Students can download 11th Economics Chapter 7 Indian Economy Questions and Answers, Notes, Samcheer Kalvi 11th Economics Guide Pdf helps you to revise the complete Tamilnadu State Board New Syllabus, helps students complete homework assignments and to score high marks in board exams.

Tamilnadu Samacheer Kalvi 11th Economics Solutions Chapter 7 Indian Economy

Samacheer Kalvi 11th Economics Indian Economy Text Book Back Questions and Answers

PART – A

Multiple Choice Questions:

Question 1.

The main gold mine region in Karnataka is ………………………….

(a) Kolar

(b) Ramgiri

(c) Anantpur

(d) Cochin

Answer:

(a) Kolar

![]()

Question 2.

Economic growth of a country is measured by national income indicated by …………………………..

(a) GNP

(b) GDP

(c) NNP

(d) Per capita income

Answer:

(b) GDP

Question 3.

Which one of the following is a developed nations?

(a) Mexico

(b) Ghana

(c) France

(d) Sri Lanka

Answer:

(c) France

![]()

Question 4.

The position of Indian Economy among the other strongest economies in the world is ……………………….

(a) Fourth

(b) Seventh

(c) Fifth

(d) Tenth

Answer:

(b) Seventh

Question 5.

Mixed economy means ………………………..

(a) Private sectors and banks

(b) Co-existence of Public and Private sectors

(c) Public sectors and banks

(d) Public sectors only

Answer:

(b) Co-existence of Public and Private sectors

![]()

Question 6.

The weakness of Indian Economy is ………………………..

(a) Economic disparities

(b) Mixed economy

(c) Urbanisation

(d) Adequate employment opportunities

Answer:

(a) Economic disparities

Question 7.

A scientific study of the characteristics of population is …………………………..

(a) Topography

(b) Demography

(c) Geography

(d) Philosophy

Answer:

(b) Demography

![]()

Question 8.

The year 1961 is known as ……………………………

(a) Year of small divide

(b) Year of Population Explosion

(c) Year of Urbanisation

(d) Year of Great Divide

Answer:

(b) Year of Population Explosion

Question 9.

In which year the population of India crossed one billion mark?

(a) 2000

(b) 2001

(c) 2005

(d) 1991

Answer:

(b) 2001

![]()

Question 10.

The number of deaths per thousand population is called as ………………………

(a) Crude Death Rate

(b) Crude Birth Rate

(c) Crude Infant Rate

(d) Maternal Mortality Rate

Answer:

(a) Crude Death Rate

Question 11.

The number of births per thousand population is called as ………………………

(a) Crude death rate

(b) Mortality rate

(c) Morbidity rate

(d) Crude Birth Rate

Answer:

(d) Crude Birth Rate

![]()

Question 12.

Density of population = ………………………

(a) Land area / Total Population

(b) Land area / Employment

(c) Total Population / Land area of the region

(d) Total Population / Employment

Answer:

(c) Total Population / Land area of the region

Question 13.

Who introduced the National Development Council in India?

(a) Ambedkar

(b) Jawaharlal Nehru

(c) Radhakrishanan

(d) VKRV Rao

Answer:

(b) Jawaharlal Nehru

Question 14.

Who among the following propagated Gandhian Economic thinkings?

(a) Jawaharlar Nehru

(b) VKRV Rao

(c) JC Kumarappa

(d) A.K.Sen

Answer:

(c) JC Kumarappa

![]()

Question 15.

The advocate of democratic socialism was ………………………..

(a) Jawaharlal Nehru

(b) P C Mahalanobis

(c) Dr. Rajendra Prasad

(d) Indira Gandhi

Answer:

(a) Jawaharlal Nehru

Question 16.

Ambedkar the problem studied by in the context of Indian Economy is ………………………..

(a) Small land holdings and their remedies

(b) Problem of Indian Currency

(c) Economics of socialism

(d) All of them

Answer:

(b) Problem of Indian Currency

![]()

Question 17.

Gandhian Economics is based on the Principle ………………………..

(a) Socialistic idea

(b) Ethical foundation

(c) Gopala Krishna Gokhale

(d) Dadabhai Naoroji

Answer:

(b) Ethical foundation

Question 18.

VKRV Rao was a student of ………………………….

(a) JM Keynes

(b) Colin Clark

(c) Adam smith

(d) Alfred Marshal

Answer:

(a) JM Keynes

![]()

Question 19.

Amartya Kumara Sen received the Nobel prize in Economics in the year …………………………

(a) 1998

(b) 2000

(c) 2008

(d) 2010

Answer:

(a) 1998

Question 20.

Thiruvalluvar economic ideas mainly dealt with ………………………….

(a) Wealth

(b) Poverty is the curse in the society

(c) Agriculture

(d) All of them

Answer:

(d) All of them

PART – B

Answer the following questions in one or two sentences.

Question 21.

Write the meaning of Economic Growth?

Answer:

A country’s economic growth is usually indicated by Gross Domestic Product (GDP). The GDP is the total monetary value of the goods and services produced by that country over a specific period of time, usually one year.

![]()

Question 22.

State any two features of a developed economy?

Answer:

- High National Income

- High Per Capita Income

Question 23.

Write a short note on natural resources?

Answer:

Natural resources are stock or reserve that can be drawn from nature. The major natural resources are land, forest, water, mineral, and energy.

![]()

Question 24.

Point out any one feature of the Indian economy?

Answer:

India has a mixed economy.

- Indian economy is a typical example of a mixed economy.

- This means both the private and public sectors co-exist and function smoothly.

- The fundamental and heavy industrial units are being operated under the public sector, while, due to the liberalization of the economy, the private sector has gained importance.

- This makes it a perfect model for public-private partnerships.

Question 25.

Give the meaning of non-renewable energy?

Answer:

The sources of energy which cannot be renewed or re-used are called non-renewable energy.

(Eg.) Coal, Oil, Gas, etc.

![]()

Question 26.

Give a short note on Sen’s ‘Choice of Technique’?

Answer:

Sen’s ‘Choice of Technique’ was a research work where he argued that in a labour surplus economy, generation of employment cannot be increased at the initial stage by the adaptation of capital – intensive technique.

Question 27.

List out the reasons for low per capita income as given by VKRV Rao?

Answer:

Rao gave the following reasons for low per capita income and low levels of per capita nutrition in India:

- Uneconomic holdings.

- Low levels of water availability for crops.

- Excess population pressure on agriculture due to the absence of a large industrial sector.

- Absence of capital.

- Absence of autonomy in currency policy.

PART – C

Answer the following questions in one paragraph.

Question 28.

Define Economic Development?

Answer:

- The level of economic development is indicated not just by GDP, but by an increase in citizen’s quality of life or well-being.

- The quality of life is being assessed by several indices such as Human Development Index [HDI]

- On the basis of the level of economic development, nations are classified as developed and developing economies.

- Developed economies are those countries which are industrialized.

- Developed economics are also termed as Advanced Countries.

- On the other hand, countries that have not fully utilized their resources like land, mines, workers, etc., and have low per capita income are termed as underdeveloped economics.

![]()

Question 29.

State Ambedkar’s Economic ideas on agricultural economics?

Answer:

Dr. B.R.Ambedkar was a versatile personality. In 1918, he published a paper “Smallholding in India and their remedies” citing Adam Smith’s “Wealth of Nations”, he made a fine distinction between “Consolidation of holdings” and “Enlargement of holdings”.

Question 30.

Write a short note on Village Sarvodhaya?

Answer:

- According to Gandhi, “Real India was to be found in the village and not in towns or cities”.

- So he suggested the development of self-sufficient self-dependent villages.

![]()

Question 31.

Write the strategy of Jawaharlal Nehru in India’s planning?

Answer:

- Jawahar lal Nehru was responsible for the introduction of planning in our country.

- To Nehru, the plan was essentially an integrated approach for development.

- He said the essence of planning is to find the best way to utilize all resources of manpower, money and so on.

- Planning for Nehru was essentially linked up with industrialization and eventual self-reliance for the country’s economic growth on a self-accelerating growth.

- Nehru carried through this basic strategy of planned development.

Question 32.

Write the VKRV Rao’s contribution on the multiplier concept?

Answer:

- VKRV Rao’s examination of the “Interrelation between investment, income and multiplier is an underdeveloped economy” [1952] was his major contribution to macroeconomic theory.

- Asa thinker, teacher, economic adviser, and direct policymaker, VKRV Rao followed the footstep of his great teacher, John Maynard Keynes.

![]()

Question 33.

Write a short note on Welfare Economics given by Amartya Sen?

Answer:

- Amartya Sen was awarded the Nobel prize for his contributions to welfare economics.

- Sen’s major point has been that the distribution of income/consumption among the persons below the poverty line is to be taken into account.

- Sen has focused on the poor, viewing them not as objects of pity requiring charitable hand-outs, but as disempowered folk needing empowerment in all aspects.

Question 34.

Explain social infrastructure?

Answer:

- Social infrastructure refers to those structures which are improving the quality of manpower and contribute indirectly towards the growth of an economy.

- These structures are outside the system of production and distribution.

- The development of these social structures help in increasing the efficiency and productivity of manpower.

- For example, schools, colleges, hospitals and other civic amenities.

- It is a fact that one of the reasons for the low productivity of Indian workers is the lack of development of social infrastructure.

Education in India:

- The Indian education system has flourished and developed with the growing needs of the economy.

Health in India:

- Health in India is a state government responsibility.

- The Central Council of Health and Welfare formulates the various health care projects and health department reform policies.

PART – D

Answer the following questions in about a page.

Question 35.

Explain the strong features of the Indian economy?

Answer:

- India has a mixed economy: In India, both private and public sectors coexist.

- Agriculture plays the key role: Around 60% of the people in India depend upon agriculture for their livelihood.

- An emerging market: India has a high potential for prospective growth which attracts FDI and FII.

- Emerging economy: As a result of rapid economic growth Indian economy has a place among the G20 countries.

- Fast-growing economy: India has emerged as the world’s fastest-growing economy in 2016-17 with 7.1% GDP next to China.

- Fast-growing service sector: The service sector, contributes a lion’s share of the GDP in India.

- Large domestic consumption: Due to large domestic consumption the standard of living has considerably improved and lifestyle has changed.

- paid growth of urban areas: Improved connectivity in transport and communication, education, and health have speeded up the pace of urbanization.

- Stable macroeconomy: The current year’s economic survey represents the Indian economy to be a heaven of macroeconomic stability, resilence and optimism.

- Demographic dividend: India is a proud owner of the maximum percentage of youth. This has invited foreign investments to the country and outsourcing opportunities.

![]()

Question 36.

Write the importance of mineral resources in India?

Answer:

Important Mineral Resources:

1. Iron -ore:

- India possesses high-quality iron-ore in abundance.

- The total reserves of iron ore in the country are about 14.630 million tonnes of hematite and 10,619 million tonnes of magnetite.

- Hematite iron is mainly found is Chattisgarh, Jharkhand, Odisha, Goa, and Karnataka.

- Some deposits of iron ore are also found in Kerala, Tamilnadu, and Andra Pradesh.

2. Coal and Lignite:

- Coal is the largest available mineral resource.

- India ranks third in the world after China and the USA in coal production.

- The main centers of coal in India are West Bengal, Bihar, Madhya Pradesh, Maharashtra, Odisha, and Andhra Pradesh.

- The bulk of the coal production comes from Bengal-Jharkhand coalfields.

3. Bauxite:

- Bauxite is a main source of metal like aluminium.

- Major reserves are concentrated in the East Coast bauxite deposits of Odisha and Andhra Pradesh.

4. Mica:

- Mica is a heat-resisting mineral which is also a bad conductor of electricity.

- It is used in electrical equipment as an insulator.

- India stands first in sheet mica production and contributes 60% of mica trade in the world.

- The important mica bearing pegmatite is found in Andhra Pradesh, Jharkhand, Bihar and Rajasthan.

5. Crude Oil:

- Oil is being explored in India at many places of Assam and Gujarat.

- Digboi, Badarpur, Naharkatia, Kasimpur, Palliaria, Rudrapur, Shivsagar, Mourn [All in Assam], and Hay of Khambhat, Ankleshwar and Kalor [All in Gujarat] are the important places of oil exploration in India.

6. Gold:

- India possesses only a limited gold reserve.

- There are only three main gold mine regions-Kolar Goldfield, Kolar district and Hutti Goldfield in Raichur district [both in Karnataka] and Ramgiri Goldfield in Anantpur district [Andhra Pradesh].

7. Diamond:

- The total reserves of a diamond is estimated at around 4582, thousand carats which are mostly available in Panna [Madhya Pradesh], Rammallakota of Kumar district of Andhra

Pradesh and also in the Basin of Krishna River. - The new Kimberlile fields have been discovered in Raipur and Bastar districts of Chhattisgarh, Nuapada and Bargarh districts of Odisha, Narayanpet-Maddur Krishna areas of Andhra Pradesh, and Raichur-Gulbarga districts of Karnataka.

![]()

Question 37.

Bring out Jawaharlal Nehru’s contribution to the idea of economic development?

Answer:

Jawahar Lal Nehru was one of the Chief builders of modem India. He was a great patriot, thinker and statesman. His ideas of economic development are :

1. Democracy : He was a firm believer in democracy. He believed in free speech, civil liberty, adult franchise and the rule of law and parliamentary democracy.

2. Secularism : Secularism is another signal contribution of Nehru to India. There are so many religions in India but there is no domination by religious majority.

3. Planning : Nehru was responsible for the introduction of planning in our country. The plan was essentially an integrated approach for development. Planning for Nehru was essentially linked up with industrialization and eventual self-reliance for the country’s economic growth on a self-accelerating growth.

4. Advancement of Science : Nehru made a great contribution to the advancement of Science, research, technology and industrial development. In his period, many IITs and research institutions were established. He always insisted on scientific temper.

5. Democratic socialism : Nehru put the country on the road towards a socialistic pattern of society. Nehru’s socialism is democratic socialism.

![]()

Question 38.

Write a brief note on the Gandhian economic ideas?

Answer:

Gandhian Economics is based on ethical foundations. Gandhi wrote, “Economics that hurts the moral well-being of an individual or a nation is immoral, and therefore, Sinful”. Again in 1924, Gandhi repeated the same belief “ that economy is untrue which ignores or disregards moral values”.

Salient features of Gandhian Economic Thought:

1. Village Republics:

- India lives in villages.

- He was interested in developing the villages as self-sufficient units.

- He opposed the extensive use of machinery, urbanization, and industrialization.

2. On Machinery:

- Gandhi described machinery as ‘Great sin’. He said that “Books could be written to demonstrate its evils”.

- It is necessary to realize that machinery is bad.

- Instead of welcoming machinery as a boon, we should look upon it as evil.

- It would ultimately cease.

3. Industrialism:

- Gandhi considered industrialism as a curse on mankind.

- He thought industrialism depended entirely on a country’s capacity to exploit.

4. Decentralization :

- Gandhi advocated a decentralized economy i. e., production at a large number of places on a small scale or production in the people’s homes.

5. Village Sarvodaya:

- According to Gandhi, “ Real India was to be found in villages and not in towns or cities”.

- So, he suggested the development of self-sufficient, self-dependent villages.

6. Bread Labour:

- Gandhi realized the dignity of human labour.

- He believed that God created man to eat his bread by the sweat of his brow.

- Bread labour or body labour was the expression that Gandhi used to mean manual labour.

7. The Doctrine of Trusteeship:

- Trusteeship provides a means of transforming the present capitalist order of society into an egalitarian one.

8. On the Food Problem:

- Gandhi was against any sort of food controls.

- Once India was begging for food grain, but now India tops the world with very large production of food grains, fruits, vegetables, milk, egg, meat etc.

9. On Population:

- Gandhi opposed the method of population control through contraceptives.

- He was, however, in favour of birth control through Brahmacharya or self-control.

- He considered self-control as a sovereign remedy to the problem of over-population.

10. On Prohibition:

- Gandhi advocated cent percent prohibition.

- Gandhi regarded the use of liquor as a disease rather than a vice.

- He felt that it was better for India to be poor than to have thousands of drunkards.

- Many states depend on revenue from liquor sales.

Samacheer Kalvi 11th Economics Indian Economy Additional Important Questions and Answers

PART – A

Multiple Choice Questions:

Question 1.

The basic factors determining population growth are ………………………..

(a) Birth rate

(b) Death rate

(c) Migration

(d) All the above

Answer:

(d) All the above

![]()

Question 2.

……………………… is a crude indicator for living standard.

(a) Gross National Product [GNP]

(b) Gross Domestic Product [GDP]

(c) Net National Product [NNP]

(d) Per Capita Income [PCI]

Answer:

(a) Gross National Product [GNP]

Question 3.

India followed the ……………………… plan.

(a) Short term

(b) Long term

(c) Midterm

(d) Perspective

Answer:

(c) Midterm

![]()

Question 4.

…………………….. is the basic causes of poverty.

(a) Low agriculture productivity

(b) Rapid growth of population

(c) Low saving and disguised unemployment

(d) All the above

Answer:

(d) All the above

Question 5.

In recent time India followed the ……………………… planning.

(a) Five year

(b) Indicative

(c) Modified

(d) Innovative

Answer:

(b) Indicative

Question 6.

……………………………. was responsible for the introduction of planning in our Country.

(a) Ambedkar

(b) Jawaharlal Nehru

(c) Radhakrishnan

(d) VKRV Rao.

Answer:

(b) Jawaharlal Nehru

![]()

Question 7.

………………………. is the largest available mineral resource.

(a) Coal

(b) Iron-ore

(c) Bauxite

(d) Mica

Answer:

(a) Coal

Question 8.

The National Harbour board was set up in ………………………

(a) 1947

(b) 1948

(c) 1949

(d) 1950

Answer:

(d) 1950

Question 9.

India stands first in sheet mica production and contributes ……………………. % of mica trade in the world.

(a) 50%

(b) 60%

(c) 70%

(d) 80%

Answer:

(b) 60%

![]()

Question 10.

……………………… is thereby also called as the backbone of the Indian economy.

(a) Agricultural

(b) Industrial

(c) Small Scale Industries

(d) Cottage industries

Answer:

(a) Agricultural

PART – B

Answer the following questions in one or two sentences.

Question 1.

List out the education system in India?

Answer:

The education system in India consists of primarily six levels:

- Nursery class

- Primary class

- Secondary level

- Higher secondary level

- Graduation

- Post-graduation

![]()

Question 2.

Define “Renewable Resources’?

Answer:

Renewable energy sources

These are the kind of energy source which can be renewed or reused again and again. These kinds of materials do not exhaust or literally speaking these are available in abundant or infinite quantity. Example for this kind include

- Solar energy

- Wind energy

- Tidal energy

- Geothermal energy

- Biomass energy

Question 3.

Write a short note on Infrastructure development?

Answer:

Infrastructural development means the development of many support facilities. These facilities may be divided into (z) economic infrastructure and (ii) social infrastructure. Economic infrastructure includes – transport, communication, energy, irrigation, monetary and financial institutions. Social infrastructure includes – education, training and research, health, housing and civic amenities.

PART – C

Answer the following questions in one paragraph.

Question 1.

Explain the education in India?

Answer:

Education in India:

- Imparting education on an organized basis dates back to the days of ‘Gurukul’ in India.

- The Indian education system has flourished and developed with the growing needs of the economy.

- The Ministry & Human Resource Development (MHRD) in India formulates education policy in India and also undertakes education programs.

The education system in India:

- Education in India until 1976 was the responsibility of the State governments.

- It was then brought under concurrent list [both Centre and State]

- The Centre is represented by the Ministry of Human Resource Development decides India’s education budget.

- The education system in India consists of primarily six levels:

- Nursery class

- Primary class

- Secondary level

- Higher secondary level

- Graduation

- Post-graduation

Education Institutions in India:

- Education in India follows the 10, +2 pattern.

- The accreditation of the universities is decided under the University Grant Commission Act.

- The Education Department consists of various schools, colleges, and universities imparting education on fair means for all sections of the society.

![]()

Question 2.

List out the density of the population?

Answer:

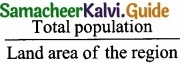

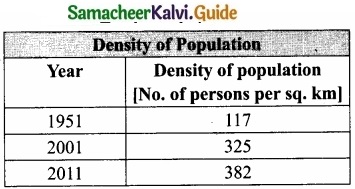

The density of population:

The density of population refers to the average number of persons residing per square kilometer. It represents the man-land ratio. As the total land area remains the same, an increase in population causes the density of the population to rise.

The density of population =

- Just before Independence, the density of the population was less than 100.

- After Independence, it has increased rapidly from 117 in 1951 to 325 in 2001.

- According to the 2011 census, the present Density of the population is 382.

- The pressure of population on land has been rising.

- Kerala, West Bengal, Bihar, and Uttar Pradesh have density higher than India’s average density.

- Bihar is the most densely populated state.

- Arunachal Pradesh has a low density of population of only 17 persons. Indian Economy 125

![]()

Question 3.

Explain “Transport”?

Answer:

Transport:

- For the sustained economic growth of a country, a well-connected and efficient transport system is needed.

- India has a good network of rail, road coastal shipping, and air transport.

- The total length of roads in India being over 30 lakh km.

- India has one of the largest road networks in the world.

- In terms of railroads, India has a broad network of railroad lines, the largest in Asia and the fourth largest in the world.

- The total rail route length is about 63,000 km and of this 13,000 km is electrified.

- The major Indian ports including Calcutta, Mumbai, Chennai, Vishakhapatnam and Goa handle about 90% of sea-borne trade and are visited by cargo carriers and passenger liners from all parts of the world.

- A comprehensive network of air routes connects the major cities and towns of the country.

- The domestic air services are being looked after by Indian Airlines and private airlines.

- The international airport service is looked after by Air India.

PART – D

Answer the following questions in about a page.

Question 1.

Explain the weakness of the Indian Economy?

Answer:

1. Large Population:

- India stands second in terms of size of the population next to China and our country is likely to overtake China in near future.

- The population growth rate of India is very high and this is always a hurdle to the growth rate.

2. Inequality and poverty:

- There exists a huge economic disparity in the Indian economy.

- The proportion of income and assets owned by top 10% of Indians goes on increasing.

- Increase in the poverty level in society and still a higher percentage of individuals are living Below Poverty Line [BPL].

- Asa result of unequal distribution of the rich becomes richer and poor becomes poorer.

3. Increasing Prices of Essential Goods:

- Even though there has been a constant growth in the GDP and growth opportunities in the Indian economy, there have been steady increase in the prices of essential goods.

- The continuous rise in prices erodes the purchasing power and adversely affects the poor people, whose income is not protected.

4. Weak Infrastructure:

- A gradual improvement in the infrastructural development.

- There is still a scarcity of the basic infrastructure like power, transport, storage etc.

5. Inadequate Employment generation:

- Growing youth population, there is a huge need of employment opportunities.

- The growth in production is not accompanied by creation of job.

- The Indian economy is characterized by “ Jobless growth”.

6. Outdated technology:

- The level of technology in agriculture and small scale Industries is still outdated and obsolete.

![]()

Question 2.

Explain the VKRV Rao’s National Income Methodology and Industrialization?

Answer:

1. Rao’s National Income Methodology:

- Rao’s name is remembered for his pioneering work on the enumeration of national income of India.

- He attempted

- To develop the national income concepts suited to India and developing countries.

- To analyze the concepts of investment, saving and multipliers is an underdeveloped economy.

- To study the compatibility of the national incomes of Industrialized and underdeveloped countries.

- Rao’s paper on “Full Employment and Economic Development” was one of the earliest contributions in the field of development towards employment.

2. Rao’s views on Industrialization:

- Rao gave the following reasons for low per Capita income and low levels of per capita nutrition in India.

- Uneconomic holdings with sub-divisions and fragmentation.

- Low levels of water availability for crops.

- Excess population pressure on agriculture due to the absence of a large industrial sector.

- Absence of capital.

- Absence of autonomy in currency policy, and in general in monetary matters encouraging holding of gold.

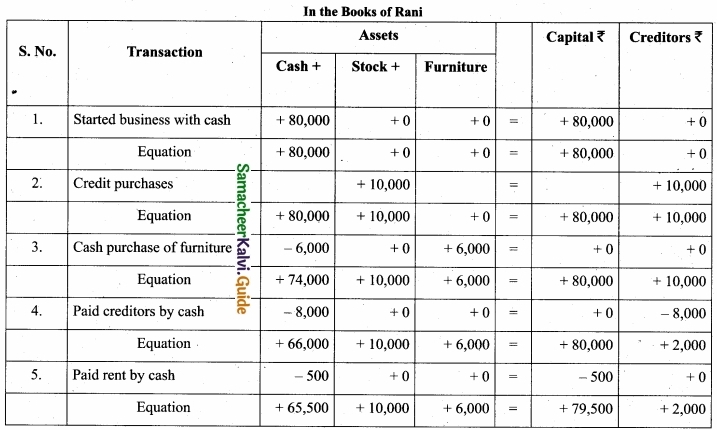

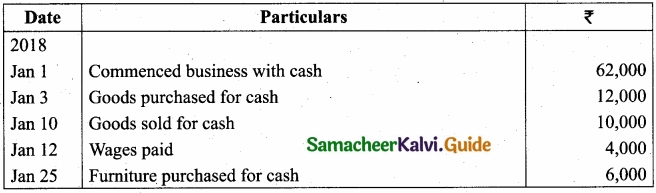

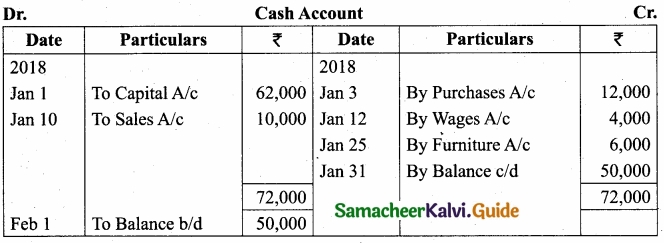

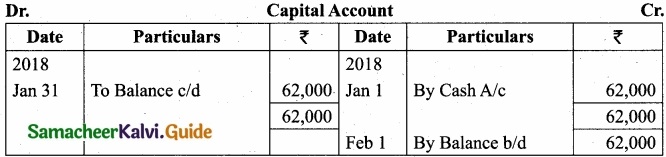

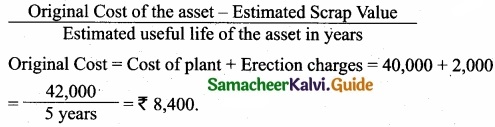

= \(\frac{1,90,00-15,000}{5}\)

= \(\frac{1,90,00-15,000}{5}\)

`

`