Students can download 11th Economics Chapter 5 Market Structure and Pricing Questions and Answers, Notes, Samcheer Kalvi 11th Economics Guide Pdf helps you to revise the complete Tamilnadu State Board New Syllabus, helps students complete homework assignments and to score high marks in board exams.

Tamilnadu Samacheer Kalvi 11th Economics Solutions Chapter 5 Market Structure and Pricing

Samacheer Kalvi 11th Economics Market Structure and Pricing Text Book Back Questions and Answers

PART – A

Multiple Choice Questions:

Question 1.

In which of the following is not a type of market structure Price will be very high?

(a) Perfect competition

(b) Monopoly

(c) Duopoly

(d) Oligopoly

Answer:

(b) Monopoly

![]()

Question 2.

Equilibrium condition of a firm is ______

(a) MC = MR

(b) MC > MR

(c) MC < MR

(d) MR = Price

Answer:

(a) MC = MR

Question 3.

Which of the following is a feature of monopolistic competition?

(a) One seller

(b) Few sellers

(c) Product differentiation

(d) No entry

Answer:

(c) Product differentiation

Question 4.

A firm under monopoly can earn ______ in the short run.

(a) Normal profit

(b) Loss

(c) Supernormal profit

(d) More loss

Answer:

(c) Supernormal profit

![]()

Question 5.

There is no excess capacity under ……………………..

(a) Monopoly

(b) Monopolistic competition

(c) Oligopoly

(d) Perfect competition

Answer:

(d) Perfect competition

Question 6.

Profit of a firm is obtained when ______

(a) TR < TC

(b) TR – MC

(c) TR >TC

(d) TR = TC

Answer:

(c) TR > TC

![]()

Question 7.

Another name of the price is …………………..

(a) Average Revenue

(b) Marginal Revenue

(c) Total Revenue

(d) Average Cost

Answer:

(a) Average Revenue

Question 8.

In which type of market, AR and MR are equal ______

(a) Duopoly

(b) Perfect competition

(c) Monopolistic competition

(d) Oligopoly

Answer:

(b) Perfect competition

![]()

Question 9.

In a monopoly, the MR curve lies below …………………….

(a) TR

(b) MC

(c) AR

(d) AC

Answer:

(c) AR

Question 10.

Perfect competition assumes ______

(a) Luxury goods

(b) Producer goods

(c) Differentiated goods

(d) Homogeneous goods

Answer:

(d) Homogeneous goods

![]()

Question 11.

Group equilibrium is analysed in ……………………

(a) Monopolistic competition

(b) Monopoly

(c) Duopoly

(d) Pure competition

Answer:

(a) Monopolistic competition

Question 12.

In monopolistic competition, the essential feature is ______

(a) Same product

(b) selling cost

(c) Single seller

(d) Single buyer

Answer:

(b) selling cost

Question 13.

Monopolistic competition is a form of ……………………

(a) Oligopoly

(b) Duopoly

(c) Imperfect competition

(d) Monopoly

Answer:

(c) Imperfect competition

![]()

Question 14.

Price leadership is the attribute of ______

(a) Perfect competition

(b) Monopoly

(c) Oligopoly

(d) Monopolistic competition

Answer:

(c) Oligopoly

Question 15.

Price discrimination will always lead to ……………………

(a) Increase in output

(b) Increase in profit

(c) Different prices

(d) (b) and (c)

Answer:

(d) (b) and (c)

![]()

Question 16.

curve under monopolistic competition will be ______

(a) Perfectly inelastic

(b) Perfectly elastic

(c) Relaively elastic

(d) Unitary elastic

Answer:

(c) Relaively elastic

Question 17.

Under perfect competition, the shape of demand curve of firm is …………………

(a) Vertical

(b) Horizontal

(c) Negatively sloped

(d) Positively sloped

Answer:

(b) Horizontal

![]()

Question 18.

In which market form, does absence of competition prevail?

(a) Perfect competition

(b) Monopoly

(c) Duopoly

(d) Oligopoly

Answer:

(b) Monopoly

Question 19.

Which of the following involves maximum exploitation of consumers?

(a) Perfect competition

(b) Monopoly

(c) Monopolistic competition

(d) Oligopoly

Answer:

(b) Monopoly

![]()

Question 20.

An example of selling cost is ______

(a) Raw material cost

(b) Transport cost

(c) Advertisement cost

(d) Purchasing cost

Answer:

(c) Advertisement cost

Part – B

Answer the following questions in one or two sentences.

Question 21.

Define market?

Answer:

In economics, the term ‘Market’ refers to a system of exchange between the buyers and the sellers of a commodity. The exchange may be direct or indirect.

![]()

Question 22.

Who is the price-taker?

Answer:

A firm under perfect competition is a price-taker. Both buyer and seller accept the price fixed in the industry.

Question 23.

Point out the essential features of pure competition?

Answer:

- The absence of any monopoly element.

- There are large buyers and sellers.

- Homogenous product and uniform price.

- Free entry and exit.

![]()

Question 24.

What is the selling cost?

Answer:

Under monopolistic competition, as the products are differentiated, the producer has to incur expenses to make his brand popular. The expenditure involved in selling the product is called “selling cost’ Eg. Cost for advertisements.

Question 25.

Draw demand curve of a firm for the following:

Answer:

(a) Perfect competition

(b) Monopoly

(a) Perfect competition:

The average revenue of the firm is greater than its average cost.

The firm is earning supernormal profit.

Explanation:

In the figure, output is measured along the x-axis and price, revenue, and cost along the y-axis. OP is the prevailing price in the market. PL is the demand curve or average and the marginal

revenue curve. The firm is in equilibrium at point ‘E’ where MR = MC and MC cuts the MR curve from below at the point of equilibrium.

(b) Monopoly:

A monopoly is a market structure characterized by a single seller, selling the unique product with the restriction for a new firm to enter the market. A monopoly is a form of market where there is a single seller selling a particular commodity for which there are no close substitutes.

Question 26.

Mention any two types of price discrimination.

Answer:

- Personal: Different prices are charged for different individuals. For example, the railways give tickets at a concessional rate to the ‘Senior citizens’ for the same journey.

- Geographical: Different prices are charged at different places for the same product. For example, a book sold within India at a price is sold in a foreign country at a lower price.

![]()

Question 27.

Define “Excess capacity”?

Answer:

Excess capacity is the difference between the optimum output that can be produced and the actual output produced by the firm.

Part – C

Answer the following questions in one paragraph.

Question 28.

What are the features of a market?

Answer:

- Buyers and sellers of a commodity or a service.

- A commodity to be bought and sold.

- Price agreeable to buyer and seller.

- Direct or indirect exchange.

Question 29.

Specify the nature of entry of competitors in perfect competition and monopoly?

Answer:

Perfect competition:

Under perfect competition, there is the possibility of free entry and exit of the firm. In the short run, if an efficient producer produces supernormal profits, it attracts new firms to enter the industry. When a large number of firms enter, the supply would increase, resulting in lower prices. An inefficient producer, disturbed by the loss, quit the market. It results in a decrease in supply so the price will go up.

Monopoly:

In a monopoly, there is a strict barrier for entry of any new firm.

![]()

Question 30.

Describe the degrees of price discrimination.

Answer:

Price discrimination has become widespread in almost all monopoly markets. According to A.C. Pigou, there are three degrees of price discrimination.

1. First-degree price discrimination :

A monopolist charges the maximum price that a buyer is willing to pay. This is called perfect price discrimination. Joan Robinson named it as “Perfect discriminating monopoly.”

2. Second-degree price discrimination :

Under this degree, buyers are charged prices in such a way that a part of their consumer’s surplus is taken away by the sellers. This is called imperfect price discrimination. Joan Robinson named it as “Imperfect discriminating monopoly”. Under this degree, buyers are divided into different groups and a different price is charged for each group. (E.g) Ticket prices in cinema theatres.

3. Third-degree price discrimination :

The monopolist splits the entire market into a few sub-market and charges different prices in each submarket. The groups are divided on the basis of age, sex, and location. (E.g) Railways charge lower fares from senior citizens.

![]()

Question 31.

State the meaning of selling cost with an example?

Answer:

Under monopolistic competition as the products are differentiated, the producer has to incur expenses to make his brand popular. The expenditure involved in selling the product is called “selling cost”.

According to Prof.Chamberlin, selling cost is the cost incurred in order to alter the position or shape of the demand curve for a product.

Under perfect competition and monopoly there is soiling COM.

(Eg.) Advertisements, Free services, Home delivery etc.,

![]()

Question 32.

Mention the similarities between perfect competition and monopolistic competition?

Answer:

Perfect Competition | Monopolistic Competition |

| 1. Large number of buyers and sellers. | Large number of buyers and many sellers. |

| 2. Homogeneous product & uniform price. | Close substitute commodity. |

| 3. Free Entry and exit. | Free Entry and exit. |

| 4. Very small size of market for each firm. | Small size of market. |

| 5. It has no monopoly power | Limited power |

| 6. Uniform power (or) low price | Moderate power |

| 7. Price policy price taker | Low control elasticity of demand |

| 8. Price elasticity – infinite | Some control over price depending on consumers brand loyalty. |

![]()

Question 33.

Differentiate between “firm” and Industry?

Answer:

Firm | Industry |

| 1. A firm refers to a single production unit in the industry, producing a large or a small quantum of a commodity or service, and selling it at a price in the market. | The industry refers to a group of firms producing the same product or service in an economy. |

| 2. Its main objective is to earn a profit. There may be other objectives as described by managerial and behavioral theories of the firm. | For example, A group of firms producing cement is called a cement industry. |

![]()

Question 34.

State the features of duopoly?

Answer:

- Each seller is fully aware of his rival’s motive and actions.

- Both sellers may collude (they agree on all matters regarding the sale of a commodity)

- They may enter into cut-throat competition.

- There is no product differentiation.

- They fix the price for their product with a view to maximizing their profit.

Part – D

Answer the following questions in about a page.

Question 35.

Bring out the features of perfect competition?

Answer:

According to Joan Robinson, “Perfect competition prevails when the demand for the output of each producer is perfectly elastic. It is an ideal but imaginary market. 100% of perfect competition cannot be seen.

Features of the perfect competition :

(a) a Large number of buyers and sellers :

Each individual buyer buys a very very small quantum of a product as compared to that found in the market. This means that he has no power to fix the price of the product. He is only a price-taker and not a price-maker. As the number of sellers is large the seller is also a price-taker.

(b) Homogenous product and uniform price :

The. products are homogenous in nature and are perfectly substitutable. All the units of the product are identical. Therefore a uniform price prevails in the market.

(c) Free entry and exit:

In the short run, if the very efficient producer earns supernormal profits, new firms enter the industry. When a large number of firms enter, the supply would increase, resulting in lower prices. If a inefficient producer incurs a loss, the loss incurring firms quit the market. So the existing firms could earn more profit as supply decreases.

(d) Absence of transport cost:

The prevalence of the uniform price is also due to the absence of the transport cost. . e) Perfect mobility of factors of production :

As there is perfect mobility of the factors of production, uniform price exists. As they enjoy perfect freedom of mobility the price gets adjusted.

(f) Perfect knowledge of the market:

All buyers and sellers have a thorough knowledge of the quality of the product, prevailing price, etc.

(g) No government intervention:

There is no government regulation on the supply of raw materials and in the determination of price etc.

![]()

Question 36.

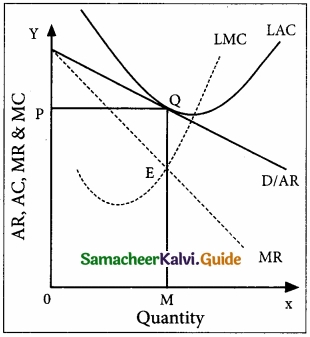

How price and output are determined under the perfect competition?

Answer:

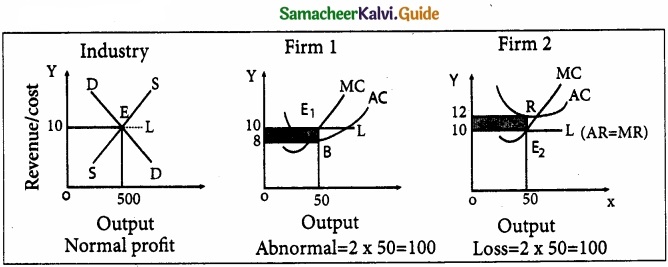

Perfect Competition: Firm’s Equilibrium in the Short Run

- In the short run, at least a few factors of production are fixed. The firms under Perfect Competition take the price (10) from the industry and start adjusting their quantities produced. For example Qd = 100 – 5P and Qs = 5P.

- At equilibrium Qd = Qs

- Therefore 100 – 5P = 5P

100 = 10P; 100/10 = P; Qd = demand

P = 10 ; P = Price

Qd = 100 – 5(10); Qs = Supply

100 – 50 = 50

Qs = 5 (10) = 50

Therefore 50 = 50

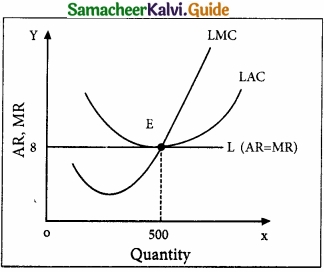

This diagram consists of three panels. The equilibrium of an industry is explained in the first panel. The demand and supply forces of all the firms interact and the price is fixed as 10. The equilibrium of an industry is obtained at 50 units of output.

In the second part of the diagram, AC curve is lower than the price line. The equilibrium condition is achieved where MC = MR. Its equilibrium quantity sold is 50. With the prevailing price, ₹10 it experiences supernormal profit. AC = ₹8, AR = ₹10.

Its total revenue is 50 × 10 = 500. Its total cost is 50 × 8 = 400.

Therefore, its total profit is 500 – 400 = 100.

In the third part of the diagram, the firm’s cost curve is above the price line. The equilibrium condition is achieved at the point where MR = MC. Its quantity sold is 50. With the prevailing price, it experiences loss. (AC > AR)

Its total revenue is 50 × 10 = 500. Its total cost is 50 × 12 = 600.

Therefore, its total loss is 600 – 500 = 100.

As profit prevails in the market, new firms will enter the industry, thus increasing the supply of the product. This means a decline in the price of the product and an increase in the cost of production. Thus, the abnormal profit will be wiped out; the loss will be incurred.

When loss prevails in the market, the existing loss-making firms will exit the industry, thus decreasing the supply of the product. This means a rise in the price of the product and a reduction in the cost of production. So the loss will vanish; Profit will emerge. Consequent to the entry and exit of new firms into the industry, firms always earn ‘normal profit’ in the long run as shown in the diagram.

![]()

Question 37.

Describe the features of oligopoly?

Answer:

Features of oligopoly:

1. Few large firms :

Very few big firms own the major control of the whole market by producing a major portion of the market demand.

2. Interdependence among firms :

The price and quality decisions of a particular firm are dependent on the price and quality decisions of the rival firms.

3. Group behaviour :

The firms under oligopoly realise the importance of mutual co-operation.

4. Advertisement cost :

The oligopolist could raise sales either by advertising or improving the quality of the product.

5. Nature of the product:

Perfect oligopoly means homogeneous products and imperfect oligopoly deals with heterogeneous products.

6. Price rigidity :

It implies that prices are difficult to be changed. The oligopolist firms do not change their prices due to the fear of rival’s reaction.

![]()

Question 38.

Illustrate price and output determination under Monopoly?

Answer:

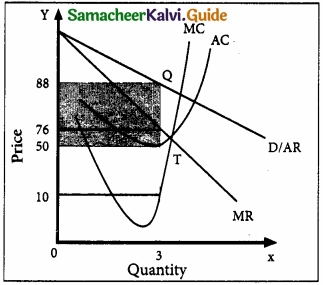

Price and Output Determination under Monopoly:

A monopoly is a one firm-industry. Therefore, a firm under a monopoly faces a downward-sloping demand curve (or AR curve). Since, under monopoly AR falls, as more units of output are sold, the MR lies below the AR curve (MR < AR). The monopolist will continue to sell his product as long as his MR > MC.

He attains equilibrium at the level of output when its MC is equal to MR. Beyond this point, the producer will experience loss and hence will stop selling. Let us take the following hypothetical example of Total Revenue Function and Total cost function.

TR = 100Q – 4Q2 and

TC = Q3 – 18Q2 + 91Q + 12.

Therefore AR = 100 – 4Q;

MR = 100 – 8Q;

AC = Q2 – 18Q + 91 + 12/Q;

= 3Q2 – 36Q + 91;

When Q = 3,

AR = 100 – 4(3) = 88,

= (3)2 – 18(3) + 91 + 12/3 = 9 – 54 + 91 + 4 = 50;

MR = 100 – 8(3) = 76;

= 3(3)2 – 36(3) + 91 = 27 – 108 + 91 = 10

From this diagram, till he sells 3 units output, MR is greater than MC, and when he exceeds this output level, MR is less than MC. The monopoly firm will be in equilibrium at the level of output where MR is equal to MC. The price is 88.

To checkup how much profit the monopolist is making at the equilibrium output, the average revenue curves and the average cost curves are used. At the equilibrium level of output is 3; the average revenue is 88 and the average cost is 50. Therefore (88 – 50 =38) is the profit per unit.

Total profit = (Average. Revenue – Average Cost) × Total output = (88 – 50) × 3 = 38 × 3 = 114.

![]()

Question 39.

Explain price and output determined under monopolistic competition with help of the diagram?

Answer:

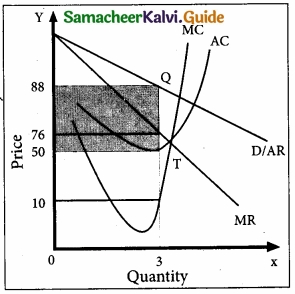

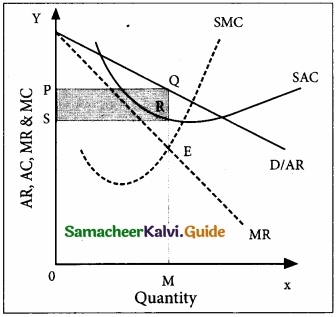

Price and Output Determination under Monopolistic competition:

The firm under monopolistic competition achieves its equilibrium when it’s MC = MR, and when its MC curve cuts its MR curve from below. If MC is less than MR, the sellers will find it profitable to expand their output.

Under Monopolistic Competition:

- The demand curve is downwards sloping.

- There are close substitutes.

- The demand curve is fairly elastic.

Under monopolistic competition, different firms produce different varieties of the product and sell them at different prices. Each firm under monopolistic competition seeks to achieve equilibrium as regards.

- Price and output

- Product adjustment

- Selling cost adjustment.

Short-run equilibrium:

The profit maximisation is achieved when MC = MR.

‘OM’ is the equilibrium output. ‘OP’ is the equilibrium price. The total revenue is ‘OMQP’. And the total cost is ‘OMRS’. Therefore, total profit is ‘PQRS’. This is super normal profit under short-run.

But under differing revenue and cost conditions, the monopolistically competitive firms may incur a loss.

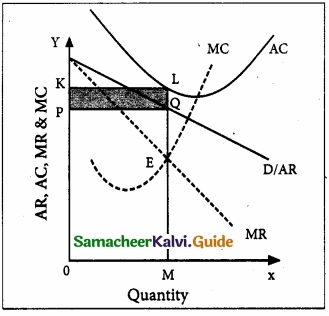

As shown in the diagram, the AR and MR curves are fairly elastic. The equilibrium situation occurs at point ‘E’, where MC = MR and MC cuts MR from below.

The equilibrium output is OM and the equilibrium price is OP. The total revenue of the firm is ‘OMQP’ and the total cost of the firm is ‘OMLK’ and thus the total loss is ‘PQLK’. This firm incurs a loss in the short run.

Long-Run Equilibrium of the Firm and the Group Equilibrium:

In the short run, a firm under monopolistic competition may earn a supernormal profit or incur loss. But in the long run, the entry of the new firms in the industry will wipe out the supernormal profit earned by the existing firms. The entry of new firms and the exit of loss-making firms will result in normal profit for the firms in the industry.

In the long run, AR curve is more elastic or flatter because plenty of substitutes are available. Hence, the firms will earn an only normal profit.

Samacheer Kalvi 11th Economics Market Structure and Pricing Additional Important Questions and Answers

Part – A

Multiple Choice Questions:

Question 1.

The supply curve in the very short period is _______

(a) Horizontal

(b) Vertical

(c) Slopes downward

(d) Slopes upward

Answer:

(b) Vertical

Question 2.

Who was propounded by the concept of imperfect competition?

(a) Philip Kotler

(b) Joan Robinson

(c) (a) and (b)

(d) None of these

Answer:

(b) Joan Robinson

![]()

Question 3.

Second condition for equilibrium of the firm _______

(a) MC curve should cut MR curve from below

(b) MC curve should cut MR curve from above

(c) MC curve coincides with MR curve

(d) None of the above

Answer:

(a) MC curve should cut MR curve from below

Question 4.

Price discrimination is called ………………………. monopoly.

(a) Increasing

(b) Decreasing

(c) Equalization

(d) Discriminating

Answer:

(d) Discriminating

Question 5.

In which type of market the seller is a price taker?

(a) Perfect competition

(b) Monopoly

(c) Monopolistic competition

(d) Duopoly

Answer:

(a) Perfect competition

![]()

Question 6.

The perfect competitive firms are ……………………..

(a) Price maker

(b) Price in charge

(c) Price given

(d) Price taker

Answer:

(d) Price taker

Question 7.

There is a barrier for entry of new firm in _______

(a) Monopoly

(b) Monopolistic competition

(c) Perfect competition

(d) Duopoly

Answer:

(a) Monopoly

Question 8.

The most important form of selling cost is ………………………..

(a) Advertisement

(b) Sales

(c) Homogeneous product

(d) None

Answer:

(a) Advertisement

![]()

Question 9.

Supply curve in long run _______

(a) Perfectly elastic

(b) Perfectly inelastic

(c) Less elastic

(d) None

Answer:

(a) Perfectly elastic

Question 10.

_______ classified market based on time.

(a) Marshall

(b) Adamsmith

(c) Chamberlin

(d) Hicks

Answer:

(a) Marshall

Part – B

Answer the following questions in one or two sentences.

Question 1.

Define Dumping?

Answer:

- Dumping refers to the practice of the monopolist charging a higher prices for his product in the local market and lower price in the foreign market.

- Through dumping, a country expands its command over other countries for its product. This is also called as “ International Price Discrimination”. For example, India’s electronic market is flooded with China’s products.

![]()

Question 2.

Classify market-based on the area?

Answer:

- Local market

- Provincial market

- National market

- International market

Question 3.

What is the classification of markets?

Answer:

Markets are classified

1. On the Basis of Area

- Local market

- Provincial market

- National market

- International market

2. On the Basis of Time:

- Very short period market (or) Market period

- Short period market

- Long-period market

- Very long period market (or) A secular period market

3. On the Basis of Quality of the Commodity:

- Wholesale market

- Retail market

4. On the Basis of Competition:

- Perfect competition market

- Imperfect competition market

Part – C

Answer the following questions in one paragraph.

Question 1.

State the sources of monopoly power?

Answer:

1. Natural Monopoly:

Ownership of the natural raw materials [E.g. Gold mines – Africa, Coal mines, Nickel – Canada, etc]

2. State Monopoly:

Single supplier of some special services [E.g – Railways in India], (ill) Legal Monopoly: A Monopoly firm can get its monopoly power by getting patent rights, a trademark from the government.

![]()

Question 2.

Explain Long-Run Equilibrium of the Firm and the Group Equilibrium?

Answer:

In the short run, a firm under monopolistic competition may earn a supernormal profit or incur a loss. But in the long run, the entry of the new firms in the industry will wipe out the supernormal profit earned by the existing firms. The entry of new firms and the exit of loss-making firms will result in normal profit for the firms in the industry. In the long run, the AR curve is more elastic or flatter because plenty of substitutes are available. Hence, the firms will earn an only normal profit.

![]()

Question 3.

Classify markets based on time.

Answer:

Alfred Marshall classified the market on the basis of time.

1. Very short period or Market period :

If occurs when with the available time the quantum supplied of a product cannot be changed. The supply curve is vertical; it is inelastic. Demand plays a major role in price determination. (Eg.) During floods the price of food products raises.

2. Short period market:

Here the quantum supplied of a product can be changed to some extent. Supply curve is little more elastic to meet an increased demand.

3. Long-period market:

Here the quantum supplied of a product can be changed to a larger extent. The supply curve is very much elastic. All the factors are variable and the price of the product is moderate.

4. Very long period market (or a secular period market) :

It occurs when the entire economy undergoes a drastic change. Newer technologies are introduced and most modem products are produced.

(Eg.) The entry of pen-drive has driven out compact disc (CD)

Part – D

Answer the following questions in about a page.

Question 1.

Explain the wastes of monopolistic competition.

Answer:

1. Idle capacity :

Unutilized capacity is the difference between the optimum output and the actual output. In the long run, a monopolistic firm produces the output corresponding to the minimum average cost, which is less than the optimum output. It creates artificial scarcity. This leads to excess capacity which is actually a waste in monopolistic competition.

2. Unemployment:

As the firm produce less than optimum output, the productive capacity is not used to the fullest extent. This will lead to unemployment of human resources also.

3. Advertisement:

There is a lot of waste in competitive advertisements which leads to high cost to the consumers. It is also claimed that advertisements cheat consumers by giving false information about the product.

4. Too many varieties of goods :

Introducing too many varieties of a good is another waste here. The goods differ in size, shape, style and colour. A reasonable number of varieties would be sufficient. Cost per unit can also be reduced if only a few varieties are produced in larger quantity instead of larger varieties with small quantities.

5. Inefficient firms :

Inefficient firms charge prices higher than their marginal cost. These firms can be kept out of the industry. But the buyer’s preference for such products are large they continue to exist. Efficient firms cannot drive out the inefficient firms because the efficient firms cannot spend for an advertisement to attract buyers. In reality, consumers are mostly emotional rather than rational.

ACTIVITY

Question 1.

Divide the class into five groups. Assign each group a market structure; for first group perfect competition, second group monopoly, third group oligopoly, fourth group Duopoly and for fifth group monopolistic competition. Now each student is to identify a business or organization or seller that orperate in that market structure. Ask each student to prepare a brief description of the following?

Answer:

- Name of the market structure

- Business name

- Industry

- Identify the conditions of market structure

- What are prices of a particular product, whether same price or different price?.

- Is there non-price competition?

Activity to be done by the students in the classroom under the guidance of the teacher. (Group Activity)

![]()

Question 2.

Find out the number of firms in Tamil Nadu or India which are producing/selling TV and Mobile phones?

Answer:

Producing / selling of Television firms:

- Samsung

- L.G

- Croma

- Panasonic

- Philips

- Sharp

- Mitsubishi

- Sony

- Red mi

- Apple TV

- Akai

Producing / Selling / of Mobile Phones Firms:

- Samsung

- Apple

- Red mi

- Oppo

- Gionee

- Infocus

- Nokia

- L.G

- Mi

- Lave

- Micro max

- Black bei

- Moto

- Letv