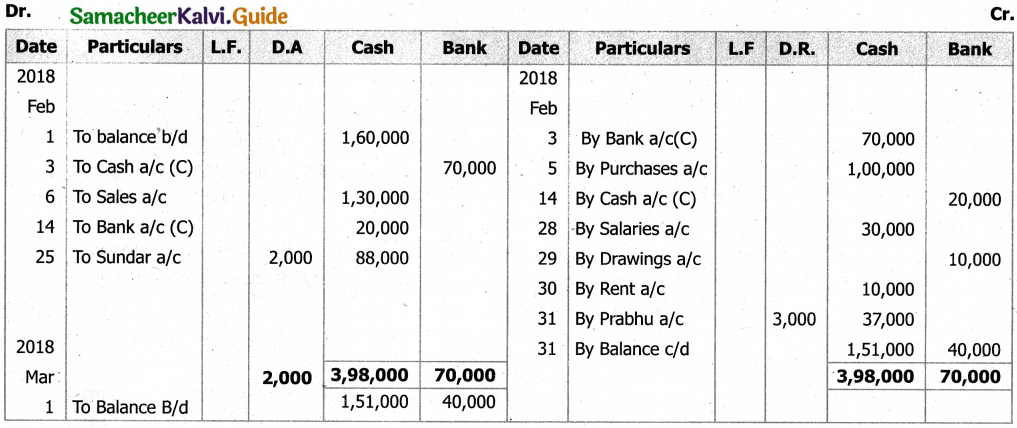

Question 12.

Enter the following transactions in Ganesan’s cash book with columns for cash, bank and discount:

2017

Nov

1 – Balance in cash on hand Rs. 400 and at Bank Rs. 3,600

3 – Received Rs. 1,600 from Gopalan in cash; Allowed him discount of Rs. 20

3 – Paid Rs. 1,000 into bank

4 – Cash sales Rs. 1,200

5 – Paid salaries by cheque Rs. 1,600

6 – Repairs of typewriter Rs. 600

8 – Paid Rs. 1,200 to Modern Co., half in cash and half in cheque

Solution:

Triple Column Cash Book of Mr.Ganeshan

Question 13.

From the following particulars prepare analytical column of petty cash book of Mr. Z:

2017

Dec

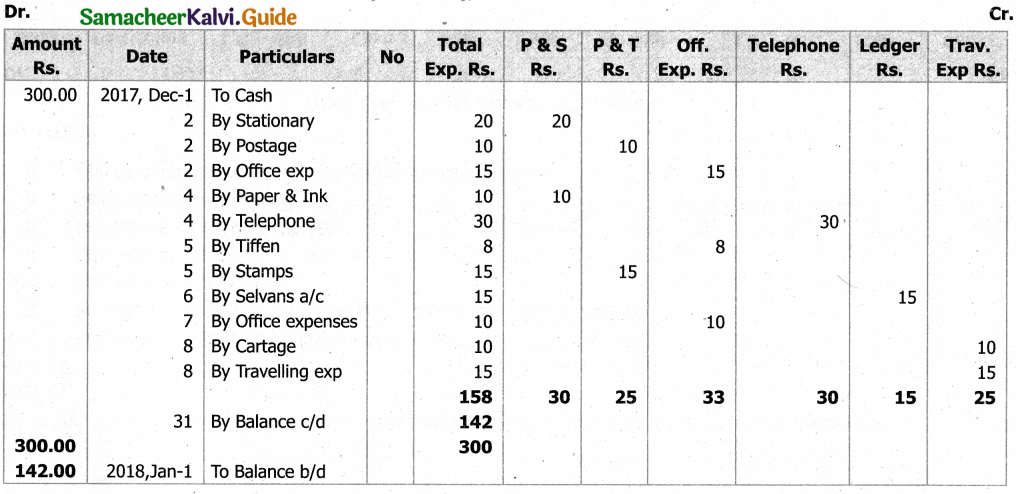

1 – Received from head cashier Rs. 300

2 – Paid for stationary Rs. 20; Postage and telegram paid Rs. 10; Paid office expenses Rs. 15

4 – Bought paper and ink Rs. 10

5 – Paid for Tiffen to office peon Rs. 8; Bought postage stamps Rs. 15

6 – Paid Selvan on account Rs. 15

7 – Paid for miscellaneous office expenses Rs. 10

8 – Paid Cartage Rs. 10; Paid travelling expenses Rs. 15

Solution:

Analytical Petty Cash Book of Mr. Z

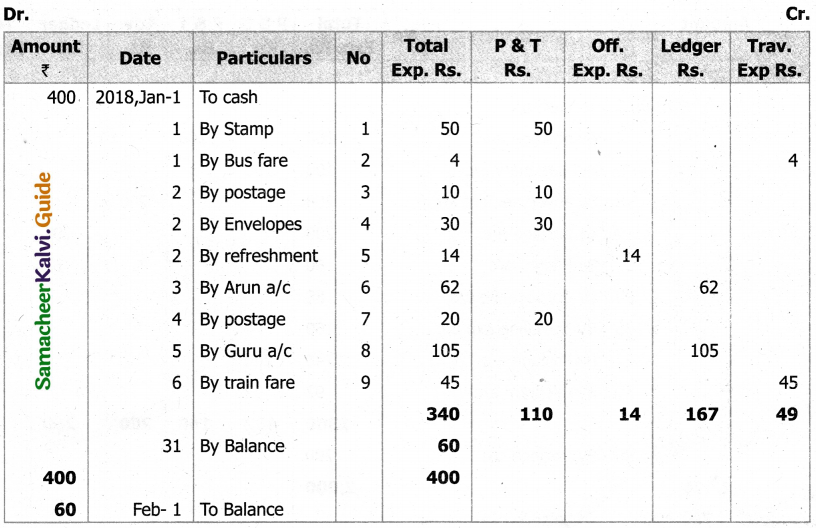

Question 14.

Lakshman, maintains a columnar petty cash book on the imprest system. The imprest amount is Rs.400. From the following information write up the petty cash book for the 1st Week of January 2018.

Jan

2018

1 – Bought stamps Rs. 50 (Voucher No.l)

2 – Paid bus fares Rs. 4 (Voucher No.2)

2 – Paid postages Rs. 10 (Voucher No.3)

2 – Paid envelopes Rs. 30 (Voucher No.4)

2 – Paid for refreshment Rs. 14 (Voucher No.5)

3 – Paid Arun a creditor Rs. 62 (Voucher No.6)

4 – Paid for postage Rs. 20 (Voucher No.7)

5 – Paid Guru a creditor Rs. 105 (Voucher No.8)

6 – Paid train fares Rs. 45 (Voucher No.9)

7 – Restored imprest

Solution:

Analytical Petty Cash Book of Mr. Lakshman

Question 15.

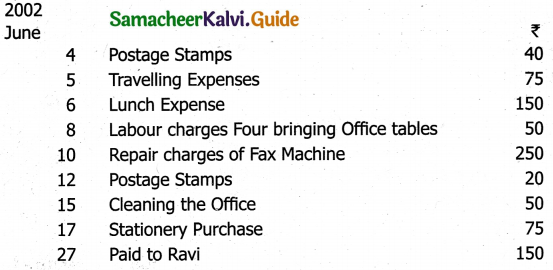

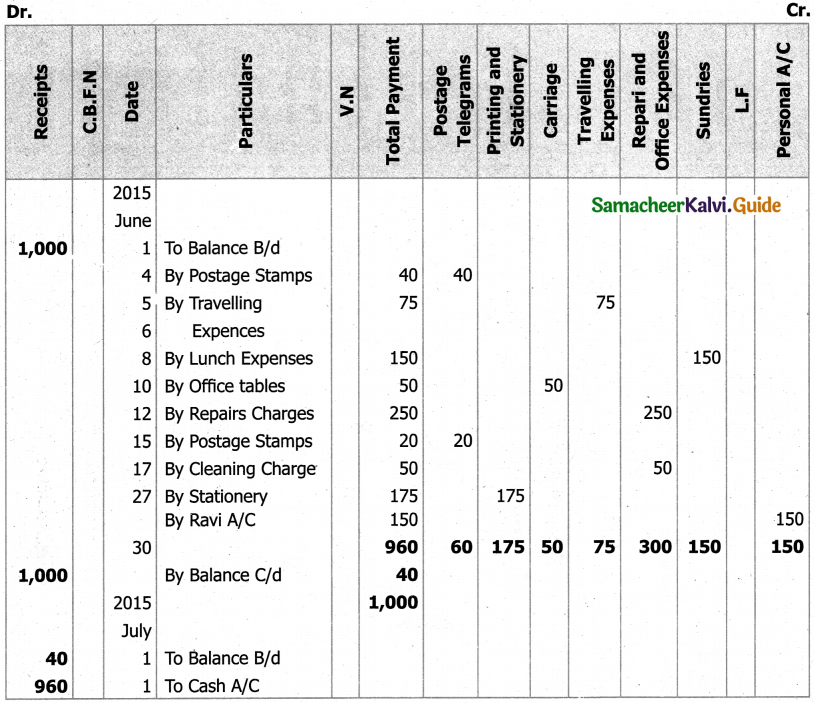

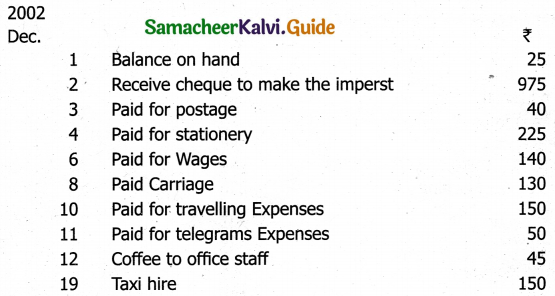

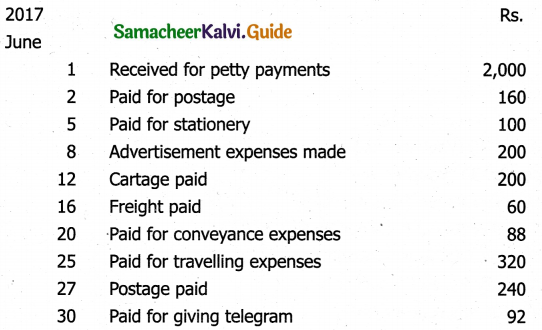

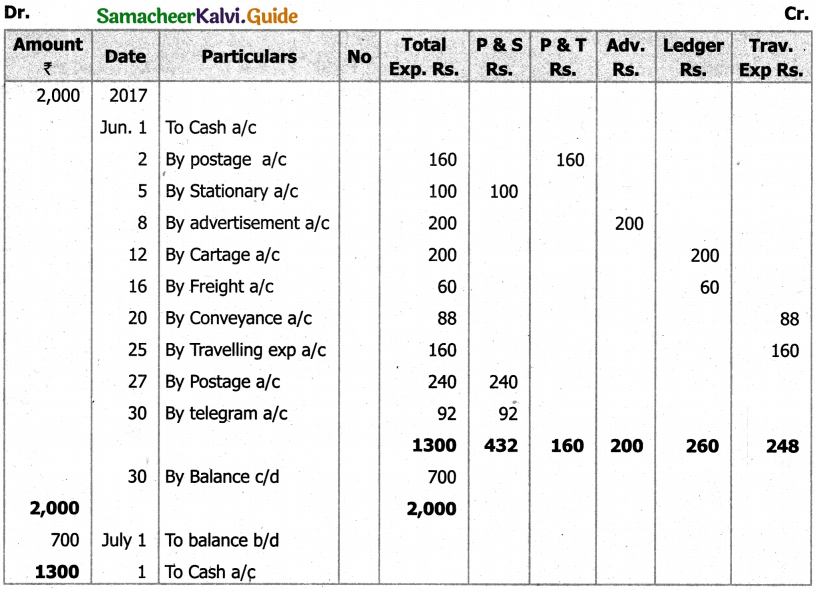

From the following transactions for the month of June 2017, drew up a Petty Cash Book in analytical form:

Solution:

Analytical Petty Cash Book

![]()

Question 16.

Prepare Mr. Keerthivasan single column cash book.

Solution:

Single column book of Mr. Kishore Kumar

Question 17.

Record the transactions given below in the double column cash book of cash book (with discount and cash columns) of Mr. Kirubakaran.

Solution:

Double column cash book or Mr. Kirunakaran (Cash book with discount and cash column)

Question 18.

Enter the following transaction in the cash book with discount and cash columns of Mr. Guru.

Solution:

Double column cash book or Mr. Guru

(Cash book with discount and cash column)

![]()

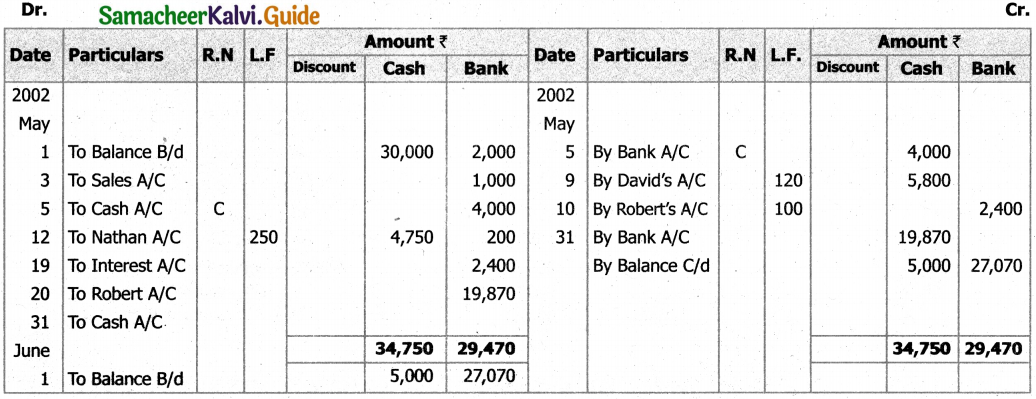

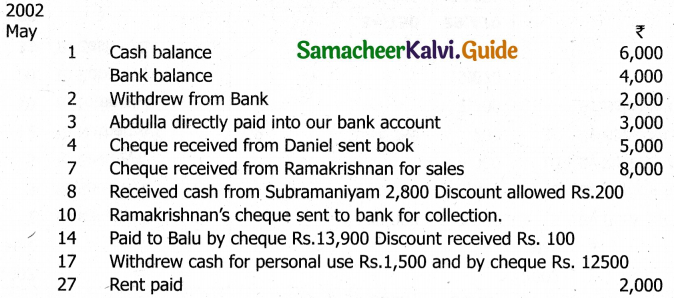

Question 19.

Enter the following transaction in the three column cash book of Mr. kumaran.

2002

May

1 – Cash in hand Rs. 30,000; Cash at bank Rs. 2,000

3 – Received cheque for goods sold to Arun and bank Rs. 1,000

5 – Paid into bank Rs. 4,000

9 – Paid cash to david from whom goods worth Rs.6,000 were purchased for credit on 1st May on term 2% cash discount within two weeks

10 – Paid to Robert by cheque Rs.2,400 in full settlement of his account of Rs.2,500

12 – Received cash from Nathan Rs.4,750 Discount allowed Rs.250

19 – Interest allowed by bank Rs.200

20 – Robert to whom we have usued a cheque has reported that our cheque is dishounred

22 – Roshan got exchange for a Five hundred rupee note

31 – Paid into bank all cash in excess of Rs.5000

Solution:

Trible column cash book or Mr. Guru

(Cash book with discount and cash column)

Question 20.

Enter the following transactions in the triple column cash hook of Mr.Yogesh

Solution:

Trible column cash book or Mr. Kumaran

(Cash book with discount and cash column)